With Walmart (WMT) and Nvidia (NVDA) expected to bring the unofficial end to Q1 ’26 SP 500 earnings this week, last week resulted in the first sequential decline in the “forward four-quarter estimate” (FFQE) since January 16 ’26.

- The FFQE last week ended at $346.82, versus the prior week’s $347.01 and the first sequential negative week since the week ended January 16th, 2026, since the FFQE was $311.89.

- The PE on the FFQE is just 21.4x versus last week’s 21.3x and January 1 ’26’s FFQE of 22.9x.

- The SP 500 earnings yield (SP EY) as of last Friday’s close (5/15/26) was 4.68%.

LSEG’s SP 500 EPS estimate for year-end ’26 is expecting 26% EPS growth this year, but I do believe if we exclude those previously-referenced one-time gains by Alphabet and Amazon on the Anthropic private investments, as well as a one-time gain by Netflix (which was the $2.8 billion Warner Bros termination fee, which amounted to roughly $0.65 per share). Alphabet’s write-up on Anthropic was $3.01 while Amazon’s per share paper gain was $1.54 per share.

Just these one-time non-operating gains amounted to $5.20.

The current LSEG bottom-up quarterly estimate as of 5/15/26 was $74.62 so excluding the one-time paper gains by Amazon and Alphabet, and the termination fee from Netflix, the quarterly bottom up EPS estimate is $69.42 divided by Q1 ’25’s $63.07 leaves benchmark followers with just a 10% y-o-y EPS growth rate for the quarterly estimate, while the “expected ’26 annual EPS estimate) and the “expected” y-o-y growth rate for SP 500 earnings is likely closer to 22% than 28%.

Still quite healthy, just not as robust as originally thought.

Treasury curve:

The above-spreadsheet which a reader can click on to expand, shows the remarkable curve-steepening last week, probably due to Kevin Warsh assuming a Federal Reserve Board position and the Fed Chair. Alan Greenspan was tested after assuming the Federal Reserve role from Paul Volcker, and Ben Bernanke wound up in the middle of the so-called Great Financial Crisis in 2008, two years after being appointed.

The bond vigilantes are beginning to stir.

A resolution Iran and a re-opening of the Strait of Hormuz would likely assuage inflation fears if WTI crude oil would drop below $75 per share stay there.

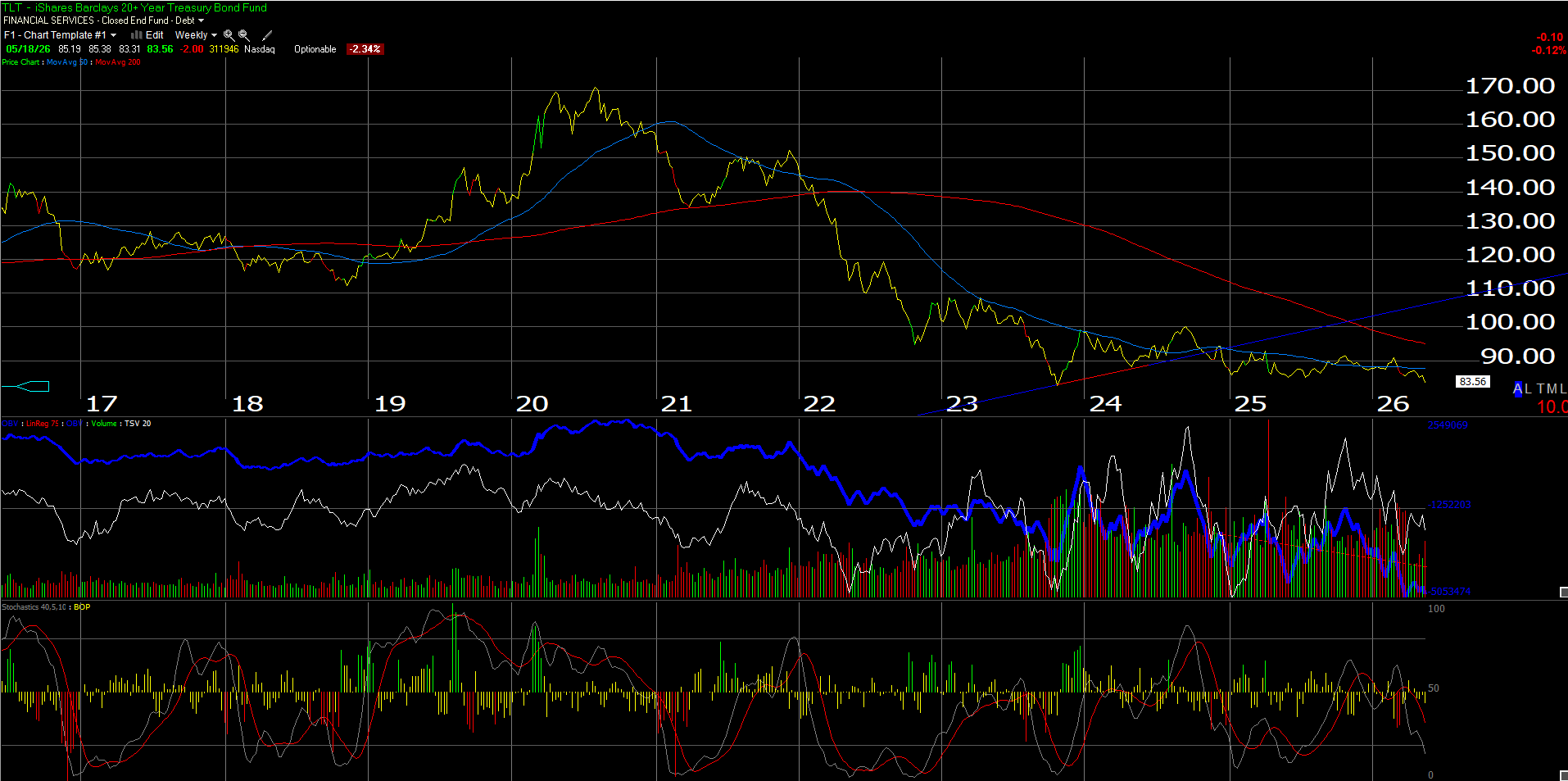

TLT (iShares 20-yr + Treasury ETF getting oversold):

Hope readers can discern the moving averages on this TLT weekly chart as of last night’s, 5/19/26, close.

A close below $80 – $82 wouldn’t be good, and we don’t want the 10-year Treasury yield to move above 5%.

The temptation here is to dump duration, but let’s see how Treasuries and corporate high-grade bonds respond to Warsh’s initial comments.

Watching credit spreads, both corporate high-yield and corporate high-grade – particularly high-grade – have absorbed the corporate bond issuance by the hyperscalers even as free-cash-flow declines y-o-y on capex spend.

Summary: Simply cleaning up some prior issues that needed addressing. None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results.

A Walmart earnings preview will be published before Walmart reports it’s Q1 ’27 quarterly earnings report this Thursday morning, May 21, ’26.

Thanks for reading.