Both the “upside surprise” factor for Q2 ’25 SP 500 earnings and revenue estimates are very strong.

As of this morning’s data from LSEG, the SP 500 EPS “upside surprise” is +6.8%, led by the energy and financial sectors. The SP 500 revenue upside surprise is +2.3%, which is also very healthy, and that’s led by energy and technology sectors.

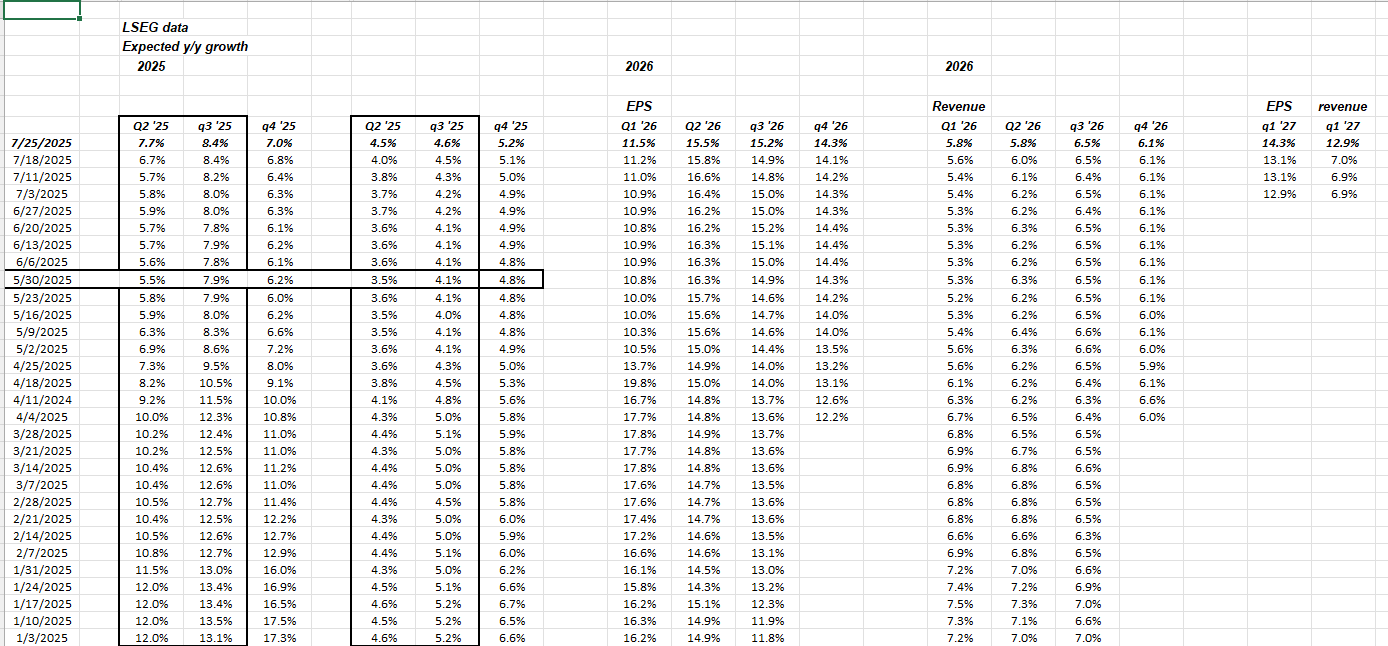

Here’s the spreadsheet that has been published on this blog over the last few months, as tariffs became a daily market issue.

Here’s what’s unusual: the usual and typical negative revisions for the following quarter (in this case, Q3 ’25 EPS and revenue estimates) as Q2 is being reported has actully been reversed, and those Q3 ’25 expected SP 500 EPS and revenue growth rates are now being revised positively.

There is an upward trend in Q3 ’25 SP 500 EPS and revenue estimates, which is very unusual.

This gets back to last week’s SP 500 earnings update, about the revision trends indicating analyst confidence.

That positive revision pattern is telling.

Summary / conclusion:

Much more will be written over the weekend as many companies that have been written about on this blog, report their Q2 ’25 financial results next week. While Microsoft and META report on July 30, Apple and Amazon also report July 31, the most interesting report in my opinion will be Boeing.

It’s very fortunate for Kelly Ortberg that he came aboard just before a significant Administration change in Washington, D.C., which has propelled the defense sector and Boeing (BA) common stocks in 2025.

BA is up 30.66% YTD as of Thursday night’s, July 24th close. It’s still well shy of it’s $449 all-time-high in March, 2019.

More to come this weekend. None of this is to be considered advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. None of the above may be updated, and if updated, may not be done in a timely fashion.

Thanks for reading.