Walmart (WMT) is scheduled to report their fiscal Q4 ’26 financial results on Thursday morning, February 19th, before the opening bell. (Walmart is on a fiscal year, and despite the year being just one month of results, the Q4 ’26 quarter about to be reported is fiscal year is ’26 and the current year beginning Feb 1 ’26 is now fiscal ’27.)

The sell-side consensus for WMT’s Q4 ’26 is expecting $0.73 on $712.8 billion in revenue (and operating income of $8.6 billion) for expected y-o-y growth of 10.6%, 5.4% and 10.9%.

If full-year consensus estimates are met exactly, full year EPS will be $2.64 and full-year revenue will be $712.75 billion for actual y-o-y growth of 5% and 5%.

For fiscal ’27, WMT is expecting 5% revenue growth and 12% EPS, and you’d have to think that with a 50x multiple on ’26 and a 45x multiple on fiscal ’27’s EPS estimate, the stock has outrun it’s reasonable valuation in calendar 2026.

In fiscal Q3 ’26 (Oct ’25 quarter) the big story was e-commerce as WMT US ecommerce grew 28% and WMT International and Sam’s ecommerce grew +22%, with Sam’s e-commerce now profitable and International e-commerce also profitable or very close to it.

In fiscal Q3 ’26, WMT grew revenue 6%, operating income 8% and EPS 7% in the pre-holiday quarter.

The two big stories for Walmart:

Although WMT is obviously reluctant to give numbers and detail in the conference call, the e-commerce revenue spoke of Walmart’s emerging revenue flywheel is now turning profitable (although WMT isn’t saying by how much, and it’s not yet profitable in Walmart US), and advertising – another emerging spoke in the flywheel – is also growing. Per one source, Walmart advertising globally grew 53% and Walmart US (Walmart Connect) grew 33% in fiscal Q3 ’26.

Now that being said, Walmart is the only SP 500 component (outside of Amazon today) that has eclipsed $700 billion in revenue, so while the y-o-y revenue percentage numbers look impressive and healthy, these numbers could still still be small relative to entire pie.

To give readers some idea of scale, Walmart US revenue was 68% of Walmart’s total revenue in fiscal Q3 ’26, while Walmart US operating profit was 86% of total operating profit, in Q3 ’26.

The other emerging story for Walmart is grocery delivery in Walmart US, which I have tried repeatedly in the western suburbs of Chicago, not without some frustration and confusion, as Walmart works out grocery delivery door-to-door in America. (More written lower in the article).

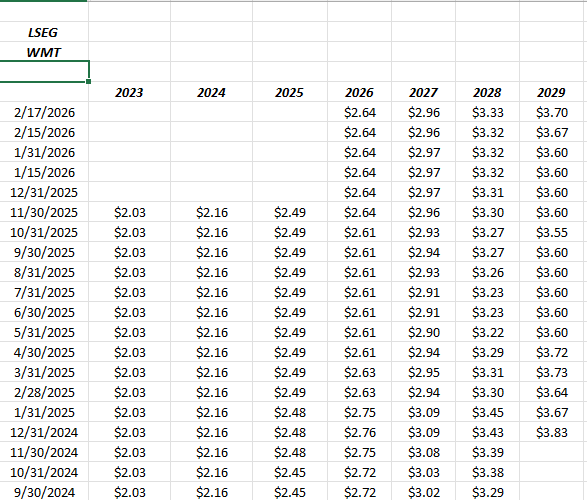

Walmart EPS / Revenue estimate revisions:

(Source: LSEG I/B/E/S estimates as of 2/17/26)

Readers are looking at fiscal year 2026 and beyond, and readers should be able to see the peak in EPS estimates in late 2024, and then the gradual weakening as tariffs kicked in for the retail giant.

