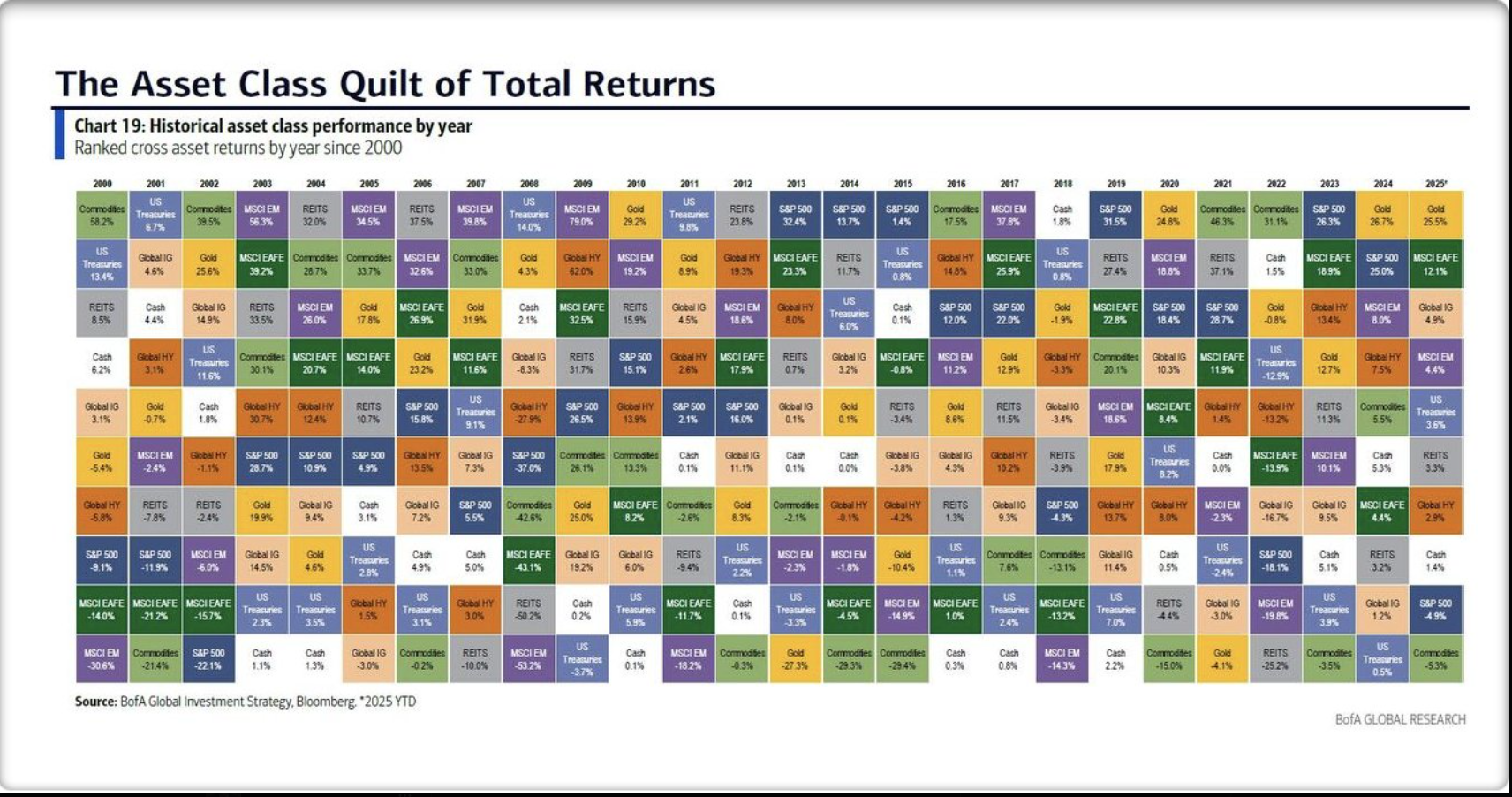

The above asset-class return quilt was posted to X late last week by FinGenAI (@ackmeni), and is originally sourced from Bank of America research.

It’s clear that long-dormant asset classes have started to lead the capital markets. Gold is the leader this year, after not having performed well since the 2011. Gold was a stellar performer from 1999 – 2000 through 2011, after falling from $800 to $200 from 1980 to 1999, so you can make the case that gold is negatively correlated to the SP 500, but there also appears to be some negative correlation to the US dollar as well, i.e. when the dollar is weaker, gold tends to find a bid.

Another way to be long gold exposure is owning companies like Newmont Mining (NEM), but you have an operating company sitting on top of a what is a precious metals producer, so you get more than just a simple long to the metal. An investor has operating risk in addition to commodity risk. In the year 2000, and after, to get gold exposure for client portfolios, you had to be long companies like Newmont, or the miners, since the Gold ETF (GLD) wasn’t launched until December, 2004.

