Next Monday, the 9th of March, 2026, will be the 18th anniversary of this secular bull stock market, which began on March 9th, 2009.

The recent rotation that started 2026, which has seen – as of last Friday, February 27th, 2026 – the Mag 7 decline 6.99% YTD, while the “XMag” (a Defiance ETF), return +3.52%, while the SP 500 equal-weight (RSP) has returned +7%, the SP 500 mid-cap has returned +8.21% and the Russell 2000 has returned +6.20% to start off the first two months of 2026.

In my opinion, it’s healthy when a market does this, since it allows the patient, non-momentum investors to benefit, and it shows investors that the market isn’t just a “one-trade” party, i.e. “buy tech”, “buy the Q’s”, etc.

To be frank, even though clients are long Microsoft, which was down -18.60% YTD at the end of February ’26, this is a very mild rotation, but very similar to the kind of rotation seen in March, 2000.

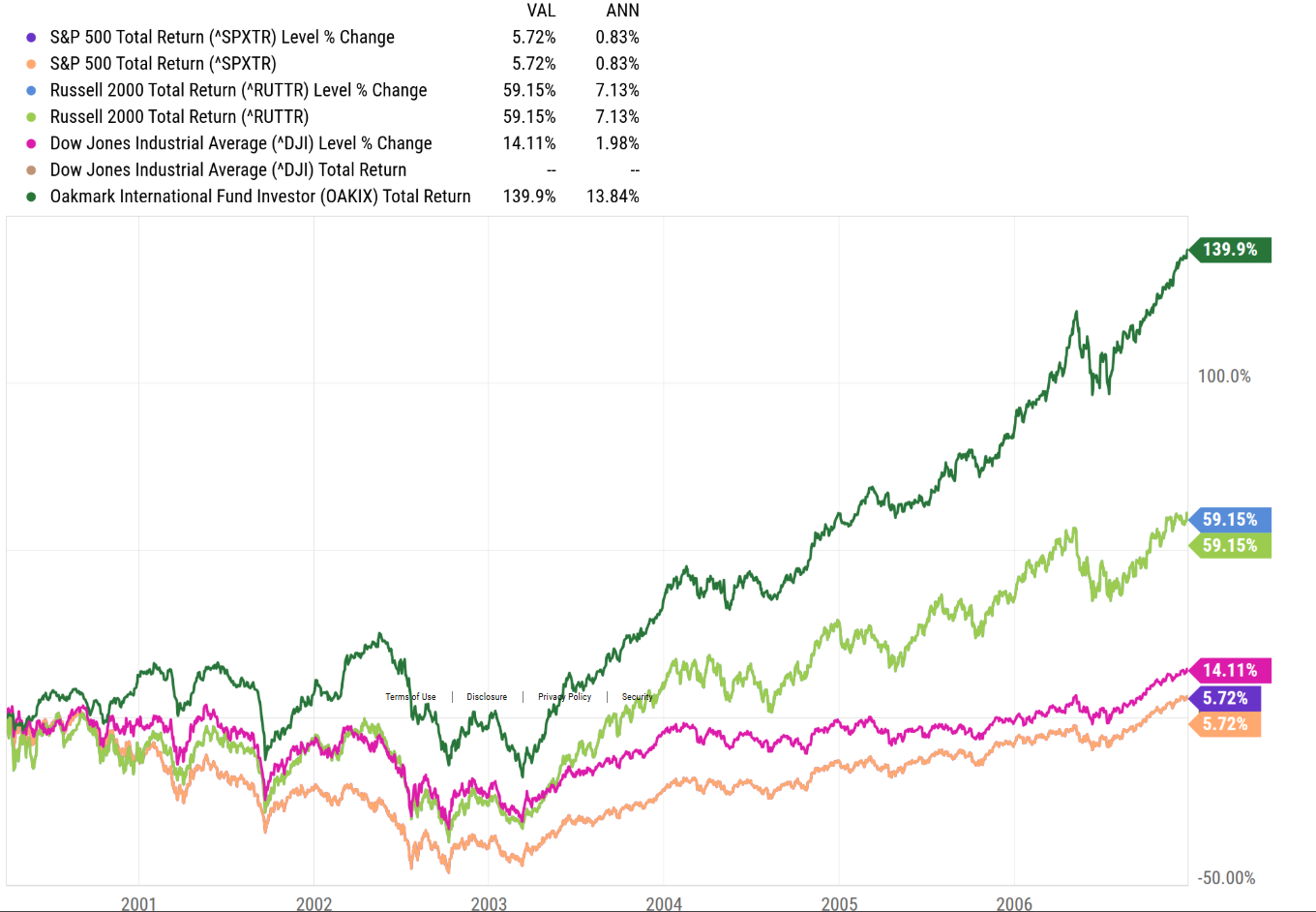

I’m not wild about this return chart from Ycharts, which shows the SP 500 versus the various asset classes that laid dormant for years in the late 1990’s and their respective returns from March 31, 2000 through March 31, 2006.

