The announcement that Pat Gelsinger “retired” on December 1st, 2024 came as a surprise this morning, and at first the stock rallied sharply on the news, but eventually the stock rolled over with a few hours left in the trading day and closed in the red, on heavier-than-average daily volume.

Following the stock quarter-in, and quarter-out since 1995, it’s been remarkable to watch the developments of Intel. The recent CHIPS Act and the government grant of – what – $3 billion, and also the Defense Department contract, still couldn’t kick-start the chip giant and get it moving in the right direction.

If you want to see some spreadsheet stats that – more than any of the others (in my opinion) symbolize Intel’s downfall, note the following:

Quarterly y-o-y revenue growth:

- 4-quarter avg: +3%

- 12-quarter avg: -9%

- 20-quarter avg: -4%

- 40-quarter avg: +1%

- 50-quarter avg: +1%

Capex growth (y-o-y and trailing 12 months):

- 4-quarter avg: +10%

- 12-quarter avg: +18%

- 20-quarter avg: +12%

- 40-quarter avg: +11%

- 50-quarter avg: +10%

Operating cash-flow growth (y-o-y and trailing 12 months):

- 4-quarter avg: -3%%

- 12-quarter avg: -25%%

- 20-quarter avg: -11%%

- 40-quarter avg: -2%%

- 50-quarter avg: 0%

Just compare and contrast the operating cash-flow growth versus the capex growth.

The difference – some of it anyway – was made up by issuing long-term debt. As of the 9/30/24 quarter, Intel had $46.5 billion of long-term debt outstanding, versus $25 billion as of December, 2019, and just $2 billion as of June, 2011.

Here’s some articles written for Seeking Alpha on the topic of Intel over the years.

- January, 2014: https://seekingalpha.com/article/1945791-intel-earnings-preview-a-truly-busted-growth-stock-or-something-else

- April, 2015: https://seekingalpha.com/article/3067036-intel-earnings-bad-news-baked-in-but-one-longer-term-problem

- April, 2016: https://seekingalpha.com/article/3965969-ibm-intel-earnings-previews-dying-slow-painful-death-business-model-transformation

- August, 2020: https://seekingalpha.com/article/4371102-intels-ceo-bob-swan-is-right-fabless-intel-is-fabulous-for-shareholders-why

- February, 2023: https://seekingalpha.com/article/4577258-intel-tough-road-ahead-stock-not-made-new-low

Writing (for me anyway) is really a form of research, and it imposes a discipline that forces an investor to follow the fundamentals.

Over the last 15 years I’ve been alternatively bullish and bearish on the stock, thinking at some point a CEO or management team could turn it around.

In my opinion the most interesting of the above articles is the August, 2020, “fabless” take. Some of the reader comments are very interesting and are relevant to today’s announcement.

By the way, Nvidia is considered a “fabless” GPU producer. It’s cash-flow statement shows very reasonable capex relative to operating cash-flow and revenue generation.

