The point of the title of this blog post is meant to persuade readers not to abandon international equity investing, despite the 4.5% rally this past week in the SP 500 and the sharp rally in the US dollar. (This blog’s dollar proxy is the UUP ETF, which was up just +0.68% last week, but has risen +2.5% in the last 30 days.)

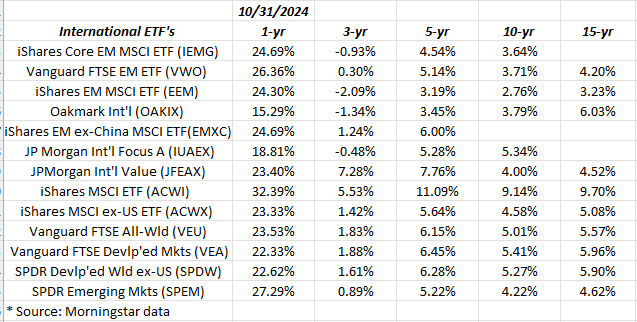

The above spreadsheet is the annual returns from a handful of mutual funds, and ETF’s across international and emerging markets.

Those are surprisingly good 1-year returns for an asset class that’s all but been ignored for the last 15 – 18 years.

Now look at the above international 3-year returns.

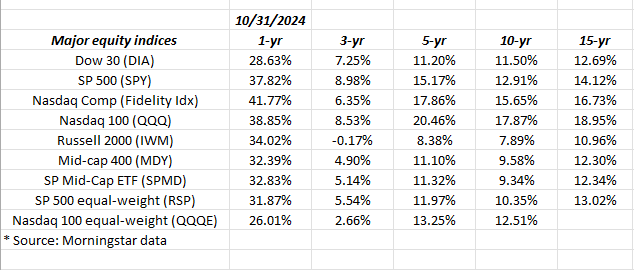

The above chart is US indices and their rolling annual returns.

The real value in international (in my opinion) is the notable discrepancy between the 10-year and 15-year US indices annual returns, and the same 10-year and 15-year annual returns for international equity indices, mutual funds and ETF’s.

JPMorgan’s international portfolio manager for their JIRE ETF (International Enhanced Equity ETF) held a lunch in Chicago last week, and I asked the team if they had ever seen 10 and 15-year international equity returns this low, and the immediate answer was “no”, but then the discussion quickly moved in another direction.

To give readers some perspective, when the large-cap growth and tech market topped in March, 2000, it resulted in an immediate rotation into asset classes that had remained dormant in the late 1990’s, i.e. value investing, small and mid-caps, and notably, international equities. The rally in international lasted for 7 years, as the SP 500 and the Nasdaq fell 50% and 80% respectively between March, 2000 and early 2003.

I had friends and acquaintances in the investment management business in the late 1990’s when clients would call up screaming at them about why more technology wasn’t owned (in the late 1990’s it was the Microsoft / Intel / Cisco triumvirate, (and GE too) that was driving the SP 500 higher).

Hate this blog to use too many cliches, but as the old saying goes, “history doesn’t repeat itself precisely, but it often rhymes”.

Summary / conclusion: The remarkable aspect to the JP Morgan lunch is that there is so little interest in the asset class, I thought it was remarkable for a notable bank to showcase that asset class, particularly after the Wednesday, November 6th rally, and the prospects for even higher SP 500 returns in 2024.

My guess is that the capital flows that would drive relative outperformance in the international asset class, are probably still pretty subdued given the relative performance in the SP 500 and Nasdaq indices. In other words, the “hot” capital is likely still flowing to the mega-caps and the market-cap weighted indices.

Part of writing this for readers is to force the analysis to remain disciplined as a portfolio manager, and reinforce the reasons to keep a position in an underperforming asset class.

Client’s largest international equity position is the JPMorgan International Developed Value Fund (JFEAX), which replaced the Oakmark International Fund (OAKIX) in late summer ’24. However David Herro’s Oakmark International will be owned again, probably after January 1 ’25, to diversify the international space, and really in response to this latest missive and the ongoing secular bull market in US equities.

Remember, the business school/investing maxim isn’t just about about “risk vs reward” but also about “correlation”.

You don’t want to learn that lesson the hard way.

None of the above is a recommendation or advice, but only an opinion. Past performance is no guarantee or even suggestion of future results. Investing can and does involve the loss of principal, even for short periods of time. None of the above information may be updated, and even if it is updated, may not be done so in a timely fashion. Readers should gauge their own comfort with their own portfolio volatility and adjust accordingly.

Thanks for reading.