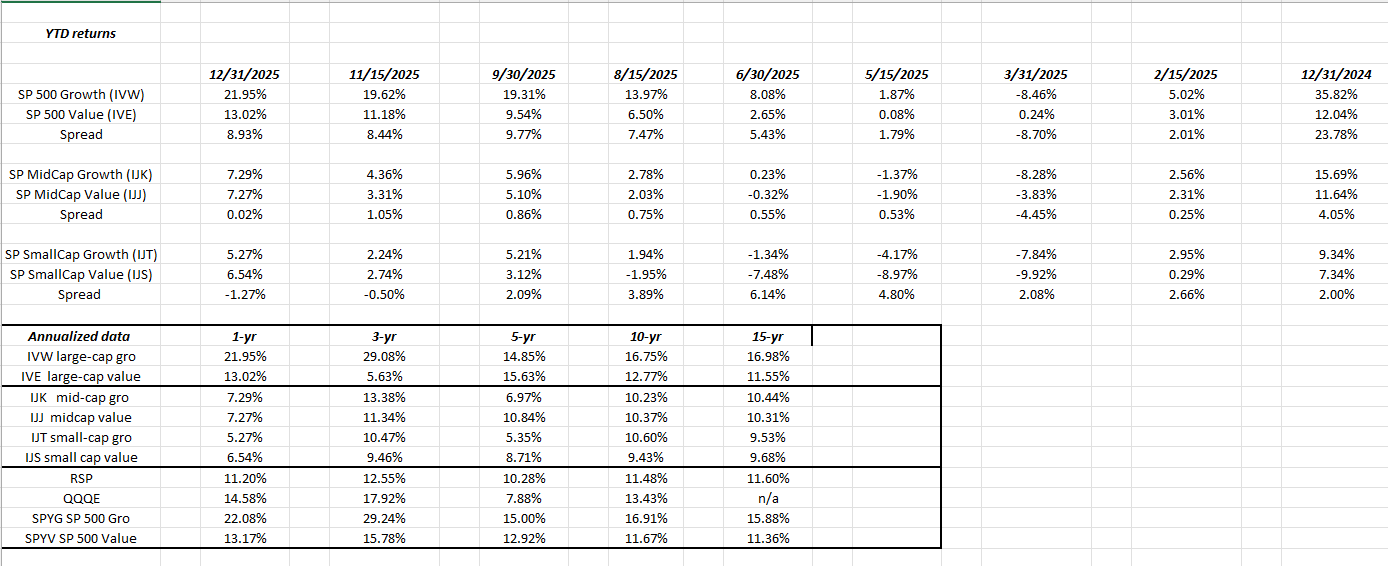

(Click on spreadsheet to enlarge)

Readers know that every 6 weeks, the “style-box” update is posted to this blog.

What’s interesting about the 12/31 data is that – for the first time since 2022 – “value” has started to outperform “growth”, and it’s started in the small-cap asset class.

Look at the third section down in the above spreadsheet and note how “small-cap value” has outperformed small-cap growth since 11/15/2025.

Again, “growth” has smoked “value” for the last 12 quarters in terms of total return and growth beat value across all three asset classes (large-cap, mid-cap and small-cap) for those twelve quarters, until this last quarter of 2025. In the 6 years from 2020 to 2025, value only beat growth during the Covid-afflicted years of 2021 and 2022.

Is it a meaningful shift ? Don’t know yet. Does it portend a broader change in style performance for the broader equity market ? Don’t know yet.

But, growth has outperformed for a long period of time, without value beating the growth returns, until this last quarter in small-cap.

It certainly bears watching, particularly as commodities are really heating up, including the oil and gas sector after the Venezuela events of last weekend.

International had a breakout versus the US in 2025.

All this is evidence of the shifting landscape in the broader equity market performance picture.

Summary / conclusion: Again, it’s probably too early to draw a conclusion that would warrant a tectonic shift in portfolio positioning towards small-cap value, but the growth outperformance trend may be starting to wane, which could impact the major indices like the SP 500 and Nasdaq.

Another update will be forthcoming in mid-February ’26.

None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future results. This data will likely be updated around mid-February ’26.

Thanks for reading.