- The forward 4-quarter estimate (FFQE) increased this week to $339.22, versus last week’s $338.29.

- The PE ratio on the new forward estimate is now 20x.

- The SP 500 earnings yield slipped below the recent +5% level to close the week at +4.97%, as of the 4/10/26 close.

- The SP 500 this week, closed above both it’s 50 and 200-day moving averages for the first time since late February ’26.

Financial sector this week:

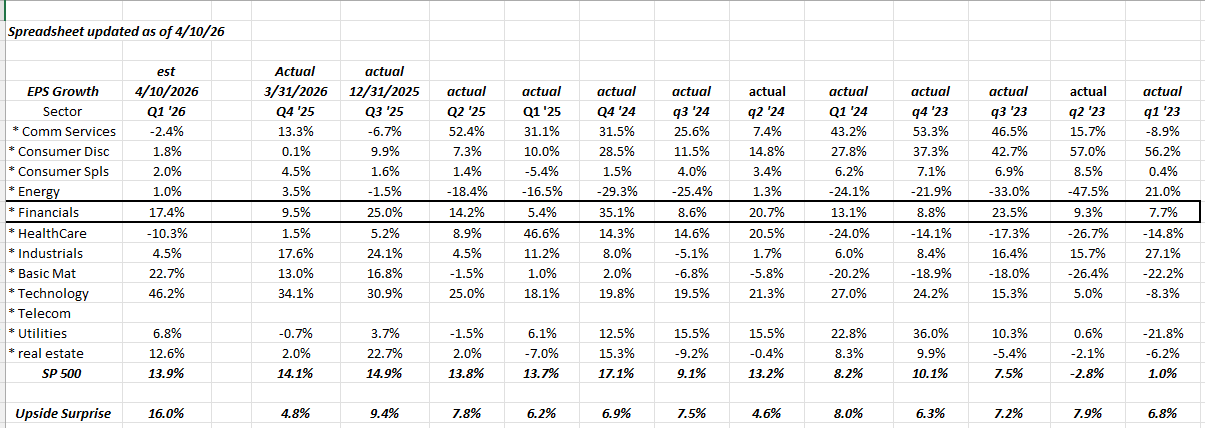

Looking at the 11 sectors of the SP 500 coming into Q1 ’26 financial results, the financial sector is highlighted for readers: the expected EPS for the financial sector for Q1 ’26, currently estimated at 17% y-o-y growth, is a smidge above the 15% average shown for the sector over the last 12 quarters, or since Q1 ’23.

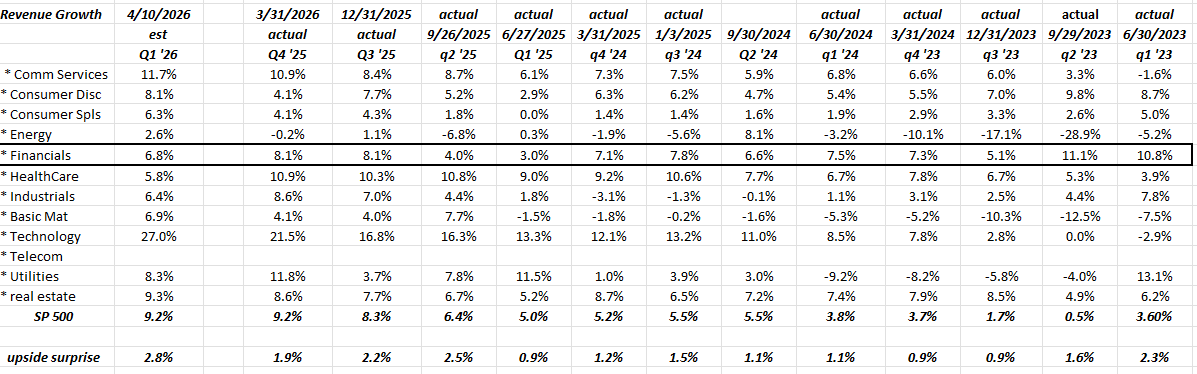

Looking at actual and expected revenue growth for financials, the average revenue growth per growth, for the sector, the last 12 quarters is 7.2%, while the estimated rev growth for Q1 ’26, is 6.8%.

Financials – at least in terms of the sector estimates – are looking for an average quarter, as Goldman Sachs (GS) kicks off results on Monday, April 13th, 2026.

Financials are the 2nd largest market cap in the SP 500, 2nd to only technology’s, 33.8% as of Friday, April 10th, per the LSEG data.

