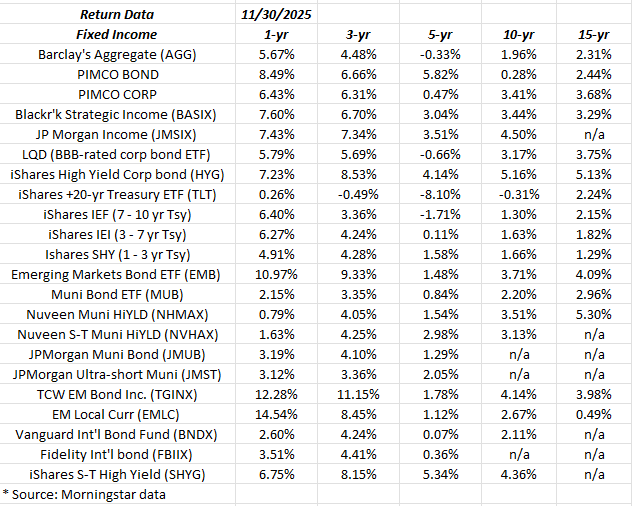

Here’s a quick look at annual returns across the fixed-income classes as of 11/30/25, with emerging markets income leading the way, and municipal bond returns lagging.

It was never a big position at all within fixed-income in 2024, but all of client’s muni bond funds were sold the day after President Trump was elected and the House and Senate went red. Muni’s typically follow the election cycle, particularly the to-and-fro around the tax debate, and higher household taxes from higher ordinary income tax rates typically lead to a better demand for muni’s (usually when the Democrats run Washington), while muni demand and returns tends to be lackluster when the Republicans are in control.

My plan – for now – is to keep an eye on muni’s vis-a-vis the November ’26 election cycle and make adjustments or changes at that point.

As of today, client municipal bond positions are very small.

International equity this year did well as did emerging market, and part of that could be the respective bond market returns, particularly for EM. It was a year of double-digit total returns for EM bond markets, as the EM’s followed the Fed’s easing cycle.

Corporate high yield is doing the best within the US asset classes. This blog is upgrading to the LQD and more investment-grade debt as the credit cycle and credit spreads remain unusually tight, and since it’s more likely that total return will be driven more by duration than (credit) yield.

The TLT (8th row down from the top) has a negative 8% 5-year return for the ETF. My own opinion is there is more upside to the long end in ’26, particularly if SP 500 equity returns start to stall in 2026.

Summary / conclusion: Frankly, it’s been a surprisingly good year for fixed-income returns. Investors are still nervous over the Fed Chair announcement. It’s a tough spot to be in for the new Chair: either he will be perceived as a Presidential lackey, or he’ll be doing battle with the President and the President’s appointees on a frequent basis. Either way, it may be a no-win position.

My own opinion on inflation is that the only reason we saw a 2% inflation rate from 2010 through 2019 was a function of the 2008 Financial Crisis, which was as close to a Boomer Great Depression as there was since WW II. America’s most coveted asset with the most wealth-creation ability for the average American (i.e. the US single-family home) saw it’s first national recession / depression since the 1930’s.

A 2.8% – 3% core CPI, core CPE rate, isn’t too bad given the GDP growth figures for 2025.

A 2.5% core inflation rate is likely far more achievable than a 2% rate.

That’s just an opinion though.

In 2026, it’s likely the fed funds rate slips into the “low 3%” range. The big question is how does the yield curve behave: does the curve steepen or flatten ? This blog is more prone to add duration in late 2025 with higher-quality corporate bond funds or ETF’s like the LQD.

None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future results.

Thanks for reading.

HI- Can you separate income from capital appreciation/decline in muni category? A little misleading as income on tax adjusted basis will boost yield. The only other way to portray value is as a % of a taxable benchmark (with historical timeline)

Would also suggest you include preferreds as an asset category (80% dividend exclusion for non-reit issues).

Happy Holidays!

If i come across the data Phil, I will, but dont have time to look into it right now.