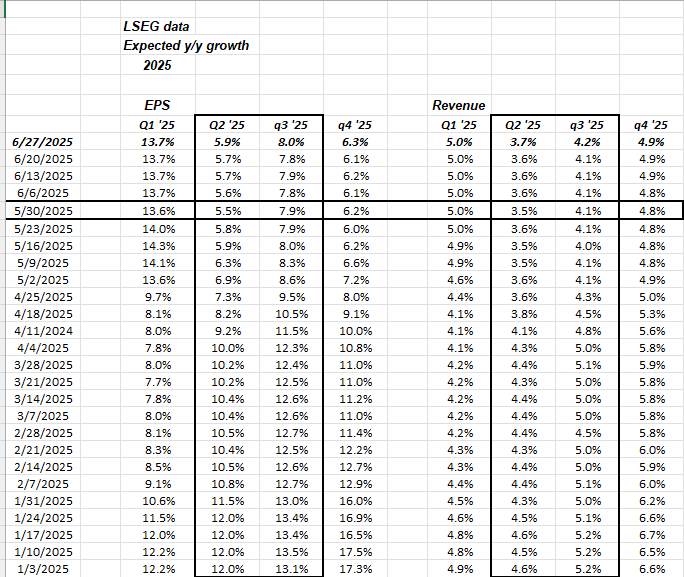

If you look at the above bordered line running horizontally across the page, it appears that as of the Memorial Day weekend, the expected quarterly EPS and revenue growth rates for the SP 500 bottomed, and have started to improve since then.

We’ll see what July 8th – July 9th holds in terms of the President’s plans for “reciprocal tariffs”.

Last night Nike announced $1 billion in expected tariff costs, which amounts to about $0.67 in EPS.

The President announced a trade deal around rare earth minerals, under the headline of a trade deal today, but it’s unclear if there is anything different on the tariff front.

Interest rates and monetary policy:

The entire Treasury yield curve – the 10-year maturity and earlier – is now below the current targeted fed funds rate of 4.375%.

That’s the yield curve telling the FOMC they are behind the curve.

The Fed is always late though, and so-called data dependent.

Here’s the interest-rate related blog post from earlier this week.

Crude oil below $60 will also put pressure on the FOMC and their current monetary policy stance.

Credit spreads:

High-yield credit spreads tightened this week, again, and investment-grade spreads remained at the same level they’ve been trading at, well down from the early April ’25 highs.

On a weekly close basis, this blog has the high-yield credit spreads (using an average) peaking at +425 – 430. This week the high-yield spread looks to have closed around +304.

The all-time-tights, I believe are around +350’ish, so credit is pretty fully-valued here, but unless a recession is looming, the plan is to stick with an overweight in credit, offset with a TLT long.

Summary / conclusion: Typically, after individual companies report earnings, I wait 24 – 48 hours before looking at the forward EPS changes to see how the analysts have changed their models. Nike guiding to an expected $1 billion tariffs this fiscal year was a first, so watching how EPS estimates change for fiscal ’26 and later will tell me how that fits with what analysts modeled.

Q2 ’25 SP 500 earnings start in two weeks, and the above spreadsheet shows that the SP 500 EPS estimate for the 2nd quarter has been slowly improving. Maybe tariffs do turn out to be a big nothing.

There is the June payroll report next Wednesday, the day before the 4th of July holiday. The labor market has remained relatively firm and has given the FOMC and Jay Powell little reason to reduce the fed funds rate.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. None of this information may be updated, and if updated, may not be done in a timely fashion.

Thanks for reading.