IBM (IBM) is scheduled to report their Q2 ’25 financial results after the closing bell on Wednesday, July 23rd, 2025.

Analyst consensus is expecting earnings per share of $2.64 on $16.59 billion in revenue and $3.19 bl in operating income for expected y-o-y growth of 9%, 5% and 11% respectively.

Despite the YTD return of IBM this year i.e. +31% as of Monday, July 21, ’25, earnings estimates for the full-year or the next few years haven’t changed much.

Last quarter Q1 ’25, IBM put up 1% revenue growth, +23% operating income growth on -5% EPS growth. Both software and RedHat decelerated y-o-y, (overall software growth falling to mid-single-digit growth) while AI rose sequentially, but remains a smaller number. The stock fell 7% in April ’25, the day after reporting Q1 ’25 financial results, as IBM’s “consulting book” has a chunk of the federal business, which was thought to be exposed (at that time) to the DOGE cost-cutting initiative.

IBM guided to 5% constant currency revenue growth for calendar ’25, and is a weak dollar beneficiary.

If IBM hits the +5% consensus revenue estimate for Q2 ’25, it will be the first time the stock has seen +5% revenue growth in any quarter since September ’23.

Valuation story:

The big change in IBM the last few years has been a return free-cash-flow generation. At one point in 6 – 7 years ago, I thought IBM was going to run into significant issues given that TTM (trailing twelve month) free-cash flow had fallen to 70% of TTM net income, but IBM’s quality of earnings have improved markedly, and free-cash-flow is back.

Here’s how this blog evaluates earnings quality for any non-financial company:

![]()

Click on and expand the above spreadsheet for IBM’s earnings quality test.

IBM’s earnings quality has improved nicely since 2022.

Looking at forward earnings estimates, IBM at $285 per share is trading at 26x and 22x expected ’25 and ’26 EPS but only expecting 6% – 7% EPS growth respectively.

While the stock’s PE looks elevated relative to it’s growth rate, IBM TTM cash-flow-per-share and free-cash-flow per share are $15 and $14 respectively, which means the stock is trading today at 15x and 16x those cash-flow metrics, so evaluating the stock on a cash-flow and FCF basis, IBM’s multiple is more attractive given it’s expected growth rates.

Today, the free-cash-flow yield is 6%.

Over the next three years – from ’25 to ’28 – IBM consensus estimates are looking for an average 6% EPS growth on 4% – 5% revenue growth, so you could make the case the stock’s run from it’s previous all-time-high in April ’13 of $215 to today’s $282 – $285, hasn’t been accompanied by much of a change in earnings and revenue growth.

Free-cash-flow has improved for sure, but IBM has not repurchased any IBM stock in the 24 quarters (6 years).

It’s doesn’t sound like Arvind Krishna and the Board are too keen on repurchasing shares at any point in the near future, either. (That may not be a bad thing either. IBM wasted a lot of cash in the Ginny Rometty era buying back stock without a discernable growthy path forward, although I do think Ginny was put in a tough spot when Sam Palmisano left, which was when the growth started to contract.)

Summary / conclusion: The way IBM is trading it appears that sell-side consensus is expecting better AI growth out of IBM, (or maybe even looking down the road further than that to quantum computing), but you could make a case that the stock is extended in the high $200’s here.

