Barrons (www.barrons.com) had a good article (subscription may be required) on the prospects for 2025 stock market returns this weekend, and it echoed or used the same logic as this blog’s November 10th ’24 article from a weeks ago. That being said, so many similar themes and conclusions are rehashed constantly in the financial media, ownership is fungible at best.

The stock market bulls are still mainly bullish and the bears are still mainly bearish, if not more so, with the latest reason this week, the overwhelmingly bullish sentiment being seen by retail investors.

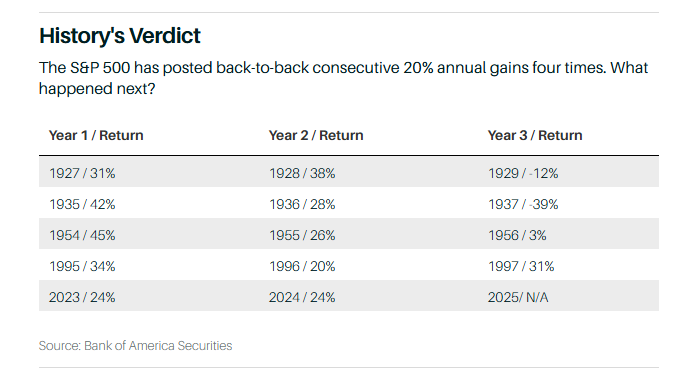

This table above from the Barron’s article is supportive of my November 10th, ’24 article linked above, where that blog post mentioned that it was only in the 1995 – 1995 period during the last 5 years of the Clinton Administration (and the Republican Congress), that the SP 500 returned more than 20% per year, mor than 2 years in a row, and that was for 5 consecutive years.

The last two years have seen siginficant PE expanion, while 2025 may see “PE contraction” where the market is up in 2025, and has a positive return, but the return is less than the +13% expected EPS growth next year.

It could happen under the Trump Administration, but, given history, the odds are against a 3rd year of +20% returns in 2025.

Could there still be a positive year of returns for the SP 500 ? Sure, absolutely in fact, if the President and Congress can cut the corporate tax rate to 15% or even 17%, it would likely lead to an increase in the SP 500 EPS for 2025, currently forecast at $275.07 next year, up 13% from the current 2024 SP 500 EPS estimate of $243.79.

Back in 2016 – 2017, President Trump’s election was a big surprise, and the Tax Cuts & Jobs Act (TCJA) wasn’t actually signed into law until late December, 2017. Here’s the impact the tax cut had on SP 500 EPS:

- 2018 SP 500 EPS: $161.93 for +23% y-o-y growth

- 2017 SP 500 EPS: $132.00 for +10% y-o-y growth

- 2016 SP 500 EPS: $118.10 for +1% y-o-y growth

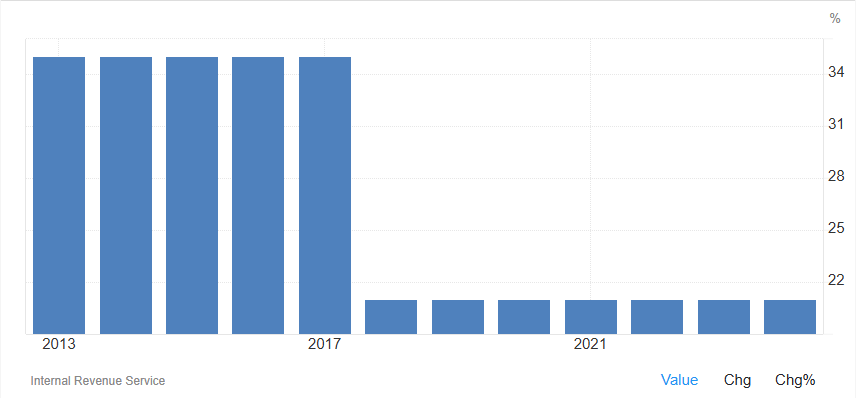

Here’s a table of the US corporate income tax rate from the Obama years through the present:

Under the last 4 years of the Obama Administration, the US corporate income tax rate (statutory, not necessarily the effective rate), was 35%, but with the Tax Cuts & Jobs Act passed in late 2017, it was reduced to 21%, and the fact is with the Republican Senate and House it could be reduced further in 2025, but the substantial US deficit and the growing pushback on the budget deficit might make reducing tax rates of any kind – personal or corporate – very difficult in the next year.

Of the two tax cuts to be had, ordinary income (i.e. personal) or the corporate tax rate, I still think the corporate tax rate would most likely be reduced – if only marginally – in 2025, and that might get cut only to 17% – 18%.

The deficit and the interest due on the Treasury debt outstanding, are going to make formidable arguments for tax cuts of any kind, but if President Trump can get it done, it would likely be in 2025.

Summary / conclusion: as the November 11th blog post details for readers, the Trump economy versus the Trump stock market (and let’s not forget the bond market either), may be two different stories in 2025.

