Boeing (BA) the airline manufacturing giant that is ordinarily the envy of the world, and one of only two airline manufacturers across the globe (AirBus being the other), reported their Q1 ’26 financial results on Wednesday morning, April 22nd, 2026, and while the results weren’t great, the results do indicate Boeing is slowly moving forward with aircraft construction and deliveries, but may not hit “peak” output until 2028.

According to Jeffries, free-cash-flow (FCF) was “the star of the quarter” even though FCF was still a loss of ($1.4 bl) so cash-flow-from-operations was likely better-than-expected at just a loss of ($179 ml). Jefferies also noted that the Max-7 and Max-10 certification are coming in 2026.

From a valuation perspective, Morningstar noted that half of BA’s enterprise value will come from the 737, thanks to its higher-margin. Morningstar expects the 737 to return to 2018-level production by late 2027, which is just 18 months away.

This blog’s analytic update noted that with Q1 ’26 results BA’s price-to-sales has fallen under 2x to 1.93x.

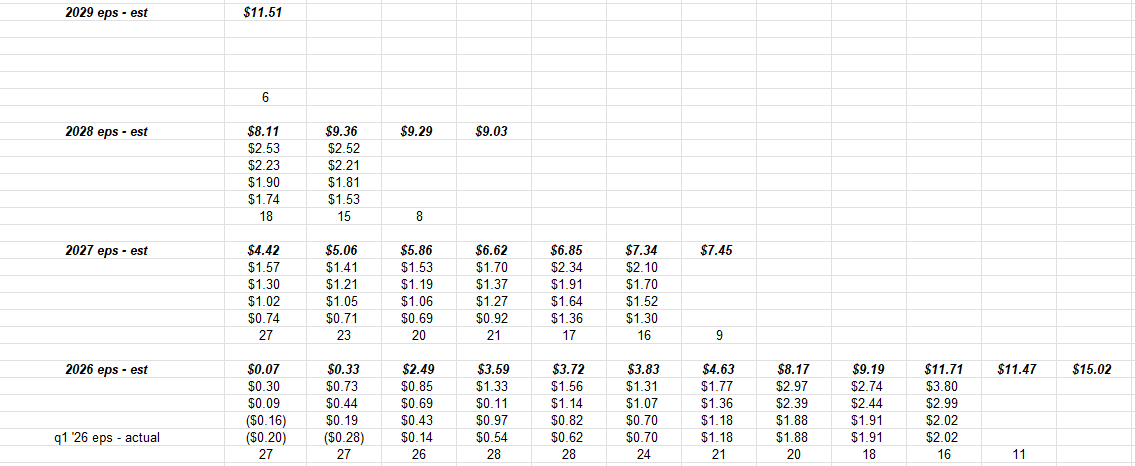

Looking at forward BA EPS estimates, readers can see how it’s 2027, but really 2028 where the delivery leverage will likely in for BA, and shareholders will likely see operating margin growth, and cash-flow and free-flow growth.

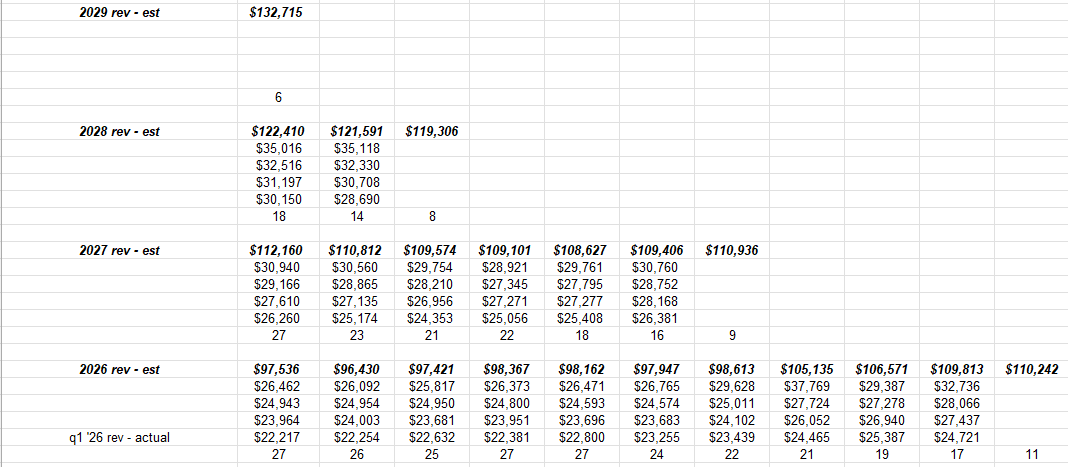

BA’s forward revenue estimates reflect the fact certifications and FAA relief on deliveries per month continue, which will help BA’s revenue estimates. 2027 revenue estimates continue to rise even though the 2027 EPS continue to reflect pressure. (You wonder why Kelly Ortberg looks so grim every time he’s on CNBC.)