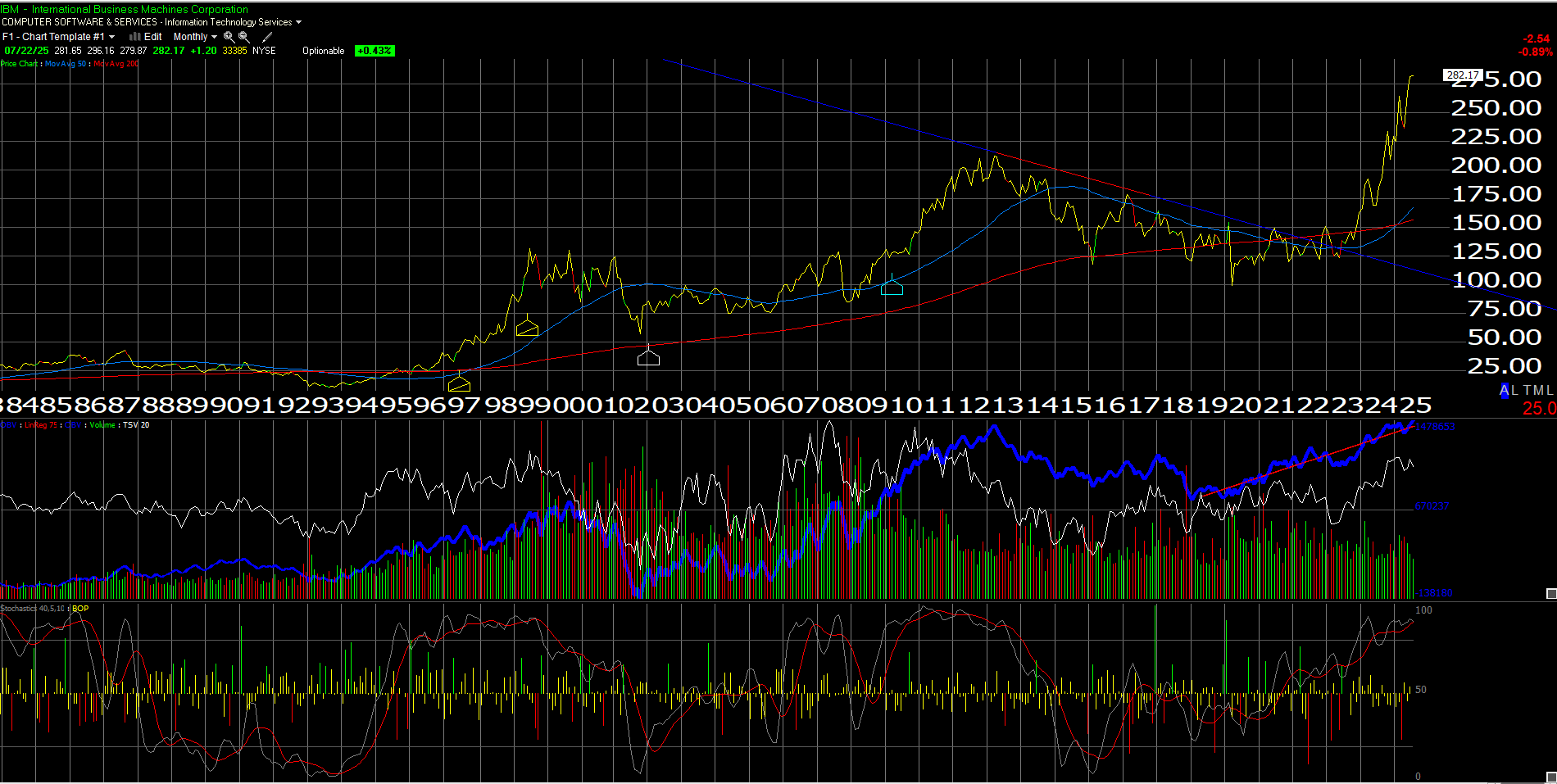

However the breakout in IBM’s stock in late September ’24, after being under water for 11 years isn’t to be ignored.

I think it was the great technician Louise Yamada who once said, “the greater the base, the bigger the race higher” which is a reference to the amount of time a stock spends consolidating under all-time-highs, and the power of that time and consolidation, and what it might say about forward returns.

Just looking at the numbers, the analysts aren’t that excited yet about IBM, in terms of walking up estimates. This article from SeekingAlpha talks about IBM’s expanding AI book of nearly $6 billion, which was surprising to me that the AI run rate was that high.

The technical breakout on the stock is important: IBM is now a top-ten holding in client accounts, after years of not holding it at all. In Q4 ’24, the stock was quickly bought in bigger quantities when IBM traded above the $213 – $213 previous all-time-high from 2013, and represents an approximate 3% position in client accounts, currently.

Stocks like IBM that were dormant or dramatically underperformed the secular bull market in US stocks from 2013 forward, could hold their value better in a bear market given that dramatically underperforming stocks don’t wear the “crowded trade” crown.

Here’s previous articles on IBM: here, here, here and here.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. None of the above information may be updated, and if updated, may not be done so in a timely fashion. Readers and investors should gauge their own comfort level with portfolio volatility and adjust accordingly.

Thanks for reading.