(Click on spreadsheet to enlarge. Annual return data from Morningstar.)

This spreadsheet analysis which is typically posted to the blog shows that “value” investing is clearly outperforming growth investing.

Last Q1 ’25, during the Liberation Day correction, the same thing happened, but once the stock market bottomed in early April ’25, growth investing started to resume it’s former leadership.

This time – or rather in Q1 ’26 – there is no external catalyst to explain the reversal from growth to value.

When the last Style-Box Update was written on January 6th, with year-end ’25 returns and annual returns as well, value was just starting to creep up on growth returns in Q4, ’25.

The January 6th, ’26 post does suggest with international starting to outperform in ’25 that “all this is evidence of the shifting landscape in the broader equity market performance.”

As the old saying goes, ‘things are a changin’ but let’s not dramatically overreact.

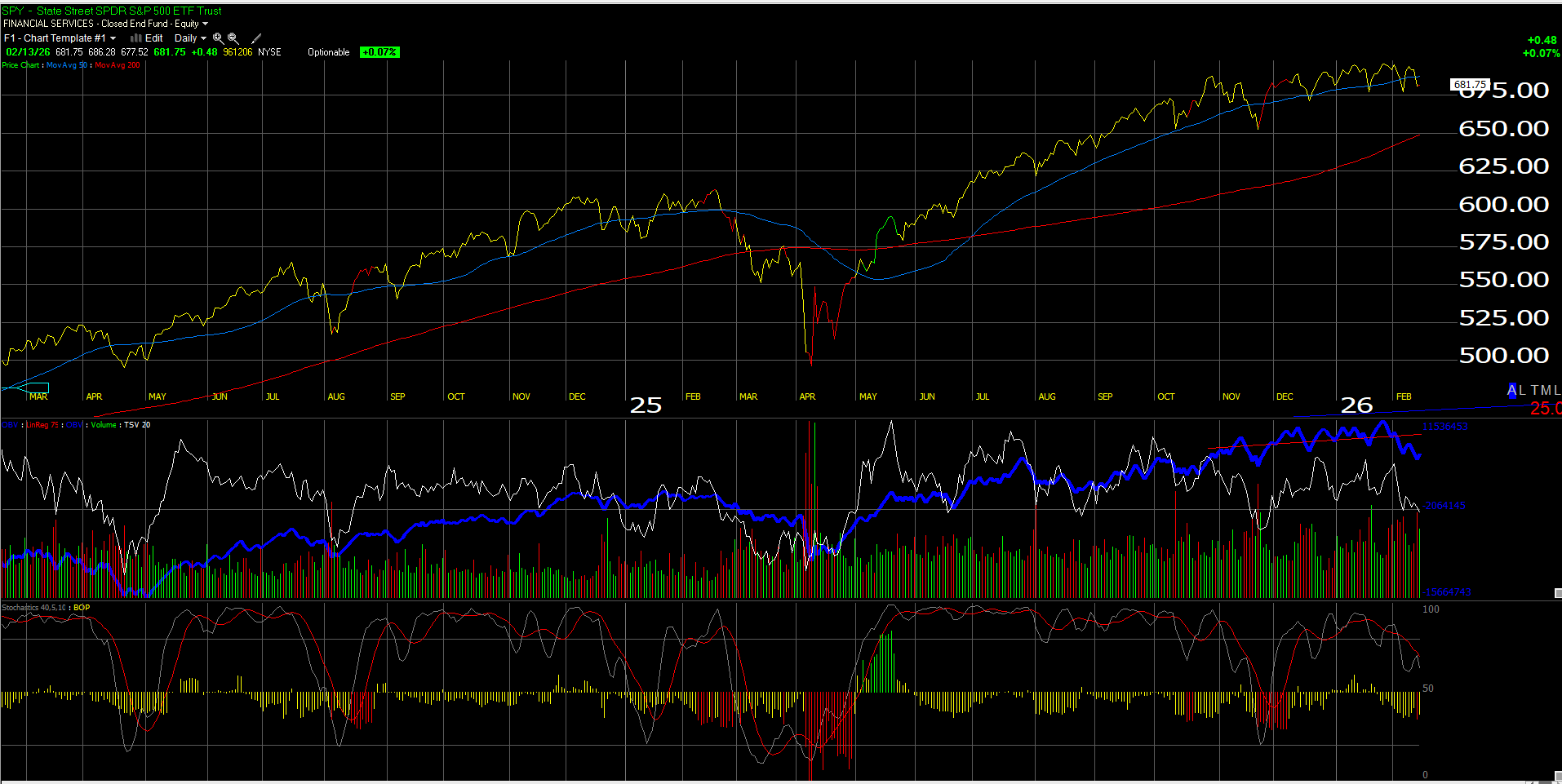

The SP 500 and Walmart:

This daily chart of the SP 500 from Worden shows the key benchmark in the early stages of getting oversold, but it was more oversold last November ’25.

