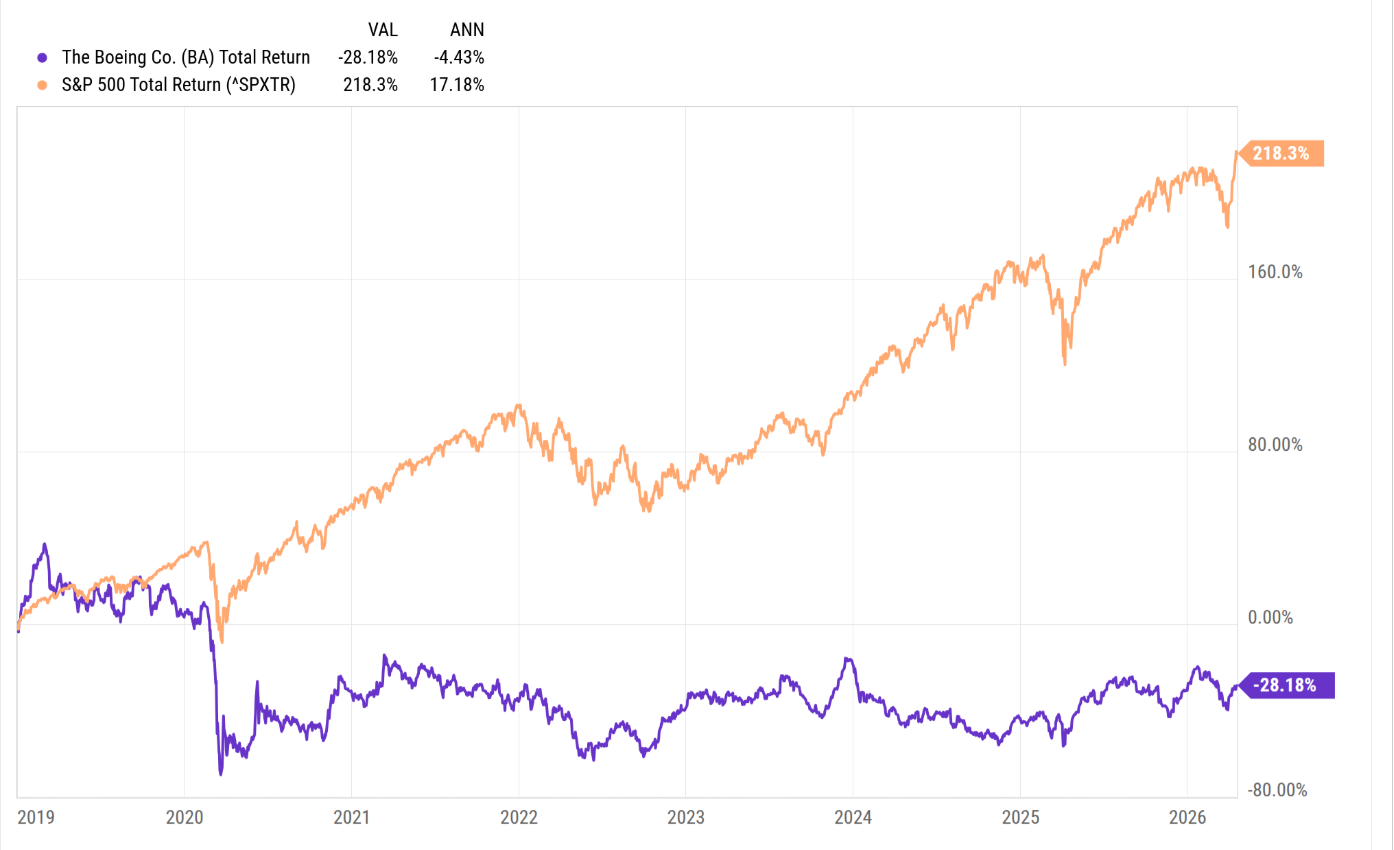

Boeing (BA) has been a frustrating long, but after an 18-year plus secular bull market in the SP 500 (bottoming on March 9th, 2009), the primary reason it was added to client accounts was that the stock has dramatically underperformed the SP 500 since it’s $446 all-time-high in March, 2019, and thus if the secular bull market should eventually run out of steam, BA’s non-correlated status to the SP 500 might be the kind of stock that would outperform in a bear market.

As you can see from the above Y-charts graph, in terms of BA’s performance relative to the SP 500, the airplane manufacturing giant continues to lag the SP 500, versus it’s early 2019 peak price.

