Apologies for the delay in getting thoughts on Netflix’s (NFLX) calendar Q2 ’25 published for readers.

The streaming giant, which continues to maintain a huge lead on it’s competitors, (although YouTube continues to get inserted into the discussion more and more) reported a good quarter, with EPS and revenue beating estimates by +2% and fractionally, resepctively, while operating income came in 3% ahead of the consensus.

Netflix also raised guidance for calendar 2025, which made Netflix a “triple-play” company i.e. beating on EPS and revenue consensus, and then raising guidance for the calendar year.

One of the issues around the stock coming into earnings was the lack of any negativity around the stock and the company, much like an Nvidia (NVDA) the last few years. I didn’t hear or read one negative comment on NFLX coming into the 2nd quarter earnings release other than valuation (see this blog’s NFLX earnings preview here), which is usually a regular criticism in bull markets.

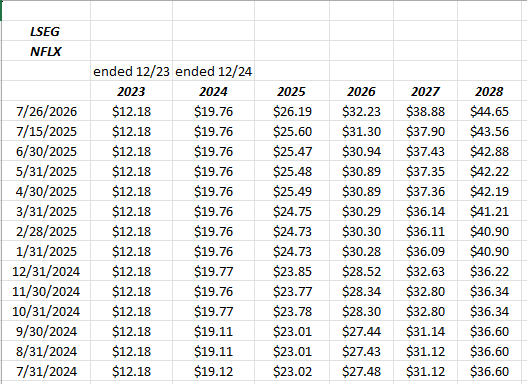

EPS revenue estimate revisions post-earnings:

Both the EPS and revenue estimate revisions continue to get revised higher post the Q2 ’25 earnings release, which should quell any worries about fundamentals being under pressure after the financial results were posted.

Shorts have started to circle Netflix like sharks in blood-stained water, but I do believe it’s still a little early for a hedge-fund to make substantial bank shorting Netflix at least on an erosion of business fundamentals. The business model “flywheel” is still emerging, and Netflix’s model is still evolving.

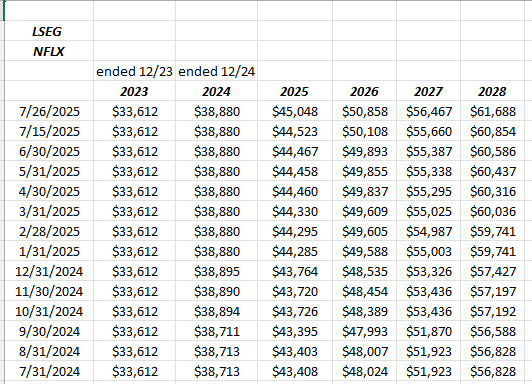

Free-cash-flow worries:

![]()

This blog not only tracks EPS and revenue estimate revisions but also free-cash-flow estimate revisions, and as readers can see, the revisions post the July 17th earnings release for forward free-cash-flow estimates continue to track higher (i.e. positive revisions to forward free-cash-flow estimates).

In terms of margin worries, NFLX management addressed the heavily-tilted back-half of 2024 releases which have skewed NFLX’s operating margin, and management noted that while the operating margin guidance for NFLX was raised once again after the July 17th earnings release, the full-year operating margin will be higher than what was seen as of the Q2 ’25 number.

Summary / conclusion: With many blog posts left to do before next week’s earnings releases and economic data are seen, this blog tries to follow-up on every earnings preview with a post-earnings review just to close the loop.

Personally, NFLX’s quarter was fine, and I think the long-term story remains intact. However, if the equity market does see it’s typical August – September weakness, NFLX will decline in price, and given it’s valuation, it will likely drop more than the SP 500’s decline.

However two comments – one from an analyst and one from Ted Sarandos, NFLX’s CEO – gave me comfort for the next 6 – 12 months (and even further out if you want to push it):

Ted Sarandos: On the conference call Sarandos noted that the 2025 slate of shows like “Squid3” as well as “Wednesday” and “Stranger Things” is “more back-half weighted than in previous years”, which includes two more football games on Christmas Day. Sarandos noted that the 50% of TV programming that isn’t streaming will continue to gravitate to streaming. NFLX’s live component, which includes (sport is a subcomponent of the live strategy) remains a small part of NFLX (presumably revenue) right now.

Analyst comment: Although the actual report can’t be found, one analyst noted that despite’s it’s US and overseas growth, NFLX still accounts for less than 10% of all global TV time (ex-China), which puts the size of the market in perspective.

This blog has been selling or trimming small amounts of shares to manage the weight in client accounts, the secular growth story remains intact. Shorts are worried about the cost of the content buildout around “live” (including sports), and compressed margins around the buildout, but Netflix Ad Suites is now complete and is being rolled out, with advertising expected to be “margin-rich” for the streaming giant.

That’s the case, and it still looks good. Common stock’s with NFLX’s valuation though can correct sharply and the drawdown can last a while if the market runs into “PE compressing” events, but that’s always the case for growth stocks.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Readers and clients should gauge their own comfort with individual stock, ETF or mutual fund volatility and adjust accordingly. None of the above information may be updated and if updated, may not be done in a timely fashion.

Thanks for reading.