Oakmark International (OAKIX) was tossed in the mix, since in the early 2000’s, international equity and emerging markets lit the lamp for most of the decade (possibly thanks to China’s 15% per year GDP growth) while the SP 500 had it’s worst decade of annual returns since the 1930’s. During the late 1990’s, international, emerging markets and China were all but ignored.

International equity’s broad outperformance (which really started in ’25) is doing well again this year, as is emerging markets, and there is probably more left in the move if you look at the weaker dollar again in ’26.

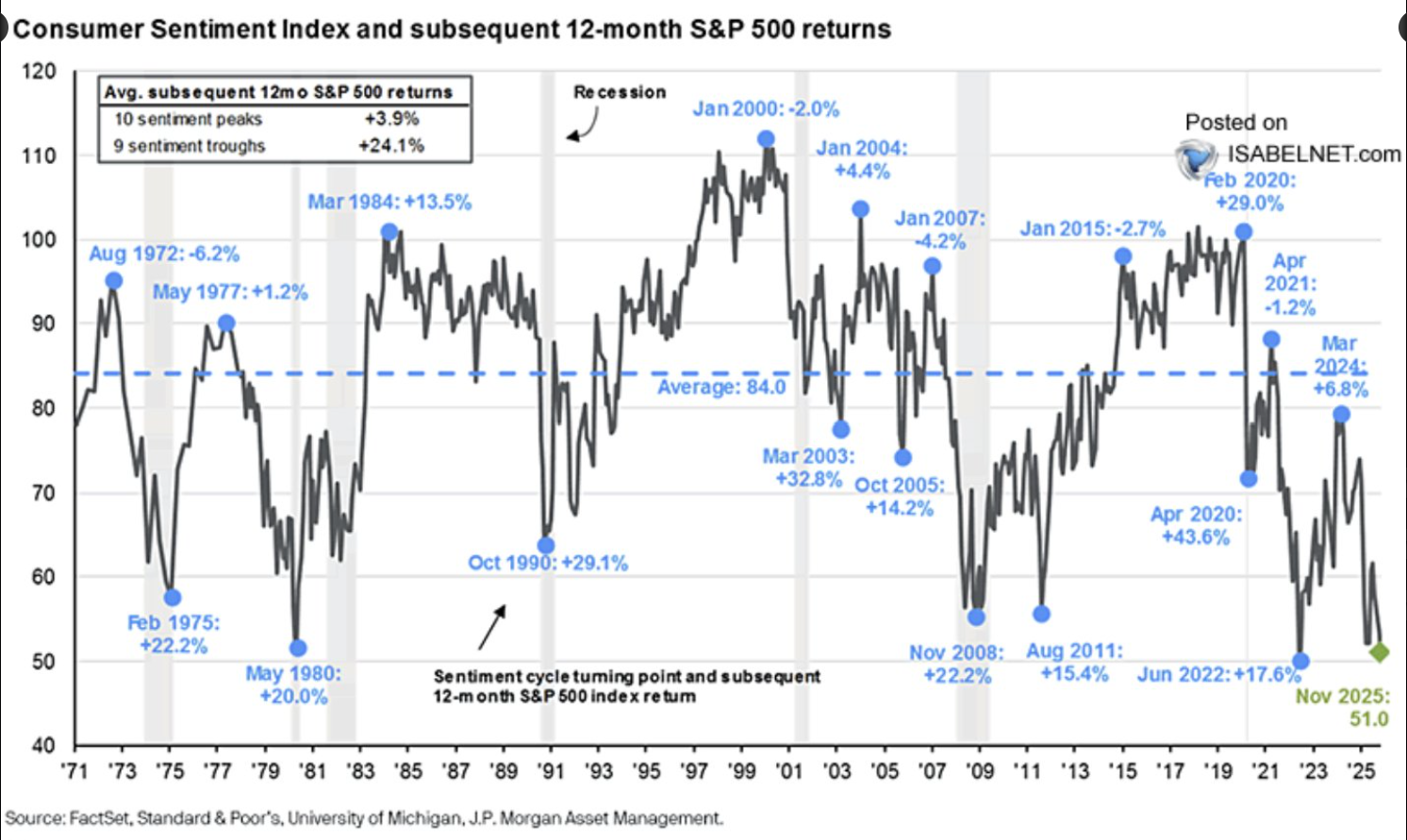

What’s the major difference between the two time periods ? In a word, “sentiment” or rather the considerable lack of bullish sentiment around stocks today (except for Nvidia and the semi’s), versus the late 1990’s when, living just north of downtown Chicago in the Lincoln Park area, I heard at least two people had quit their jobs and started trading their 401(k) on a full-time basis.

To his credit, David Kelly, JPMorgan’s Chief Global Strategist started off his early January ’26 review of Guide to the Markets, with a comment about how sentiment was much more rational today, even after an 18-year bull market. On the JPMorgan graph above, note sentiment today versus in 2000.

SP 500 sector comparisons:

Even if you look at the sector returns in YTD 2026, it’s almost the exact opposite of 2025’s sector returns:

- Consumer Discretionary (XLY): -21.4% YTD in ’26 versus the 7.36% return in ’25;

- Consumer Staples (XLP): +15.87% YTD return in ’26, versus the +1.52% return in ’25;

- Energy (XLE): +25.07% YTD return in ’26, versus +7.88 in ’25;

- Financials (XLF): -6.10% in ’26 YTD, versus +14.89% in ’25;

- Healthcare (XLV): +3.49% YTD in ’26, versus +14.50% in ’25;

- Industrials (XLI): +14.20% YTD in ’26, versus +19.20 in ’25;

- Basic Materials (XLB): +17.77%, YTD in ’26, versus +9.96 in ’25;

- Real estate (XLRE): +8.65% YTD in ’26, versus +2.60% in ’25;

- Technology (XLK): -3.62% YTD in ’26, versus +24.60% in ’25;

- Communication Services (XLC): +0.28% YTD in ’26, versus +24.07 in ’25;

- Utilities (XLU): 11.81% YTD in ’26, versus 16% in ’25;

As readers can see, tech and financials – which normally trade in a very correlated manner anyway – while communication services (Alphabet, META, Netflix, etc.) is also lagging.