Is this move temporary or permanent ? The move in international is probably more longer-lasting, without the “binary” result from the March, 2000 top in tech and large-cap growth. In other words, there is certainly a world where both the SP 500 and the international Ex-US could perform quite well together, but the historical average returns for international are likely to provide more alpha than the traditional US-centric portfolio going forward (in my opinion). When large-cap tech and growth peaked in March, 2000, and international funds, and value funds, and small-mid cap funds took off, large-cap growth and tech were dead money for years. Looking at this blog’s recent post on SP 500 annual returns, the 25 year annual return for the SP 500 is just 7%, while the annual returns since January 1 ’22 are still mediocre, which likely means any flat to down market for the SP 500 and strictly US investments can still generate mediocre to healthy returns.

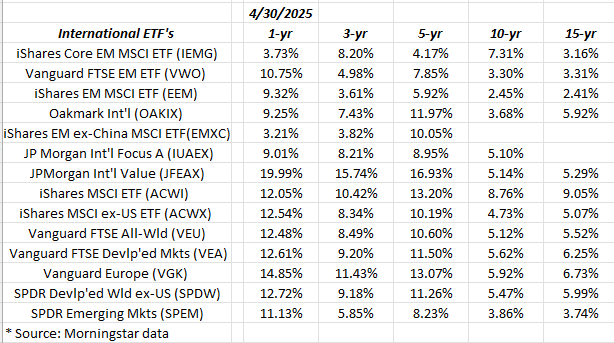

International returns:

Since investing is a probability-based business, updating the annual returns this weekend, here’s how a number of international funds and ETF’s look (in term of annual returns) as of April 30, ’25:

Source: Morningstar annual return data

Readers might have other international ETF’s and mutual funds that they like, and prefer, but these are the 14 that I update monthly (in terms of the annual return) with the intent to add to some single-country funds like India and Vietnam, as well as some single countries in Europe as well.

Europe is having a nice run: it’s clear Europe has moved to center-right versus center-left after the immigration debacles, although UK has moved the opposite direction with Stermer’s ascension to Prime Minister.

There is no question international returns have begun to improve in the last 12 months.

Summary / conclusion: In Bob Dylan’s “Forever Young” ballad, there is a line in the song that says, “May you have a strong foundation when the winds of change shift” and correlating that to the investment game, when long-dormant asset classes start to generate alpha, pay attention.

This blog’s three – four largest non-US positions for clients are the JP Morgan International Developed Value Fund (JFEAX), the Emerging Markets ex-China (EMXC) ETF, and the VEA ETF or the Vanguard FTSE Developed Markets ETF (VEA), as well as the VGK (Vanguard FTSE Europe) with the JFEAX having a little more euro and British pound exposure (6 of 10 top holdings), while the VEA has a little more pound and a little less euro exposure.

A few clients are also long David Herro’s Oakmark International Fund (OAKIX).

It will get pushback, but China – in my opinion – is un-investable. The EMXC and the VWO / EEM did a get a little bounce on Friday, with China signaling to the US that they are interested in talking tariffs with the US (finally), but when Jimmy Lai (pronounced Lee), was tried for treason by China for continuing to publish his pro-democracy Apple News Daily in Hong Kong, every single VWO position was sold from client accounts.

Lai was put on trial starting in 2020, but the issue began to get some press in the latter half of the last decade, which is when all the VWO was sold for clients, and – at least according to Google – Jimmy Lai remains in solitary confinement in a Hong Kong prison today.

China remains a communist country. There are far easier ways to create wealth for your clients.

Here’s a bunch of articles (here, here, here and here) written in the 2nd half of 2024, suggesting that readers pay attention to international annual returns. (Never mentioned gold though, and long just a small amount.)

In one of the linked articles above, I mention that with international returns, a lot of the attribution is about the dollar, and it’s relative strength or weakness with other currencies. Both David Kelly, JPMorgan’s Chief Global Strategist, and Rick Rieder, Blackrock’s Global Fixed Income CIO, thought the dollar was overvalued, in their updates around the early April, 2025 market lows. What that portends for gold is a likely positive, but for international annual returns it’s a definite plus, not to mention the same opinion coming from two of the best strategic minds in the business.

While many might think of 2025 as a difficult equity market, like post March, 2000, it’s just a different equity market. Long dormant asset classes are starting to outperform. That’s not a bad thing.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Investing can involve the loss of principal even for short periods of time. None of the above information may be updated and if updated may not be done in a timely basis. Readers should gauge their own comfort with portfolio volatility and adjust accordingly. All annual return data above is sourced from Morningstar.

Thanks for reading.