The SP 500 still has not taken out the 7,000 level. Not a shock given the performance of the Mag7 / 10 stocks, and now the outperformance of value across the style-boxes.

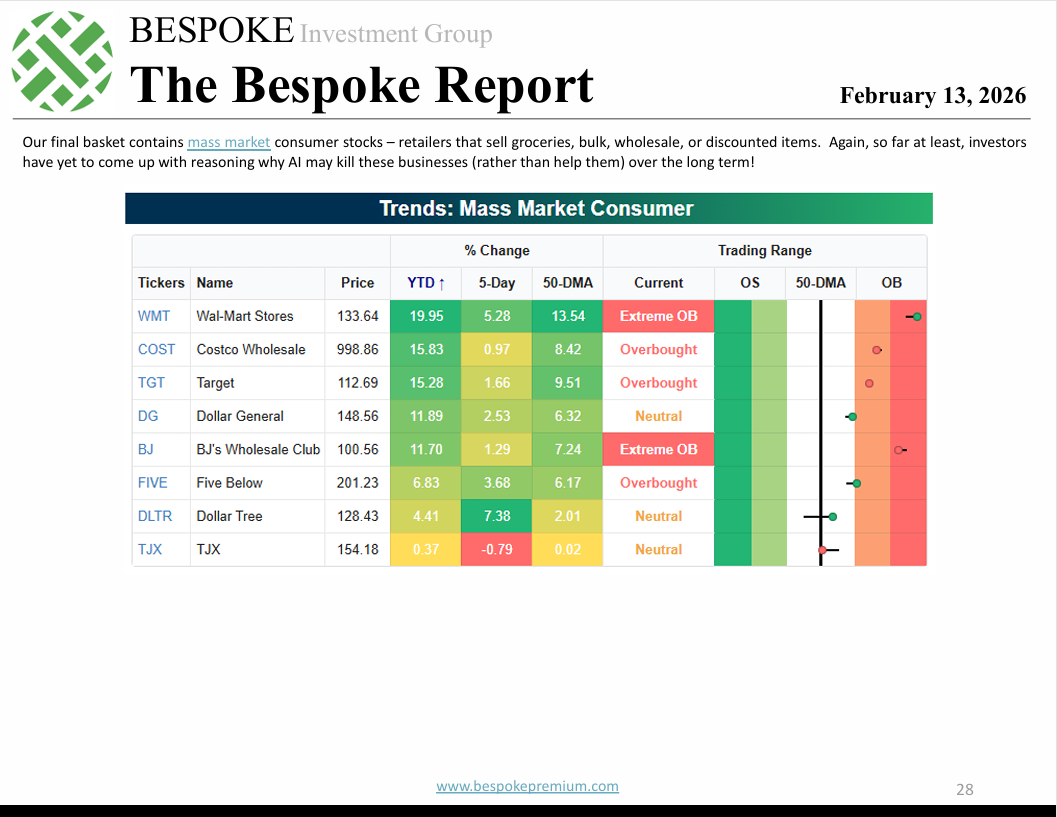

Walmart (WMT) reports Thursday morning, February 19th, 2026 before the opening bell. The consumer staples sector has been on fire, led by Walmart and Costco. Costco (COST) bottomed two days before Christmas on December 23, ’25, and has run from $843 to close at $1,018 last Friday, February 13th, ’26.

Here’s a table from Bespoke’s weekend report dated February 13 ’26, which shows the extreme overbought nature of Walmart and the whole staples sector.

A reader asked a question if I were thinking of selling any Walmart before earnings, and in fact some Walmart was sold prior to this coming Thursday’s earnings report. It’s a guess but there is still probably 75% – 80% of the original WMT position being held, and more partial positions might be trimmed this week. The addition of Walmart to the Nasdaq 100 index really brought some accumulation into the stock after that announcement.

Summary / conclusion: The style box analysis confirms the relative outperformance of value vs growth across the market caps, but the question is how long does it last, and just how much “alpha” can value generate vs growth, given it’s long period of underperformance.

Consumer staples stocks always sport “growth valuations” given the consistency and dependability of their revenue, operating income and EPS results. Coke (KO) missed when they reported their Q4 ’25 results, the stock dropped a little following, but then ramped sharply from $72 to close at $78 last Friday, being pulled along by the staples burst of momentum. Walmart will be an important tell this week. (Earnings preview will be published.)

The mega-caps, the “growth trade” (including larger-cap banks) and the market leadership the last 4 years was due for a break, and the continued enormous capex builds around AI have given the former market leadership pause.

Even international and emerging markets are overbought, and the dollar is oversold (long JPMorgan Int’l Value, i.e. JFEAX and JIVE), the emerging markets ex-China (EMXC) ETF, and some Japan (EWJ ETF).

A reversal trade from here will see the old leaders rally, and the “new leadership” correct. That will be the litmus test for the new trade.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Clients and readers should gauge their own comfort with portfolio volatility and adjust accordingly. None of the above information may be updated, and if updated may not be done so in a timely fashion.

Thanks for reading.