When BA reports Q1 ’26 results before the opening bell on Tuesday, April 22nd, ’26, sell-side consensus is expecting a loss of ($0.86) per share on $21.89 billion in revenue and operating income of $270 million for expected y-o-y growth in revenue of 12%. You’d think that would be quite healthy as Boeing moves back toward it’s “peak revenue” of $102 billion in 2018 (BA printed $89.4 billion in total revenue in 2025), but it’s not seeing anywhere close to that in margins or EPS growth or cash-flow growth, which is likely a function of the FAA keeping production limitations on the aerospace giant, and Boeing not being able to “leverage” it’s manufacturing prowess. BA operates under the same principle as GM, or Intel or any other massive manufacturer, i.e. the ability to drive widespread volume over a fixed cost base is when EPS, and margins, and cash-flow really improve dramatically.

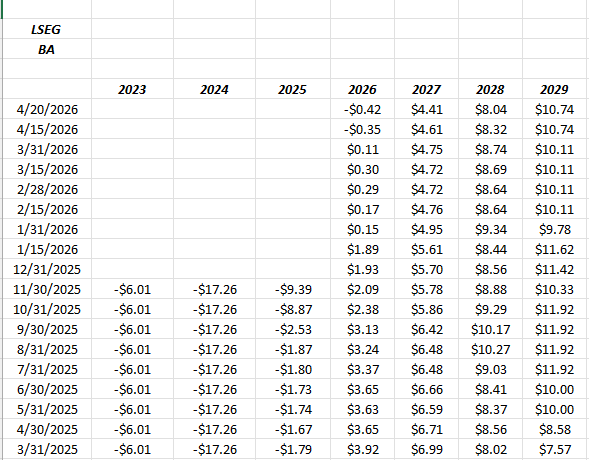

BA EPS and revenue revisions:

From looking at the forward EPS estimates courtesy of LSEG, BA looks like a 2028 story, although the stock would likely discount that EPS improvement well in advance, and much would depend on what’s happening with margins and cash-flow.

BA’s revenue estimate revisions have improved slightly with the aerospace giant expecting new “peak revenue” next year in 2027, surpassing 2018’s $102 billion.

As a quick summary of the preview for Tuesday morning’s results, Jefferies put out a short preview note, saying Q1 ’26 deliveries were 143 aircraft, versus the 130 expected. Morningstar noted after the Q4 ’25 results that BA will likely deliver 564 737 planes in 2026, versus the actual 2025 737 deliveries of 447.

My own comment is that GAAP financial accounting for BA is a mess, and the only relevant valuation metric for BA is the just over 2x revenue valuation is at least in the historical framework as well as the expected revenue growth for BA in ’26, ’27, and ’28 of 9% respectively.

Morningstar has had a good bead on BA’s valuation at $250 per share, which has been close to “peak price” for BA in 2021, late 2023, and early 2025.