The one interesting aspect to the financial sector numbers, is that Q1 ’26 is lapping a pretty weak quarter in Q1 ’25. In Q1 ’25, the financial sector EPS growth was just +5.3%, while actual revenue growth was just +3%.

While this blog expects the Q1 ’26 actual results to be healthy, since Iran was just one month of the Q1 ’26, how management’s address “linearity” in the quarter (i.e. how was March ’26 relative to January and February ’26, and what changes were noticed), particularly in bank credit areas like consumer and industrial lending, and of course “private lending” and to what extent the banks are having issues with their private credit books. (I have to note it was interesting to see – using some Bespoke data – that it appears publicly-traded, high-yield credit spreads tightened last week, which was unexpected given the news of continued issues around private credit.)

Goldman Sachs:

Goldman Sachs (GS) is scheduled to report their Q1 ’26 financial results before the opening bell on Monday, April 13th, hence readers won’t get any opportunity to buy or sell the stock during open market hours before the financial results are released. JPMorgan (JPM), Citigroup (C) and Bank of America (BAC), report before the open Tuesday, April 14th, so this blog will be out with previews on these earnings in the next 24 – 48 hours.

Goldman’s consensus estimates per LSEG data are $16.9 billion in revenue, $6.5 billion in pre-tax operating income and $16.49 in EPS, for expected y-o-y growth of +12%, 15%, and 17% respectively.

Goldman noted in their Q4 ’25 results that the investment banking backlog was up for the 4th quarter in a row in Q4 ’25, when Goldman printed 11% revenue growth, 11% pre-tax income growth and 17% EPS growth. With the potential AI deals coming down the road in ’26, SpaceX (if in fact Elon Musk does choose to take SpaceX public), and the Fannie (Fannie Mae) / Freddie (Freddie Mac) IPO’s still in the wings, there are some potentially big IPO’s in the pipeline, and you’d have to expect Goldman will be involved with all those deals.

Goldman’s valuation remains reasonable at 15x and 14x expected 2026 and 2027 EPS of $58.26 and $65.09, for expected EPS and revenue growth in 2026 and 2027 of 14% and 12%, and 9% and 5% respectively. Goldman’s book value (BV) and tangible book value (TBV) are in the 2.5x category, which is well above the 2010 – 2019 decade when the stock traded mostly around book value of 1x.

One last valuation point: in late 2021, Goldman traded up to $400 and at that point it was trading at 7x trailing-twelve-month (TTM) earnings of $60 per share. Readers need to remember this was a full two years after the Fed reduced the fed funds rate to zero, SPAC’s were in full swing, bitcoin and crypto also dominated the news, Congress passed the $2 trillion bailout package for middle-class America after the economy was shut-down, and “liquidity” was the name of the game.

As of Q4 ’25, Goldman’s TTM EPS are just $53.66 per share, the stock is at $900, and the PE multiple on the stock (TTM EPS) is 17x.

Goldman is very sensitive to changes in market liquidity and capital market conditions, so know what you own. TTM EPS for Goldman fell to $20 in TTM EPS in 2022, after the Fed raised rates numerous times during that year.

Summary: Unfortunately this blog sold Goldman Sachs too early, with clients having no positions currently in Goldman, but note how the move in the stock since late, 2021, has been entirely “PE expansion” rather than earnings-driven stock performance. The former banking giants like Goldman and Morgan Stanley (MS) have very volatile EPS streams, primarily thanks to the economic sensitivity to the US economy, although there has been some stability added after the post-2008 financial reforms eliminated proprietary trading. As the wealth management businesses grow, the EPS growth should become more stable and predictable.

The financials that report this week should show decent results for Q1 ’25, but listen for the linearity on the conference calls in terms of how the quarter progressed and if there were any major changes to capital market conditions, like credit, liquidity, etc.

If Monday morning, April 13th finds the US and Iran have re-opened the Strait, and all is copacetic again within the Middle East, the January 28th, 2006 high for the SP 500 of 7.002.28 comes back into focus.

The Dow hit 50,000 and retreated and the SP 500 hit 7,000 and retreated. My own expectation is that 2026 will be a tougher year for stock returns, particularly large-cap returns, after the last 3 years for the SP 500 of double-digit returns.

2026 SP 500 expected sector EPS growth rates continue to rise, even this latest week, and after the 4 – 5 weeks of Iran-filled headlines.

Let’s see if actual results back up the estimates.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Readers should gauge their own comfort with portfolio volatility and act accordingly.

Thanks for reading.