(H/t Mike Zaccardi)

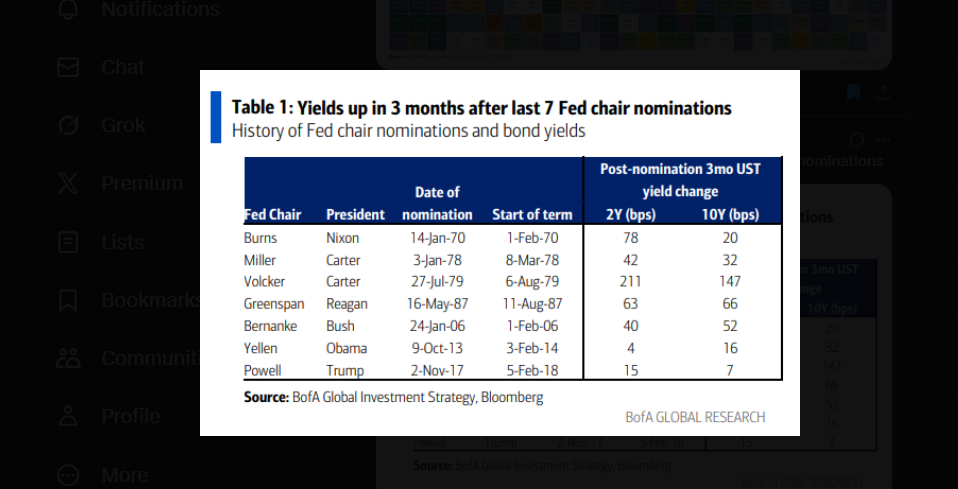

Table from Bank of America showing the change in 2-year and 10-year Treasury yields dating back to the early 1970’s, after a new Fed Chair is named.

Look for the yield curve to steepen once the new Federal Reserve Chairman takes office, which President Trump says he will announce after the start of the new year.

The one aspect of the table that’s uncertain is whether the yield increases began after the announcement, or only after the actual Fed Chair takes the position. Jay Powell’s Fed Chair position is due to end May 15, 2026, so there is some time before the yield increases may begin.

