While Fed Chairman Jerome Powell adhered to the Fed’s stated policy of “slower economic growth with expected higher inflation” yesterday at his Congressional testimony, there is no question that the sentiment is shifting within the Federal Reserve for an easier monetary policy, in the coming months.

While the President Trump-appointed Fed Governor’s Barr and Bowman have started becoming more vocal about the need for the Fed to lower interest rates, what convinced me was Austan Goolsbee’s, the Chicago Federal Reserve President’s comments from Monday, June 23rd, where he noted that thus far, the surge in tariffs has had a more modest impact on the economy relative to what was expected. The exact quote was “somewhat surprisingly, thus far the impact of tariffs has not been what people feared.”

I thought it unusual that Austan was so direct, for what was clearly an “easier monetary policy” comment.

Austan Goolsbee was appointed by President Obama to be the chairperson of the Council of Economic Advisors during President Obama’s presidential tenure, thus this opinion is likely not borne of partisan sentiment.

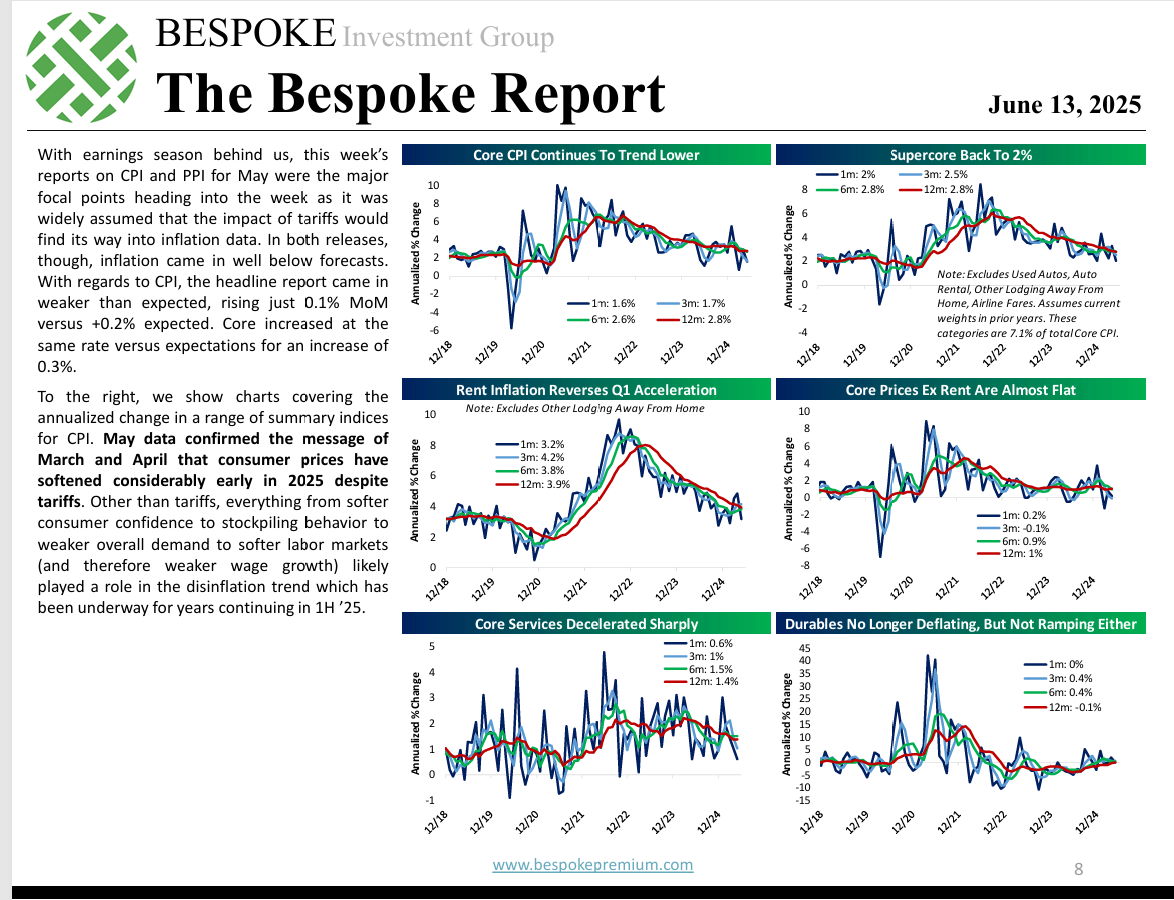

Inflation Charts:

Click on the above Bespoke Report page and note the Core Services inflation chart in the lower left-hand corner of the page.

Services inflation has been an issue since 2022 – 2023 when overall CPI peaked in the 9% area, with services inflation being much slower to recede to the 2% – 3% than goods inflation over the last few years.

However, services and shelter inflation have finally started to cooperate with the Fed’s restrictive monetary policy.

Summary / conclusion: Last year Jay Powell and the FOMC reduced the fed funds three times, by 50’s bp’s the week of September 20th, 2024, by 25 bp’s the week of November 8th, 2024, and another 25 bp’s the week of December 20th, 2024.

At the time, Jay Powell and the FOMC noted ( I thought) that the fed funds rate at 5.375% was unduly restrictive in terms of monetary policy, and (I thought again ) suggested that at 4.375% where it stands currently, was still restrictive.

The 2-year Treasury today trades with a yield of 3.80%, while the fed funds rate is still stuck at 4.375%, which is suggesting the Fed / FOMC is right about monetary policy’s impact.

When Treasury Secretary Bissent was playing good cop to the President’s bad cop in early April ’25, he said specifically to pay attention to crude oil: my impression was that the Trump Administration wanted crude lower ( mid $50’s ?) given it’s inflation and consumer purchasing power implications, but it would allow the Fed to lower rates mainly to start to lower interest expense on Treasury debt, which is now the single-biggest line-item of the budget deficit.

With the hysteria around tariffs, and Israel – Iran, and the rest of the media noise, the bigger picture remains the record budget deficit (as it sits in the background like the 800 pound gorilla in the corner of the cage), which ultimately needs to be dealt with. Moderate Republicans supposedly came out yesterday and said that they were pushing back on the Medicaid cuts. That’s not great news for the deficit-reducers.

There is still the probability that the budget bill will not lessen the budget deficit, and that’s the shorter and longer-term issue now.

That may be why investors are more bullish on the short-end of the Treasury yield curve than the long-end of the curve.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results.

Thanks for reading.