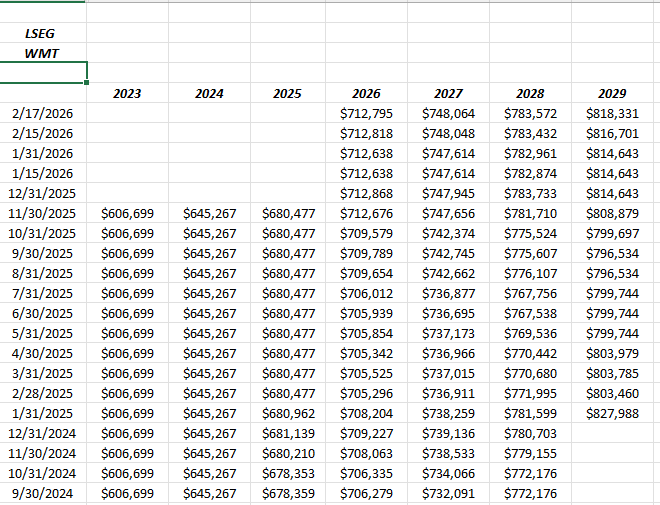

(Source: LSEG I/B/E/S estimates as of 2/17/26)

Revenue estimate revisions for 2026, 2027 and 2028 show that slow, steady upward drift that is typical of Walmart revenue.

The battle for grocery between Walmart and Amazon:

From modeling both Walmart and Amazon since the mid-1990’s and posting full financials including income statements, balance sheets and cash-flow statements, not to mention EPS and revenue estimates for the last 30 years, you get to know companies in a different way from just the public perception. The evolution of conference call notes and commentary is always evolving as these businesses evolve, and one thing that’s been clear in Walmart calls is the emergence of e-commerce and their desire to deliver “grocery” door-to-door. Amazon announced their intention to close the Amazon Fresh and Amazon Go stores before their last conference call, and they will now deliver “grocery” door-to-door, with an additional cost via Amazon Prime.

For Walmart customers, as I am, it’s been interesting to watch the evolution of grocery. Walmart has charged me for both regular Walmart grocery delivery and Walmart+ (driver enters your home to stock delivery, which I don’t use) and to say the service is a bit “inconsistent” is an understatement. With Amazon now pushing for grocery deliver likely to be fulfilled at the Whole Foods stores to start, Walmart’s growing e-commerce grocery business will eventually be running head-to-head against Amazon, but for now the I’m guessing the numbers are small for each company.

Depending on which analyst you read, Walmart’s brick-and-mortar grocery business is anywhere from 50% to 70% of that now-over $700 billion in revenue, so grocery delivery might (someday) start to cannibalize the store traffic.

As of February ’26, this is a cumbersome process for both these companies, and it will be interesting to watch it play out in real time. I’d give Walmart a slight edge to the head-on battle given their store experience with grocery, but the truck delivery and driver experience could be (and has been) difficult. Amazon has the door-to-door delivery down cold, although they are now charging extra for that privilege (after 20 years of “free” delivery), but they now have to grapple with grocery as a product line.

Stay tuned.

Summary / conclusion: Walmart has had quite a run year-to-date in calendar ’26, +20.18% year-to-date (YTD) in the first six weeks of 2026, and as of Friday, February 14th, 2026. Other consumer staples stocks like Costco (COST) have also performed well YTD, and some of the original Walmart position this blog has held over the last few years has been trimmed prior to Thursday morning’s release.

Walmart’s revenue flywheel and the growth in areas like advertising and e-commerce are opportunities to capture additional “margin-rich” revenue particularly in advertising.

In this blog’s late November ’25 Walmart earnings preview and earnings summary this blog got a little carried away with the e-commerce gains vs Amazon, and I had to issue a tempered response to a reader. Walmart’s ecommerce share per an AI search, is 6.4% – 9.6%, while Amazon is much higher at 36% – 53%. It’s interesting that the same search listed Walmart’s and Amazon’s online grocery market share, at 31.6% to 22.6% respectively.

Current EPS estimates for Walmart are looking for 12% EPS growth in fiscal ’27 and ’28, substantially better than fiscal year 2026’s +5%. The increase in the stock price may have discounted this faster EPS growth already.

The AI implementation announced in April ’23 and then again in ’24 were mainly supply center cost savings, so I haven’t given up on the expected margin gains for Walmart if these supply-chain are fully realized and if the additional flywheel revenue – like advertising – becomes material.

The current WMT position is about 1.25% of total assets. A correction in the stock seems inevitable here in the next few months, given the run it’s had.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. All EPS and revenue data for WMT is sourced from LSEG I/B/E/S. None of this information may be updated, and if updated may not be done in a timely fashion.

Thanks for reading.