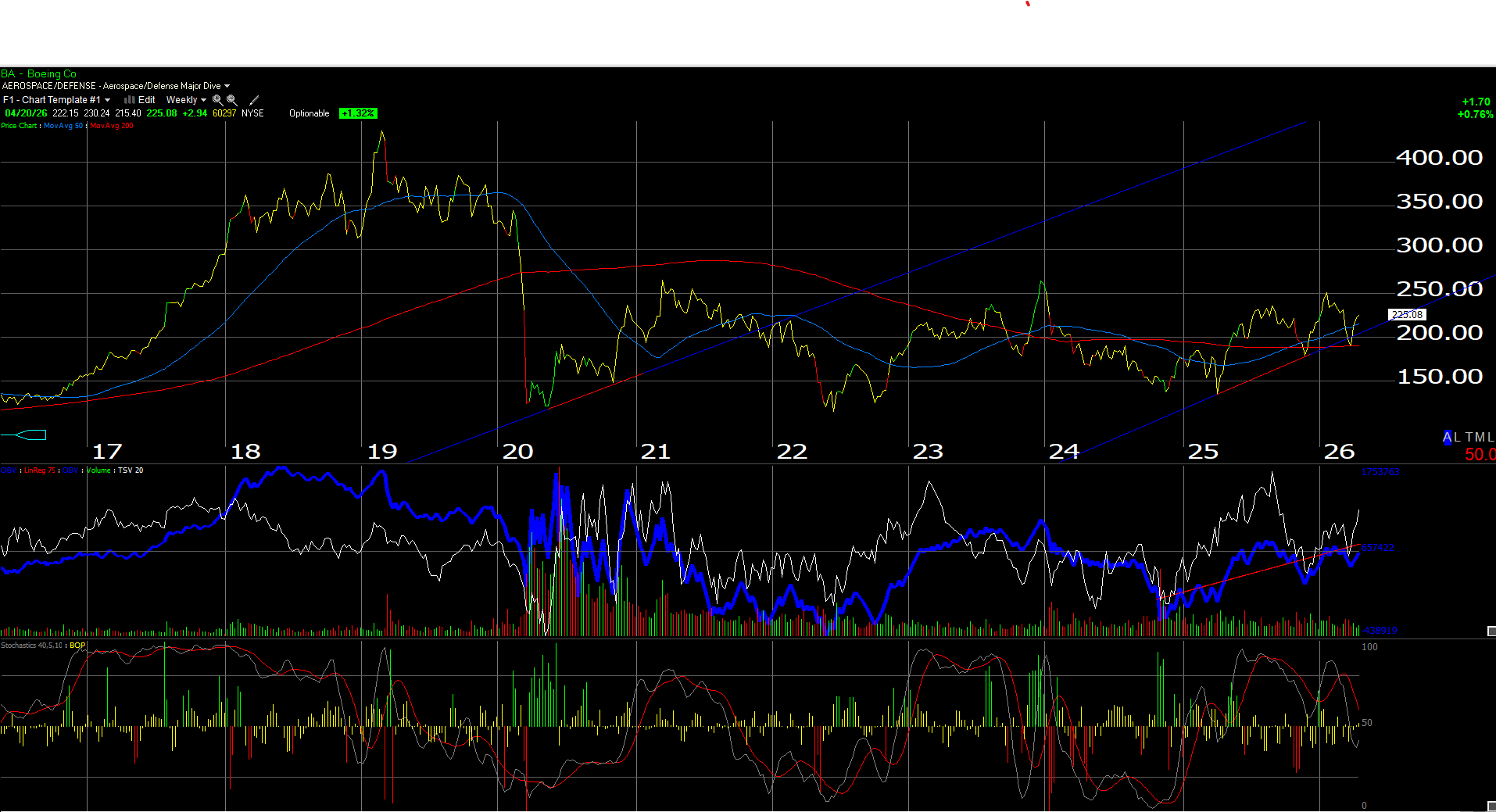

Coming into earnings tomorrow, BA is holding it’s 200-week moving average technically, with a lot of negative news around the stock, which is usually a plus, but management comments on the FAA loosening the grip and allowing BA to improve manufacturing pace would be very well received (and probably very unlikely).