BA summary: even though BA’s GAAP financial statements look grim, BA will print record record revenue sometime in 2027, surpassing the previous $102 – $103 bl peak late last decade. Also, BA (the stock) beat the SP 500 in 2025 (as discussed in the earnings preview last week), and is ahead of the SP 500 in 2026, up 7% YTD versus the SP 500’s 4.99%. (Performance data from Morningstar.)

This blog will likely keep BA for now in client accounts, although that can change at any time. It’s interesting that the ITA (Aerospace & Defense ETF) peaked exactly when the US and Israeli planes struck Iran (weekend of Feb 28, ’26) and has now pulled back to it the ITA’s 200-day moving average at $215.80. The only reason the ITA is brought up is that BA is now it’s 3rd largest position at 10% of the ITA ETF, where it was the 5th or 6th largest position several months ago.

Peak Boeing for this blog would be full aircraft production and an operating margin that starts to exceed 10% – 12%. But BA absolutely cannot have a another mid-flight mishap, or crash, with attribution coming back on Boeing. A slow and steady recovery will look good for BA and the stock should start to discount it, probably sooner than readers might think.

IBM:

IBM actually had an OK quarter, but what they failed to mention on the earnings call Wednesday night, April 22nd, 2026, after IBM reported their Q1 ’26 financial results, was whether further progress on the AI book was made.

This AI progress was specifically-noted in this blog’s earnings preview because IBM has talked about it on every conference call since last fall ’25.

Even the Goldman Sachs analyst James Schneider asked the IBM CFO Kavanaugh on the conference call last Wednesday night, ” I was wondering if you could comment on the AI bookings – which is a metric you’d previously given – but I think you just commented as a percentage of your total bookings right now. ”

The CFO James Kavanaugh gave a detailed and expanded answer to Goldman’s analyst question, without really commenting specifically about “the AI book”. The answer talked more about how AI was now layered across several different parts of the portfolio, as if to say to the analysts “we can’t exactly tell how much AI is driving product growth.” (My words, not theirs.)

That’s never good when a company stops disclosing specific information like that, but the Morningstar analyst did note that IBM’s issues within software were not because of AI.

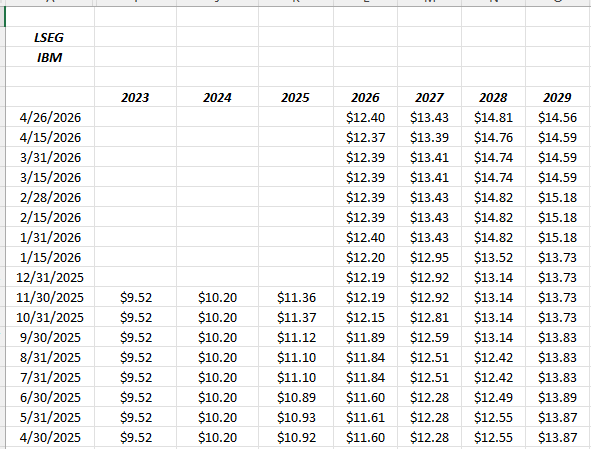

Readers should note that IBM’s forward EPS estimates did continue to increase after the Wednesday night conference call, albeit with some disappointment around software and disclosure.

Also, since IBM just maintained 2026 guidance at > 5% cc revenue growth, and at least $1 bl in free-cash-flow, perhaps analysts were disappointed guidance wasn’t improved for ’26. (cc stands for constant currency).

IBM summary: not wild about the tempered discussion of AI and it’s influence on the “IBM book” but we’ll have to see if this gets quantified further in July ’26. So far, IBM’s stock is being held although that can change. The stock is down 22% YTD as of Friday, April 24th’s market close, well below the SP 500’s +4.99% YTD return. Was the AI influence over-hyped by IBM ? Is there a way IBM can benefit from the AI buildout ?

The benefit of the doubt will be given to IBM for now, although the stock at $232 per share is trading just $17 above the April, 2013 peak between $213 – $218, and is down from the fall ’25 peak of $325 per share. The stock price action is telling investors that not much has changed yet from the Spring, 2013 peak price.

Hope all this helps. None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future results. All EPS and revenue data is sourced from LSEG. Readers should evaluate their own comfort with portfolio volatility and adjust accordingly. None of the above information may be updated, and if updated, may not be updated in a timely fashion.

Thanks for reading.