With Venezuela the big news over the weekend, let’s watch and see how Chevron (CVX) trades on Monday, January 5th. Chevron is thought to be the only US global integrated oil company still operating in Venezuela, at least relative to it’s original facilities. Doing a quick Grok search, it’s interesting that Venezuelan President Hugo Chavez in 2007 forced Exxon (XOM) and Conoco (COP) into joint ventures with PDVSA ( a state-owned Venezuelan oil company) which was considered the final act of the expropriation that started in the mid-1970’s, beginning under then-Venezuelan President Andres Perez.

The point being that most of the mainstream media blamed Maduro for expropriation and reducing crude oil production and exports from Venezuela, but the “nationalization” goes all the way back to the 1970’s, when the Arab oil embargo (and nationalization of US facilities in the Middle East) caused US gasoline to spike from $0.30 per gallon to $2.50 – $3.00 per gallon, when Saudi Arabia expropriated all the US crude oil facilities in the Middle East.

The bigger point being that turning on the Venezuelan oil fields might not be as easy as the Administration thinks. It might be analogous to trying to start a car that’s been laying dormant in the backyard for 20, 30, or 40 years.

In 2025, energy sector EPS fell (or is expected to fall -9.2%) with one quarter left to report, i.e. Q4 ’25, while in 2026 energy sector EPS is expected to +7.8%. The 7.8% expected 2026 EPS growth rate has come down from 17.7% in early August ’25.

You would think – and this is just my own opinion – if one integrated oil company had a leg-up on getting production started quickly in Venezuela, it would be Chevron.

——————–

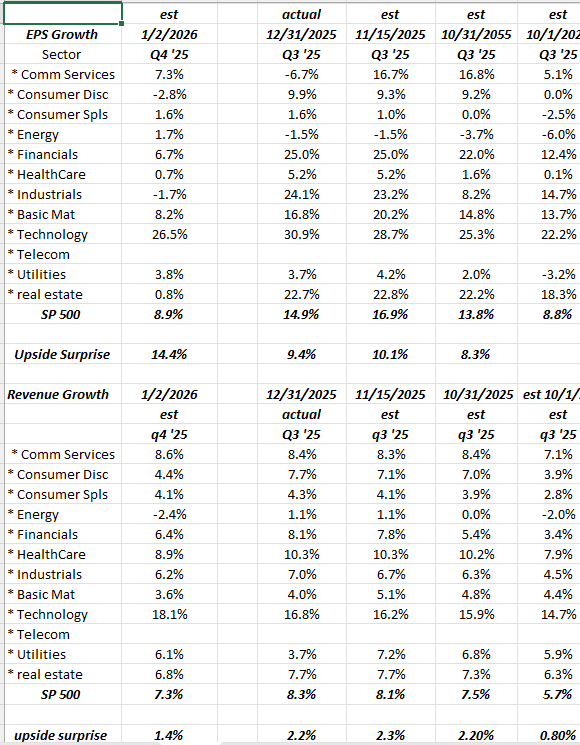

With the 3rd quarter ’25 SP 500 EPS and revenue growth now final, and we await Q4 ’25 EPS and revenue, scheduled to start next week, here’s how Q3 ’25 EPS and revenue progressed during reporting season:

Tech sector EPS grew +30.9% in Q3 ’25, while tech sector revenue growth was +16.8%.

Tech sector EPS grew +30.9% in Q3 ’25, while tech sector revenue growth was +16.8%.

The SP 500 EPS and revenue growth as a whole grew EPS +14.9%, while revenue growth was +8.3%, so “technology” basically grew 2x faster than the benchmark metrics in Q3 ’25.

To give readers some perspective on the tech sector numbers, the +30.9% was the strongest y-o-y growth rate for the tech sector since Q1 ’24 which saw a 24% y-o-y growth rate (aided by a negative comp of -8.3% in Q1 ’23). Excluding the COVID years of ’20 and ’21, the best growth rate from 2010 to 2019 for the tech sector was +36.5% in Q1 ’18 which was greatly enhanced by the tech companies being able to repatriate substantial cash held overseas, thanks to prohibitive US tax laws, which were eliminated under the TCJA (Tax Cuts & Jobs Act) signed into law by President Trump in late December, 2017. Microsoft, Cisco, and Oracle all repatriated billions of dollars held overseas for years, most – but not all of the repatriated cash – of which went into share repurchases, upon it’s return to the US.

The point being, the Q3 ’25 +30.9% growth rate was the purest rate of growth possibly since the late 1990’s, but this blog’s sector data doesn’t go back that far.

Not to spoil the tech party, but expected EPS and revenue growth for tech in Q4 ’25 – per the LSEG I/B/E/S data – is expecting (as of 1/2/26), +26.5% EPS growth and +18% revenue growth.

Those are good numbers – but the SP 500 in general and the tech sector specifically – starts to lap the tough y-o-y growth comps from 2025.

Summary / conclusion: It’s going to be interesting to see if the tech sector can generate EPS and revenue growth in Q4 ’25 that exceeds the record +30.9% EPS growth and +16.8% revenue growth seen in Q3 ’25.

There are other sectors to note too: the financial sector in Q3 ’25 saw actual EPS and revenue growth double from what was expected early in the quarter, but financials likely face tougher comp’s in Q4 ’25 since President Trump’s re-election saw sharp appreciation in Q4 ’24 as capital deregulation and pro-business policies were expected under President Trump’s 2nd term.

This secular bull market in stocks turns 17 years old on March 9, 2026. It’s getting long in the tooth. What might the tech sector trade like if tech sector EPS and revenue growth drops down to 10% and 8% respectively in the next few years ? That’s still good growth, but well below growth rates the investment community is used to seeing.

One more note: LSEG I/B/E/S had some earnings data “issues” at the end of 2025. The new “forward 4-quarter” estimate came out on January 2 ’26, but I’d prefer not to publish or comment on it until we see next week’s data on January 9th, 2026.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. All earnings data is sourced from LSEG I/B/E/S.