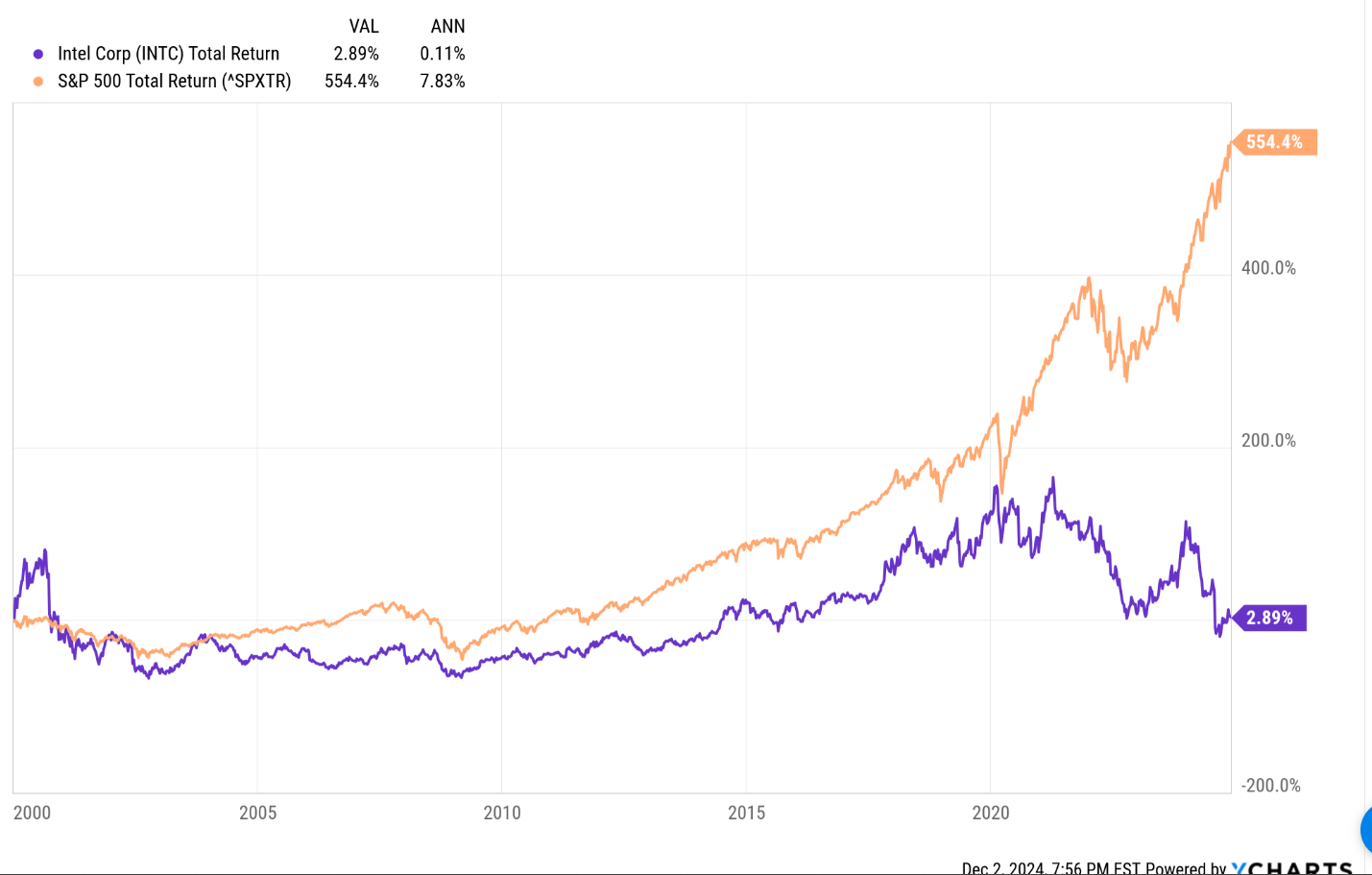

Performance chart:

This is a pretty grim performance chart for Intel’s stock over the last 24 years.

Summary / conclusion:

The general consensus is that Intel missed a lot of opportunities over the last 25 years including mobile, foundry, etc. and never tried to reduce the capital intensity of the business as Texas Instruments (TXN) did after the 2001 – 2002 bust, and that stock has performed admirably over the same time period.

Intel needs to find some sustainable revenue growth, and also needs to figure out a way to reduce that capex drag. The expression has been used before on this blog, but spending $10 to $15 billion per year of your operating cash-flow on greenfield fabs is like running the proverbial marathon with a piano on your back.

The positives around Intel are that $18 – $20 should be good support for the stock. This blogs favorite technician is Gary Morrow (found on X at @garysmorrow, and he likes the stock at these levels at 15-year lows. Another plus is that – after being jettisoned from the Dow 30 – stocks actually tend to perform pretty well. (Ryan Detrick over at Carson Group has written about this over the years.)

This blog holds no Intel positions for clients currently, but with new management, maybe there’s still a chance for the ’90’s chip giant.

None of this is a recommendation or advice, but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal, even for short periods of time. This information may or may not be updated and if updated, may not be done so in a timely fashion.

Thanks for reading.