1-year annual returns for a number of the bond market asset classes slid lower in November ’24, thanks primarily to the strong stock market rally after the re-election of President-elect Trump, but also thanks to the stronger dollar, also reacting to the Presidential election results.

As of 11/30/24:

- The SP 500 (SPY) YTD total return: +27.97%

- The Barclays Aggregate YTD total return: +3.05%

- A balanced 60% / 40% portfolio YTD total return: +18%

Although it’s a tough compare to a 28% SP 500 TYD return, a +18% YTD return for 2024 is a pretty good return.

International:

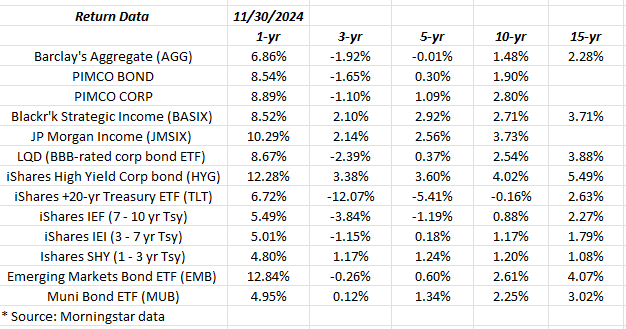

Click on the above table / spreadsheet and note the 1-year annual returns for international on 11/30/24, versus 10/31/24 and then 9/30/24. (NOte the bordered boxes.)

International – thanks to the strong dollar – had one of it’s worst months versus the US equity indices in quite a while, as readers can see from noting the 1-year annual returns as of 11/30/24 versus the same 1-year annual returns as of 10/31/24.

The good news around international (if there is any) is that the 1-year annual returns as of 11/30/24, after that horrid month for international returns, are about where they were on 8/31/24.

For international, it’s (usually) all about the dollar.

Summary / conclusion:

Typically at annual client meetings, the client will always talk about what hasn’t worked or the (what I call) “the holes in the portfolio”.

The recession that has been forecast since early 2022, or almost three years now, is nowhere in sight, and even less likely if the President-elect and the new Congress will pass pro-growth tax initiatives, which I personally think could be a tough sell with the size of the budget deficit today.

The Treasury yield curve is trying to steepen, but has really just flattened, as the 2-year Treasury yield closed tonight at 4.18% while the 10-yaer closed at 4.22%.

Even if the FOMC reduces the fed funds rate by 25 bp’s to 4.375% on December 18th, ’24, the Treasury yield curve will still be or is likely to be still inverted from the fed funds to the 10-year Treasury yield, but it will be a much smaller inversion.

Bond returns could remain paltry for a while, and the whole “tax/tariff/DOGE” initiatives of the new Administration could complicate portfolio construction.

None of this is a recommendation or advice, but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal, even for short periods of time. This information may or may not be updated and if updated, may not be done so in a timely fashion.

Thanks for reading.