Alphabet (GOOGL) reports their Q2 ’25 financial results after the closing bell on Wednesday night, July 23rd, 2025, with analyst consensus expecting $2.18 in earnings per share, on $93.9 – $94 billion in revenue, and $31.1 billion in revenue for expected y-o-y growth of 15%, 11% and 13% respectively for the search giant.

The ironic aspect to this quarter is that it will be the worst quarter since Sept ’23, when the search giant saw 9% y-o-y EPS growth, 11% revenue growth but 25% operating income growth.

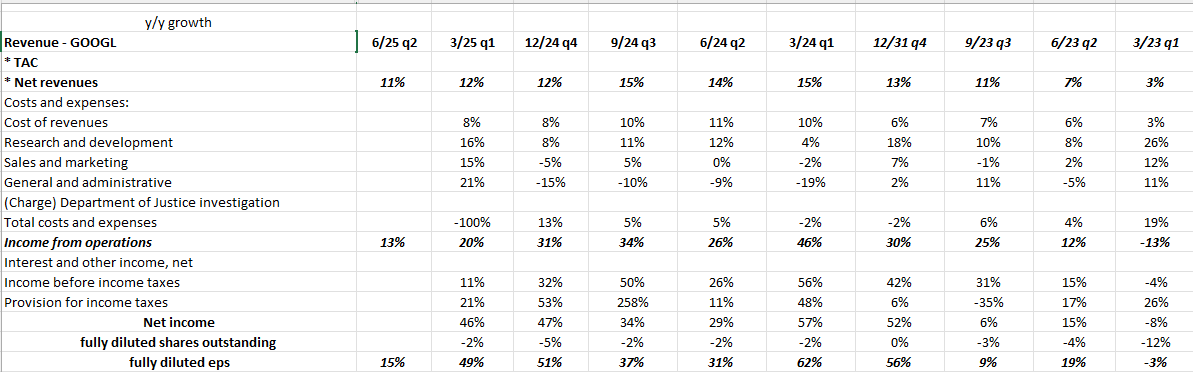

Here’s common size income statement of this period:

Source: internal spreadsheet

GOOGL has been notably weak the last 6 months when the original DeepSeek headlines hit, resulting in sharp selling for any stock related to Nvidia and the AI buildout. Alphabet’s Wiz acquisition was dilutive at a time the stock was down already thanks to Liberation Day, and then on April 17th, a Federal Court Judge announced that “Google holds an illegal monopoly on online advertising technology”. There was also the Apple trial disclosure in early May ’25, that was interpreted as Alphabet’s search function might be curtailed on Apple’s iPhone. Apparently during the trial it was disclosed that Google’s search traffic on Apple devices had declined for the first time in over two decades, thanks to greater usage of ChatGPT and Perplexity.

Not a fun quarter for our friends at Alphabet. But this also represents opportunity.

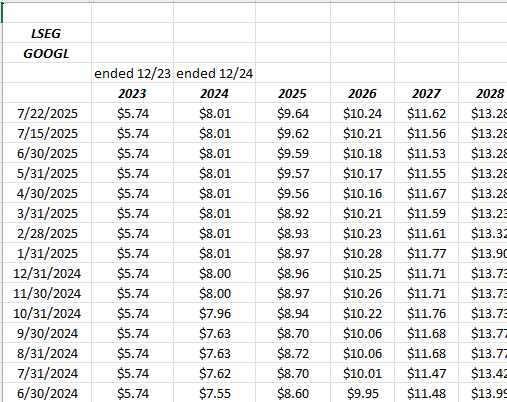

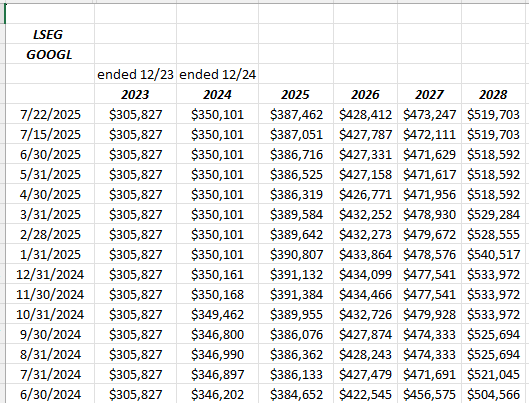

EPS and revenue estimate revisions:

Readers rarely comment on the estimate revisions but note how the barrage of negative headlines for Alphabet hasn’t resulted much in EPS revisions for calendar 2025. GOOGL’s 2025 EPS estimate has risen 12% since June 30 ’24.

GOOGL’s revenue revisions also remain positive despite the prospects for expected loss in search market share.

Advertising is still 74% of total GOOGL revenue as of the March ’25 quarter, but the fact is that metric has been slowly declining from the low 80% range in 2022. Google Cloud has been growing 1% – 2% per year, and was 14% of Google’s total revenue as of March ’25, up from 7% in late 2021.

The positive aspects for Alphabet today are Waymo and YouTube. Depending on your search vehicle, Waymo’s current estimated valuation is $45 – $50 billion, up from just $5.6 billion last October ’24, while YouTube’s estimated valuation is thought to be $475 – $550 billion. My own opinion is that Waymo’s valuation could grow quite rapidly over the next year to 18 months, as it could for Tesla.

Valuation:

Google’s stock is up $35 from it’s last April ’25 earnings report, and has risen 14% in the last month and 5% in the last week.

Google’s EPS the next three years is expected to grow 12% -13% while the current multiple is 18x (3-year average) so the stock is another good example of a reasonably-valued, stock attractive on a PE-to-growth basis. Cash-flow multiples (ex cash) are 16x and 30x with a 5x price-to-sales metric.

The cash-flow is what still amazes me: even with TTM capex (trailing-twelve-month capex) doubling from $30 bl to $60 bl in the last 7 quarters, GOOGL still sports a 4% free-cash-flow yield. GOOGL buybacks average about $15 bl per quarter.

I don’t think raising the buyback amount again will do much for the stock.

No one is yet talking about anyone in the AI segment slowing their capex buildout, but that could be a major catalyst for the company’s stocks throughout the tech AI segment if and when it should happen.

Capex is consuming 46% of GOOGL’s cash-flow as of the March ’25 quarter.

My own model has GOOGL fairly valued right about where it’s trading today at $185 – $190. (The price from the model is $192.) Morningstar has GOOGL fairly valued at $237.

Summary / conclusion:

Three of the former Mag-7 / Mag-10 coming into the Q2 ’25 earnings season are quite beaten up from a sentiment perspective: Google is one, Apple is another, and then you have Tesla, which also reports Wednesday night, July 23rd, after the closing bell.

While Alphabet is facing challenges thanks to AI, particularly around search, the ability which many of these AI giants, particularly the software companies have to change direction rapidly means they are never out of the “game” so to speak in terms of relative performance, but investors have to be patient.

It will be interesting to see how and when and if Alphabet starts to disclose Waymo and YouTube data and to what degree.

Given the headlines the last 60 days and the sentiment coming into the report, there’s likely more upside in GOOGL in the 2nd half of 2025.

With search slowing or at least becoming less dominant, and Waymo and YouTube rising, Alphabet’s experiencing it’s very own version of Schumpeter’s, “Creative Destruction”.

The stock’s a 1% position in client accounts currently.

None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future results.