Summary / conclusion: With the Iran air strike this weekend, the “trade” today acted well after the open, with the Nasdaq and SP 500 closing positive after a -1.5% down open for the major indices.

Coming into 2026, the stock market was due for a more subdued year if only from a “sequencing of returns” perspective, which is what could have been said transitioning from 2024 to 2025, but I suspect the “liberation day” selloff in February through early April of ’25, put so much fear into the market, that the rally after the early April low in ’25 was really formidable.

Do secular bull markets end die from old age ? Tom Lee doesn’t think so, and Tom is an experienced market prognosticator. In a 2025 blog post – probably at the end of the year – I looked at the various bull markets of the 20th Century, and the longest lasted from May, 1942 through 1965 – that was the DJIA, and not the SP 500 – but the 1982 to 2000 bull market lasted 18 years, and this current secular bull market has also lasted 18 years.

When the Nasdaq and SP 500 peaked in March, 2000, the resulting selloff was horrible. I thought the Nasdaq declined roughly 30% between mid-March, 2000, and the end of May, 2000. You aren’t seeing that extreme “head for the exits” yet that was seen back in 2000.

There was only one 50% correction in the SP 500 in the entire post WW II period, and that was 1973 – 1974, i.e. Watergate, Vietnam, the oil embargo, and a host of other issues.

My instinct is to treat the fact that the 2000 to 2009 bear market was the worst decade for stock returns since the 1930’s and that a little allowance should be given to this bull market since from between March, 2000 through 2009, the SP 500 saw two 50% corrections, while the Nasdaq saw an 80% correction.

But the bearish sentiment today is what keeps me leaning a little more bullish than what otherwise might be warranted. Even retail clients who are my age are bearish, and I suspect it’s that everyone remembers 2001 and 2002 and then 2008, all too clearly.

Berkshire Hathaway’s cash pile also has my attention. Warren Buffett built an equivalent cash stash in the late 1990’s.

None of this is advice or recommendation, but only an opinion. It’s hard not to note the similarities between the rotation today and early 2000. Past performance is no guarantee of future results. Readers should gauge their own comfort with portfolio volatility, and adjust accordingly.

Thanks for reading.