It’s well-documented that international equity (and even bonds for that matter) have had a good 2025 so far this year, but the following chart on Emerging Market ex-China also indicates that emerging markets are possibly starting to show some forward progress.

Source: Topdown Charts (on X)

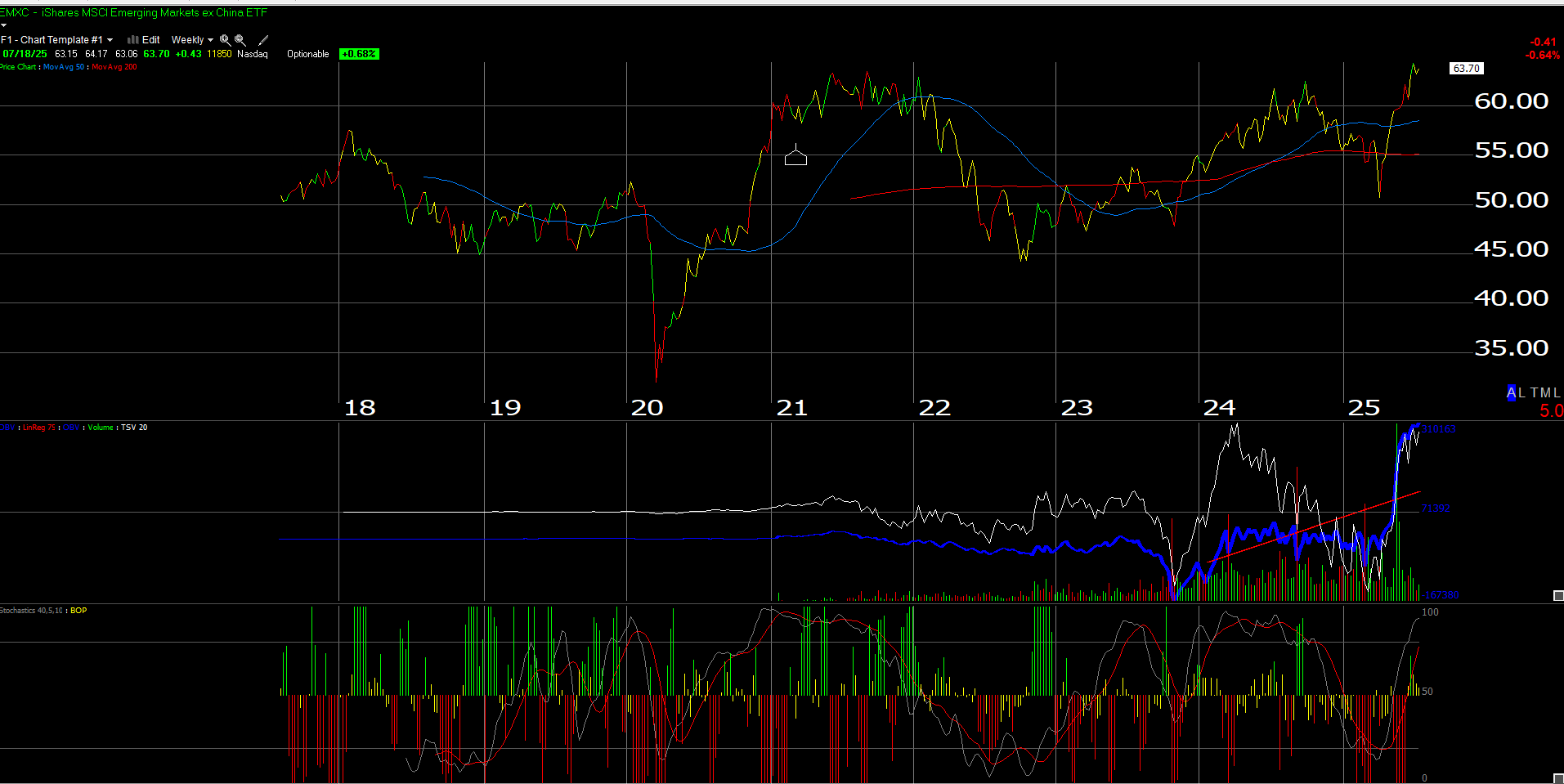

While the Topdown chart above looks to be on a log scale, the iShares EMXC ETF was only launched in August, 2017, hence it’s a much shorter time frame. Here’s the EMXC chart as of Friday, July 18th’s, 2025, market close:

Source; Worden (please click on the chart for easier reading)

The EMXC peaked at $63.74 on June 10th, 2021, and has just now gotten back to retest this level and closed Friday, July 18th, 2025 at $63.70.