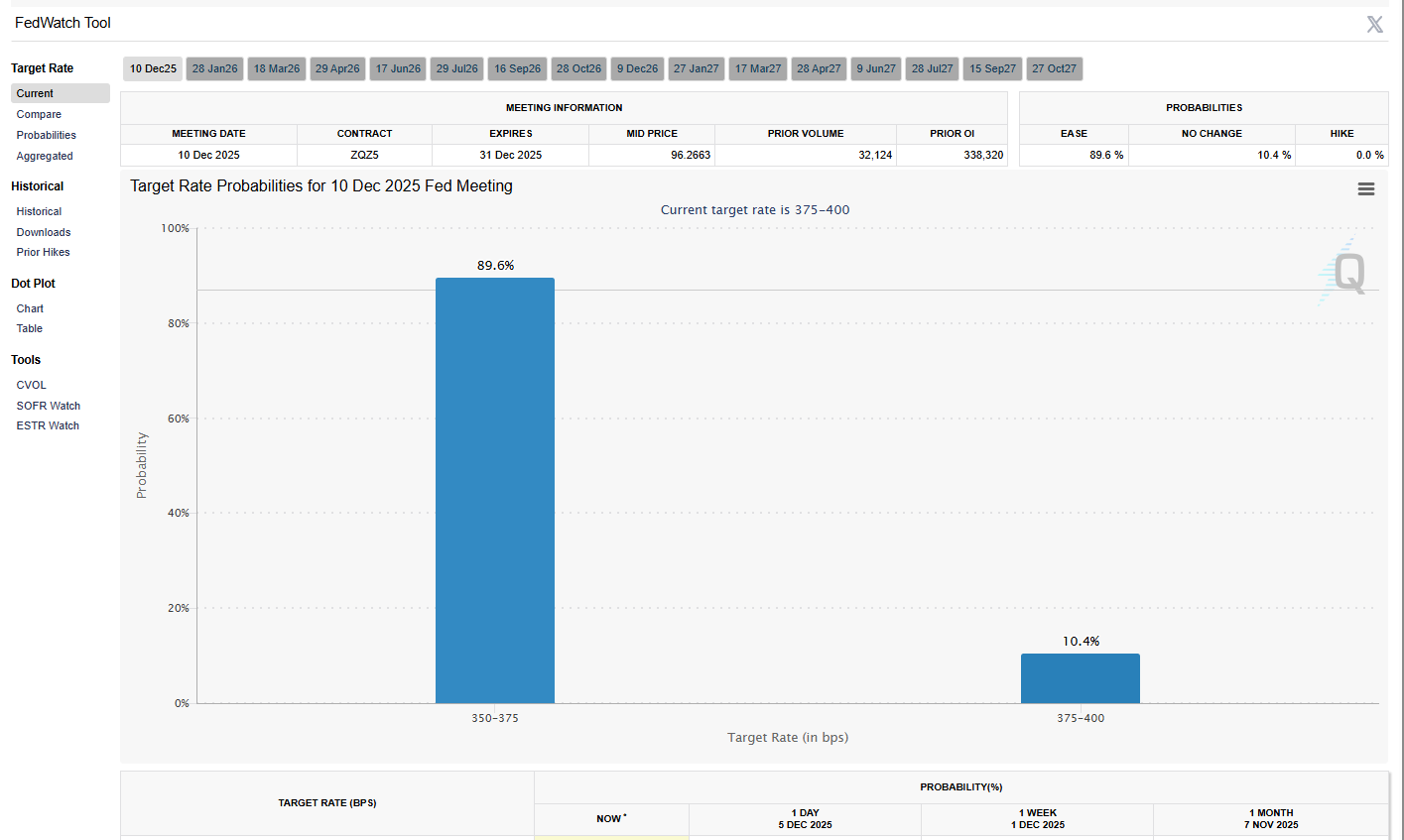

This bar chart or graph shows an 89.6% chance of a drop in the fed funds futures again on Wednesday, December 10, 2025.

The new fed funds rate is expected to be 3.625%, for an expected decline of 25 pb’s.

The Treasury yield curve remains relatively flat from fed funds to the 10-year maturity, which is yielding 4.15% as of this writing.

The 2’s – 10’s spread has been trading around +50 – 60 bp’s since early April, 2025.

With Wednesday’s expected move in fed funds, and this morning’s Treasury yield, the spreads will be 52 basis points, after the fed funds rate cut Wednesday, 12/10.

As history, I remember when Alan Greenspan was appointed to be named Paul Volcker’s successor by Ronald Reagan, and then Greenspan was met with the 1987 Crash just two months after taking over the position, and Bernanke was faced with the 2008 Financial Crisis just 30 months into his new term. (Maybe there is a pattern here.)

The mainstream financial media will create all this angst around the new Fed Chair, and like Greenspan replacing Volcker and Bernanke replacing Greenspan, monetary policy will work itself out.

Summary / conclusion: The bias of this blog was to lengthen duration in 2025 (not dramatically, just gradually) and remain long the TLT (iShares +20-year Treasury ETF), but with the AGG up just 7% YTD in ’25, the year was really a push and just so-so for fixed-income investors. The TLT’s total return as of Friday, December 5th, 2025, was 5.04%. 2025’s AGG return is the best return for the bond benchmark since 2020’s 7.48% return. That being said, the year isn’t over yet.

The TLT’s total return as of Friday, December 5th, 2025, was 5.04%.

The fact is the Treasury yield curve could steepen further in 2026, as the President continues to use the bully-pulpit to try and extract lower fed funds rate from the Federal Open Market Committee (FOMC). Certainly the first table above shows regardless of the policies of the new Fed Chair, the yield curve will build in a yield premium for uncertainty once the Fed Chairman is seated.

This blog’s largest fixed income position for balanced accounts is the JMSIX (JPMorgan Income Fund), run by Andy Norelli, and it’s outperforming the AGG year-to-date by 11 bp’s.

None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future success.

Thanks for reading.