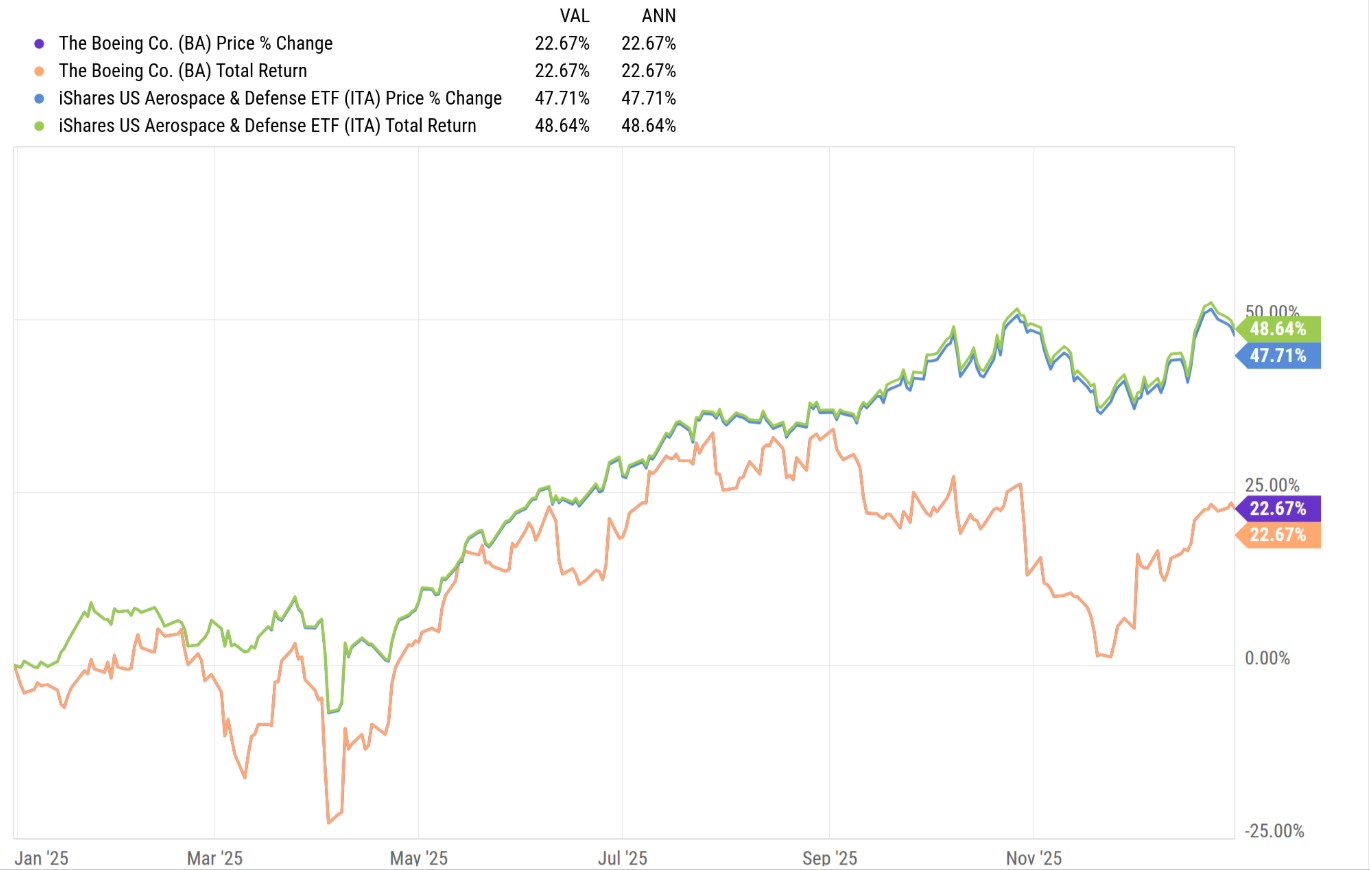

If BA just continues not to work, a possible swap into the ITA (aerospace / defense ETF) would be an option since the next Trump Administration defense bill is looking for a significant spending increase. In 2025, BA rose 22.88% beating the SP 500, while the ITA rose 53.54% per the Y-Charts graph below.

Boeing’s investment story today is “how patient can you be ?” in terms of owning the stock.

IBM earnings preview:

When IBM reports Wednesday afternoon, April 22nd, 2026, the sell-side consensus is expecting $1.81 in EPS, $15.6 billion in revenue and $2.6 billion in operating income for “expected” y-o-y growth of 13%, 7% and 16% respectively.

With Q4 ’25 IBM had a fairly good quarter, (the 4th quarter for IBM is typically their strongest of the year), when IBM announced the AI book has risen to $12.5 billion, $2 – $2.5 billion greater than Q3 ’25. Software rose 14% and is growing as a percentage of IBM revenue, and maybe more importantly has not been impacted by the “SAAS-pocalypse” that has impacted the rest of technology.

IBM has really been trying to reinvent itself since the earlier part of last decade, and looks like Arvind Krishna and his team may have done that since the stock traded above it’s April, 2013 of $215 per share in the 4th quarter of 2024, and hasn’t looked back since.

As the LSEG EPS estimate revisions indicate, IBM is showing steady increases in EPS estimates the last 12 months, which is exactly what you’d like to see as an investor.

IBM is still trading with a free-cash-flow yield of 5% at $258 per share, while the stock’s multiple of 21x and 19x is a little rich given the expected EPS growth of 7% in 2026. That being said, early in 2025, expected IBM EPS growth was looking for 6% growth, while actual 2025 EPS growth was 12%.

The above-linked article covers a lot of ground, but it’s still fascinating to me that IBM has not bought back any material stock this decade, and really since 2018 and 2019. That’s much different than IBM of the 2000 to 2009 era and again from 2010 to 2019.

As a quick conclusion to IBM’s earnings preview, as long as the AI book continues to expand at a methodical pace, and as long as IBM’s move into software won’t be crushed over AI, Arvind Krishna and the team may once again, have rebuilt and repositioned IBM as was done by previous management’s in the late 1990’s, and then again in the early 2000’s.

IBM missed almost the entire bull market from 2013 to Q4 ’24, so – like Boeing – Big Blue has that “non-correlated” aspect to the stock, Maybe even more importantly from 2000 to 2009, IBM managed to outperform the SP 500 – albeit only slightly – with a positive return.

SAAS-pocalypse has probably pushed IBM’s stock price too far down as tech stocks peaked late October ’25 and didn’t bottom until March 30 ’26.

This blog’s intrinsic value estimate for IBM is closer to $300 while Morningstar’s fair value estimate is $325.

For IBM, AI represents both opportunity and risk.

Overall conclusion: The secular bull market that we saw from 1982 to 2000, required that investors re-allocate the portfolio and invest in stocks, sectors, and asset classes that didn’t actually participate in the rally of the late 1990’s, in order to preserve wealth from the horrific bear stock that was seen by the SP 500 and Nasdaq from 2000 though well into the decade from 2010 to 2019.

IBM and Boeing represent non-correlated positions from a portfolio construction standpoint.

Readers should pay attention to what hasn’t worked for long periods of time, as much as what has worked.

None of this is advice or recommendation, but only an opinion. Past performance is no guarantee of future results. All EPS and revenue estimates for any holding mentioned are sourced from LSEG. None of this information may be updated, and if updated may not be done on a timely basis. Readers should evaluate their own comfort with portfolio volatility and act accordingly.

Thanks for reading.