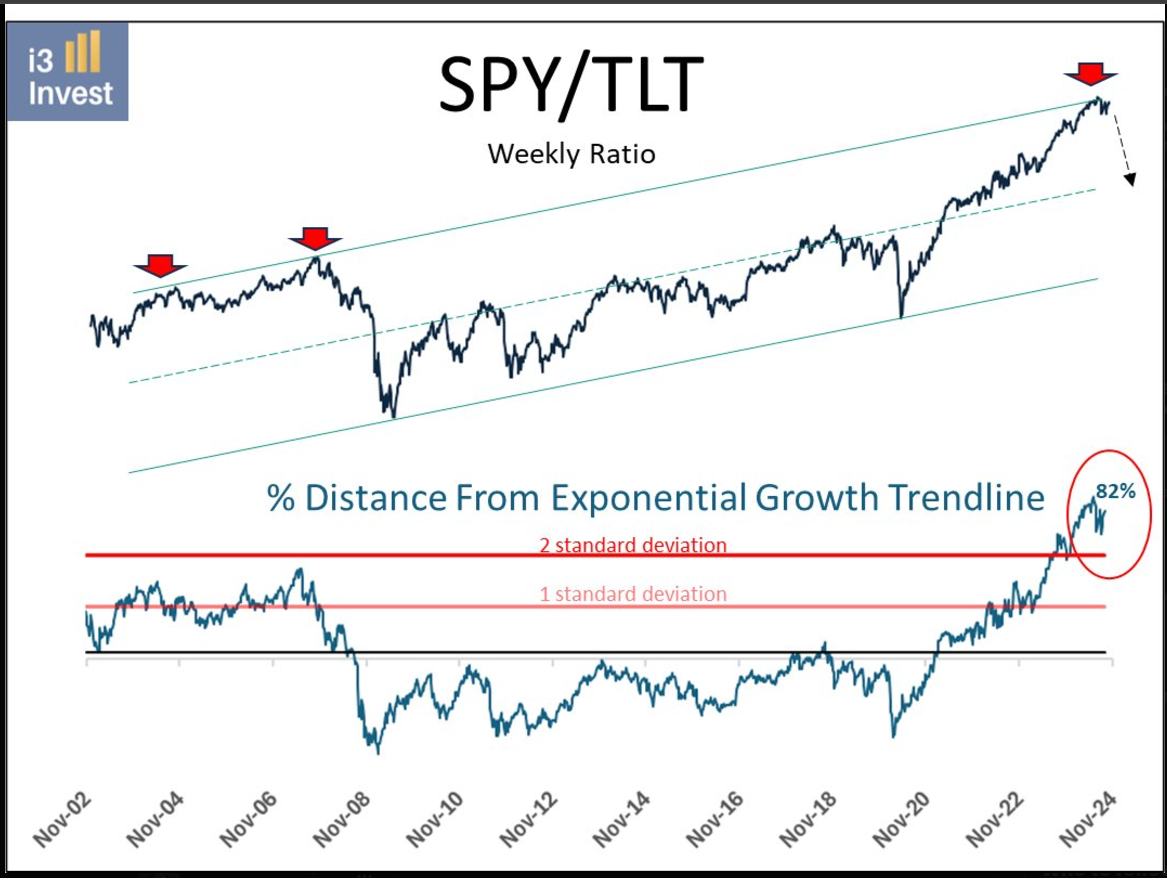

The above table was cut-and-pasted from “X” last week, (can’t recall the author) and while I do think “relative’ trends like this can be deceptive, this chart does make a good case for being long the TLT and short the SPY (or at least reducing exposure to the SPY).

If the tariffs do appear shortly after the inauguration, and they remain and they appear punitive, it could be inflationary and that would mean a steeper yield curve, higher long-term Treasury interest rates, and another tough year for bond returns. Personally, I am hoping the President-elect is judicious and thoughtful about tariffs and trade restrictions, and we don’t suffer a repeat of Smoot-Hawley (highly, highly unlikely, mainly because the US economy is so very different today than the US economy of the late 1920’s and early 1930’s).

Here’s a series of CEO comments from earnings release conference calls, that was published by “The Transcript” in the last few weeks.

International

Tariffs are on CEOs’ minds

“I’ll start it off by saying a statement of the obvious, and that is it’s very early. And like everyone, we’re waiting to see what happens when the Trump administration actually takes office in January. Having said that, we feel good about the processes and the systems we put in place since the first Trump administration to manage tariffs or other challenges.” – Lowe’s Companies ($LOW ) EVP Marvin R. Ellison

“So the last time we were faced with tariffs. We had just over $100 million exposure in terms of Chinese imports into the United States. And out of that, about $100 million was subject to tariff. At that time, we were pretty successful in mitigating most of the exposure with pricing. This time around what’s changed is that we’ll have to see what we can do with pricing. It depends on what product categories they have go after it depends on the magnitude of what they’re doing…But what’s changed probably more so is that our exposure is a little bit less, it’s less than $100 million right now, and we have more manufacturing capabilities.” – Mettler Toledo International ($MTD ) CFO Shawn P. Vadala

Companies will seek to reduce dependence on China

“And then the third thing is what I would call the more permanent structural change, which is how do we continue to drive our strategy around our supply chain to lessen our dependence on China, which we’ve done a lot of that, 8 years ago, 10 years ago, about 40% of what we sold in the U.S. came from China. Today, that number is closer to 20% to 25%…we will continue to be less dependent on China from a supply chain point of view. So that’s all I’d like to say about tariffs.” – Stanley Black & Decker ($SWK ) President, CEO & Director Donald Allan

Tariffs may create inflation

“The question, I think, would be more to the extent that tariffs can have a negative impact or negative read-through on inflation that might have a chilling effect into how quickly the Fed continues to lower interest rates, and that would be more detrimental to biotech. So again, not a policy, but more of a kind of macroeconomic.” – Charles River Laboratories International ($CRL ) Corporate EVP Flavia H. Pease

“I went through the tariff regime at Stanley Black & Decker back in the first President Trump Administration. We were not proactive in pricing. The learning from that is we are going to be proactive in pricing going forward. And so as you hear more about this over time, I want you to realize that this is going to be something that is on our radar and is very important that we address early on in whatever changes if things change.” – Stanley Black & Decker ($SWK ) President, CEO & Director Donald Allan

This may help to reduce some of the uncertainty around the trade environment, as we approach the Inauguration.

None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal even for short periods of time. The information above may or may not be updated, and if updated, may not be done in a timely fashion.

Thanks for reading.