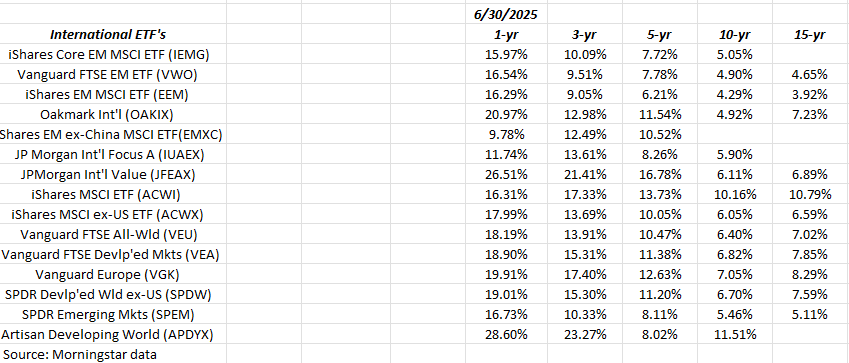

Annual return data for international and EM funds and ETFs:

The above spreadsheet is annual return data from Morningstar and readers can see how the bigger mutual funds like JPMorgan Int’l Developed Value (JFEAX) and Oakmark International (OAKIX) managed by David Herro are up 20% – 25% as of June 30 ’25. The top 3 lines are the emerging markets ETF’s, which are up mid-teens YTD, some of that due to China.

After what China did to Jack Ma and Ant Financial in 2020, it’s difficult to own any China stock market exposure directly. Basically Xi Jing Ping made a personal decision to shelve the Ant Financial IPO late in 2020, after a speculative frenzy around the company. Maybe even more interesting is that with the Alibaba IPO, Jack Ma was the richest person in China and since Jack Ma also founded Ant Financial, the Ant Financial IPO would have meant an enormous amount of wealth for Ma, and that fact saw Ma drawing increasing regulatory scrutiny from Chinese regulators.

Ma has put himself in self-imposed seclusion, away from the public view in China, all because he was a driving force for capitalism becoming more visible in China, and CCP leaders did not like that.

China’s exchanges could get a healthy bounce over the next few years, but it’s tough to own anything China-related for clients.

Summary / conclusion: The last time international equity and emerging markets had a multi-year run with well above-average returns was back in 2000 to 2007. Almost like clockwork, when large-cap growth and tech peaked in March, 2000, international, emerging markets, value-style investing, commodity companies, gold and just about any asset class that went nowhere in the 1990’s, took off like a bottle rocket.

Part of the driver behind international and emerging market returns was China’s economy, which grew at 15% annual rate in the 2000’s as the US economy and stock market took a significant beating. The 2008 Financial Crisis ended both the international and emerging market run, and most non-US asset classes have been tough to find anything other than average returns for 15 years.

Looking at the annual return spreadsheet, note the 5, 10 and 15 year annual returns for the category, which are still mostly single digits.

In my opinion, international and EM are still under-appreciated and under-invested asset classes.

Certainly the weaker dollar is helping in 2025. President Trump’s comments late last week might cause a strengthening in the dollar in the near term, but after the 10% drop in the US dollar in just 2025, some strengthening was expected.

Both David Kelly, JPMorgan’s Chief Global Strategist and Rick Rieder, Blackrock’s Chief Strategist, noted earlier this year that the dollar was fundamentally overvalued and had been for a few years. What was interesting was that they said roughly the same thing around the same time, about the dollar, and from that I thought the dollar’s decline might last longer than 6 months.

The equity bull market of the 1990’s was a narrow market lead by the likes of Microsoft (MSFT), Cisco (CSCO), Intel INTC), General Electric (GE), Walmart (WMT), Pfizer (PFE), etc. Today’s bull market is also narrow with the “Mag 7” or “Mag 10” group of companies.

There is a lot of “non-correlated” asset classes and individual stocks out there waiting for a catalyst. Look elsewhere, other than the Mag-7 and Mag-10 for opportunities in terms of portfolio construction.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Readers and investors should gauge their own comfort with portfolio volatility, and adjust accordingly. None of the above information may be updated, and if updated may not be done so in a timely fashion.

Thanks for reading.