If the sell-side consensus estimate is met for Walmart’s fiscal Q3 ’26 (essentially calendar ’25 with a January ’26 quarter end), Walmart will print it’s first trailing-twelve-month of revenue in excess of $700 billion.

Think about that. The US economy is $33 trillion in size and Walmart revenue is 2.1% of the entire US GDP.

Speaking of Walmart consensus estimates, when the retail giant reports its Q3 ’26 quarter on Thursday morning, November 20th, before the opening, the consensus estimates are looking for $117.4 billion in revenue, $0.60 in earnings per share, and $7.1 billion in operating income for expected year-over-year (y-o-y) growth of +4.6%, +3.4% and -10%, respectively.

In fiscal Q2 ’26 or last quarter, revenue rose 5%, EPS +2%, and operating income was flat y-o-y. Grocery and general merch comped in line, but the “flywheel” changes that Walmart is undergoing (i.e. advertising, Walmart Connect and Global advertising) are growing in the low 20% range.

Here’s the last 3 articles written on Walmart this year (earnings previews and summaries), in August ’25, May ’25, and February, ’25, that talks about the growth in Walmart’s “flywheel” (basically emerging new revenue streams), with the expectation that with the grocery and general merchandise business remaining roughly stable, that the new revenue streams should eventually boost margins.

Walmart to my knowledge has not disclosed the percentage of revenue these new businesses, but management has been fairly forthcoming about annual growth rates.

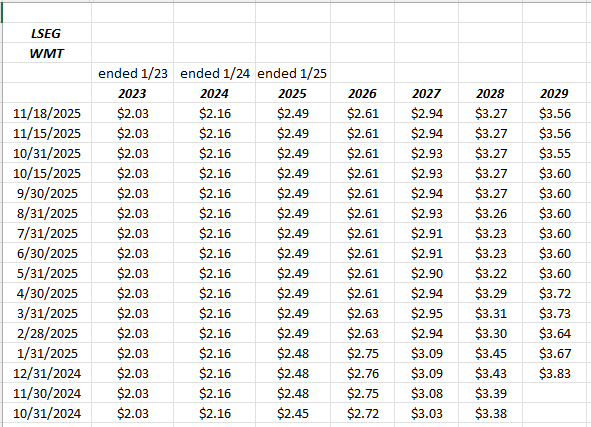

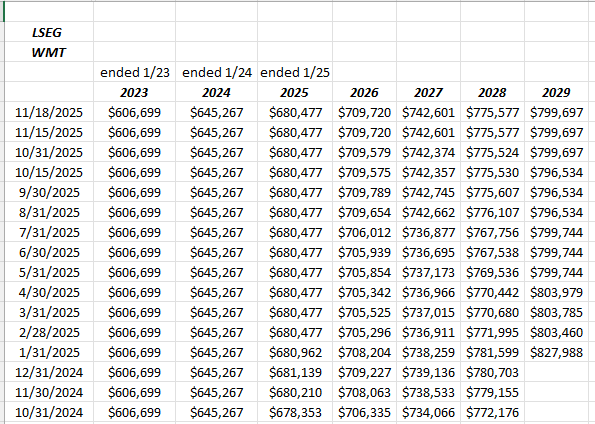

Walmart EPS and revenue estimates:

The one interesting aspect to Walmart’s consensus EPS estimate is that after exiting calendar 2024 with positive revisions, the tariffs took a slight tool on the numbers, but fiscal 2026 has steadied, and fiscal 2027 EPS estimates have seen slight positive revisions so, the tariff impact could be wearing off.

Walmart revenue estimate revisions have continued on a mildly positive track since last fall ’24.

Walmart revenue estimate revisions have continued on a mildly positive track since last fall ’24.

Walmart’s valuation:

The stock never looks cheap on a PE valuation, which is very similar to how most consumer staple stocks trade.

With Walmart trading at $102 – $103 coming into the Thursday morning earnings report, based on current EPS estimates of $2.61 for fiscal ’26 and $2.94 for fiscal ’27, the multiple on Walmart is 38x and 35x those estimates for “expected” growth of 4% and 13% respectively.

This blog has always talked to readers about Walmart’s cash-flow multiple of 18x the trailing-twelve-month estimate of $5.31 (as of July ’25), since the store depreciation of Walmart’s 10,800 stores is added back to operating cash-flow since it’s a non-cash expense.

Is 18x cash-flow a great valuation ? Not really, but like most consumer staples, when you factor in the consistency and stability of Walmart’s core grocery and general merchandise business, consumer staple stocks tend to trade at elevated multiples.

Walmart’s free-cash-flow issue is that the Walton family doesn’t want their share of ownership to get much above 50% for a any length of time, so excess free-cash-flow, which Walmart has, doesn’t get entirely put into share buybacks as you’d think it would.

Summary / conclusion: Walmart comp’s have averaged 5.4% the last 10 quarters, although the recent quarters have been in the 4.5% range. The fascinating aspect for me about Walmart’s disclosure around earnings every quarter is that Walmart provides analysts and investors with the “average ticket” every quarter, which has to give analysts and investors some insight into general inflation since Walmart’s product categories are mostly grocery (50% – 60% of total revenue), general merchandise and health and wellness.

Walmart’s “average ticket” increase the last 6 quarters was +1.5%, while the last 12 quarters was +2.4%, so Walmart’s average ticket has been dropping, which you would think would eventually flow into government inflation data.

Will SNAP payments disrupt the quarter for Walmart ? Walmart has a sizable exposure to SNAP in the rural areas.

If the stock is down 10% after earnings Thursday, this blog would be a buyer.

The margin expansion from the new revenue streams is likely only just starting, but it would help investors too to see what percentage of revenue that Walmart Connect, Walmart Advertising and Ecommerce comprise of the overall revenue stream.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Readers should gauge their own comfort with individual stock and market volatility and adjust accordingly. None of this information may be updated, and if updated may not be done in a timely fashion.

Thanks for reading.