The optics aren’t the best but these “annual return” updates run every few months can show how distorted long-term returns can get and where the value might be if readers want to look where the crowd isn’t.

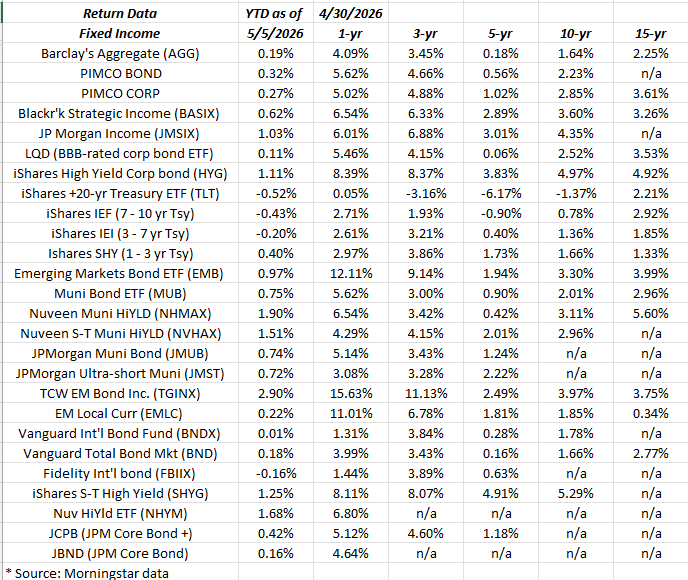

Emerging markets income is having a good run. There’s good yields abroad and with a weaker dollar and the EM central banks seemingly more willing to reduce interest rates than the Fed, EM bond markets have put up some decent returns.

Muni’s are starting to make a comeback: muni’s have been dead money for 18 months thanks to a Republican President, House and Senate, and a nice tax bill that gave some of the federal tax money to American’s, but if the Democrat’s win big in the House come November ’26, (which is what usually happens), muni’s and high-yield muni’s might start to work.

High-yield muni bond funds and ETF’s typically have very long durations – much longer than corporate bond funds and ETF’s – so be aware of that. But that long duration would be a plus if crude oil heads back down towards $60 per barrel, under a Kevin Warsh Fed.

With the OBBB tax bill clearly putting a bid under the US economy, corporate bonds – even investment-grade corporate bond funds and ETF’s – are a place to hide out until the end of 2026.

Default rates for high-yield corporate credit remain in the 2.5% – 2.7% annual pace, so a high-yield ETF like the HYG (iShares HighYield Credit ETF) and the SHYG (iShares 0-5 yr HighYield Credit ETF) with SEC yields at 6.45% and 6.47% are a great place to “clip coupons” as Blackrock’s Rick Rieder mentioned on his recent Thursday morning bond and market call (although not specifically about high-yield).

Recession odds are very low here – have to think most sell-side economic models have less than a 20% probability over the next 12 months – so the TLT and Treasury returns don’t look great, but that will change.

This blog has been a little too bullish duration over the last 18 months. Thought we’d see a fed funds rate closer to 3% by now.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. All return data cited above is from Morningstar. None of this information may be updated and if updated may not be done in a timely fashion.

Thanks for reading.