Crude oil was down 4% Sunday night, as OPEC once again announced a production increase of 411,000 bpd (barrels per day), a move by OPEC that will eventually help US inflation, and give the Fed another reason to lower the fed funds rate.

In early April, when the whole tariff mess blew up, Treasury Secretary Bessent came out publicly, and noted there was a bigger picture aspect to the tariff picture, which included not just raising $700 – $800 billion from the new tariffs, but the current Administration wanted to bring the price of crude oil down, which would lower interest rates and hopefully encourage the Fed to lower the fed funds rate, all intended to lower the refinancing costs on US Treasury debt and thus ultimately start to bring the budget deficit down in a meaningful way.

The US mainstream media only wanted to focus on the tariff issue, since it generated the more emotional response from Americans, but with the tax bill now in the works, the less emotional and really analytical background to the tariff policies are starting to come to fruition.

Does it mean it will be a success ? That’s very hard to say, since the tax bill is only slowly makes it way through Congress, but the lower crude oil prices, which eventually means lower gas prices, sure helps.

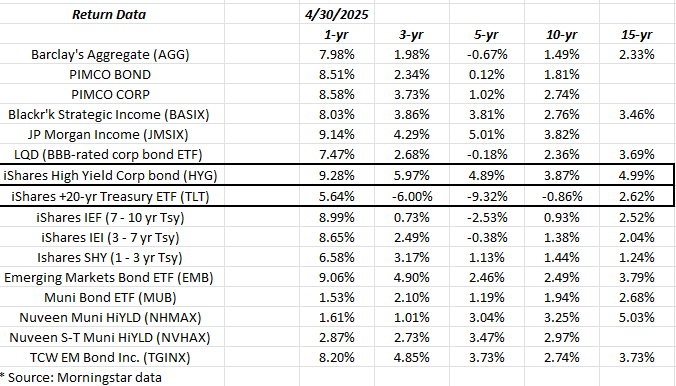

The two asset classes highlighted on the above spreadsheet are TLT and the HYG or iShares High-yield Credit ETF.

Note how the 10-year and 15-year returns for most bond asset classes remain quite low, after the zero interest rates from 2008 to 2016, and then again from March, 2020 to March ’22.

The 10-year annual return on the TLT is still negative, and has been for a year or so.

Short-end interest rates will eventual fall as the Street figures out when the FOMC will lower rates, before the FOMC does.

The Wednesday FOMC release will not move the fed funds off the current 4.375% fed funds target, but I do expect Jay Powell to be a little more conciliatory in his comments, now that the President has tempered his comments about the future of the Fed Chair. Plus, falling crude prices and the benign inflation data for the first three months of the year, should help temper Fed hawkishness.

That being said, the real “disconnect” being seen every day now is the difference between rising “inflationary expectations” and the lack of a response in the actual Treasury market. Those rising inflation expectations should have caused the 10-year and out Treasury yields to rise and prices to fall.

Last week’s March ’25 PCE data was again friendly, and the almost all of the January, February, March ’25 inflation metrics – mainly Core CPI and Core PCE – have been very “bond-friendly”.

The one aspect to the lower tax bill – a reduction in the corporate tax rate from 21% to 15% – seems the least deficit-friendly of all the proposals, but the President and the Congressional majority may opt for greater reductions in personal marginal tax rates, and sacrifice any meaningful reduction in the corporate tax rate. (That’s a personal opinion.)

Summary / conclusion: Fixed income asset class returns have been a tough long since 2021 and really since 2022. However, eventually I do think the fed funds rate can be cut to 2.75% – 3%, since meaningful budget deficit reduction, is on it’s face, contractionary for the US economy, and with that lower fed funds rate, we could see nice rallies in longer-maturity Treasuries as this unfolds.

Like 2021 – 2022 though, this may be another last hurrah for meaningful bond rallies until there is good reason for yield to rise sharply higher again.

Credit spreads have gradually improved since the lows on April 7th – April 8th, along with the improvement in the equity market.

Moody’s has set an expected default rate of +2.8% to +3.4% for high yield bonds for 2025, which given publicly-traded high yield credit like the HYG is trading at a 7% – 8% yield, which implies a lot of yield cushion, but all of the major credit rating firms have raised their default risk levels for 2025, given current conditions. The average default risk for US firms rose to 7.8% during Covid or 2020. (As a former credit analyst in the early 1990’s, it’s been 30 years since Moody’s and Standard & Poors and Fitch credit reports were read regularly. A recent Moody’s report found on Google seems to make a distinction between “expected default rates” of US bonds, and “rising default risk”. I do know after Enron and Worldcom went bankrupt in the early 2000’s the rating agencies had to revamp their credit rating methodology to incorporate “market-based” indicators like actual changes in credit spreads, versus the old black-box model of debt service coverage and cash-flow ratio’s, which as we found out with Worldcom and Enron, were pure fiction, when credit spreads were blinking red well before the actual defaults.)

Equity futures are down about -0.50% to -0.75% Sunday night, after last week’s 1.5% rise in the SP 500, and now on Monday morning the averages are looking to open at around those same levels.

The SP 500 is fast approaching it’s 200-day moving average just over head on the chart.

None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal even for short periods of time. None of the above information may be updated, and if updated, may not be done so in a timely fashion.

Thanks for reading.