IBM is scheduled to report their Q3 ’24 financial results after the closing bell on Wednesday, October 23rd, 2024.

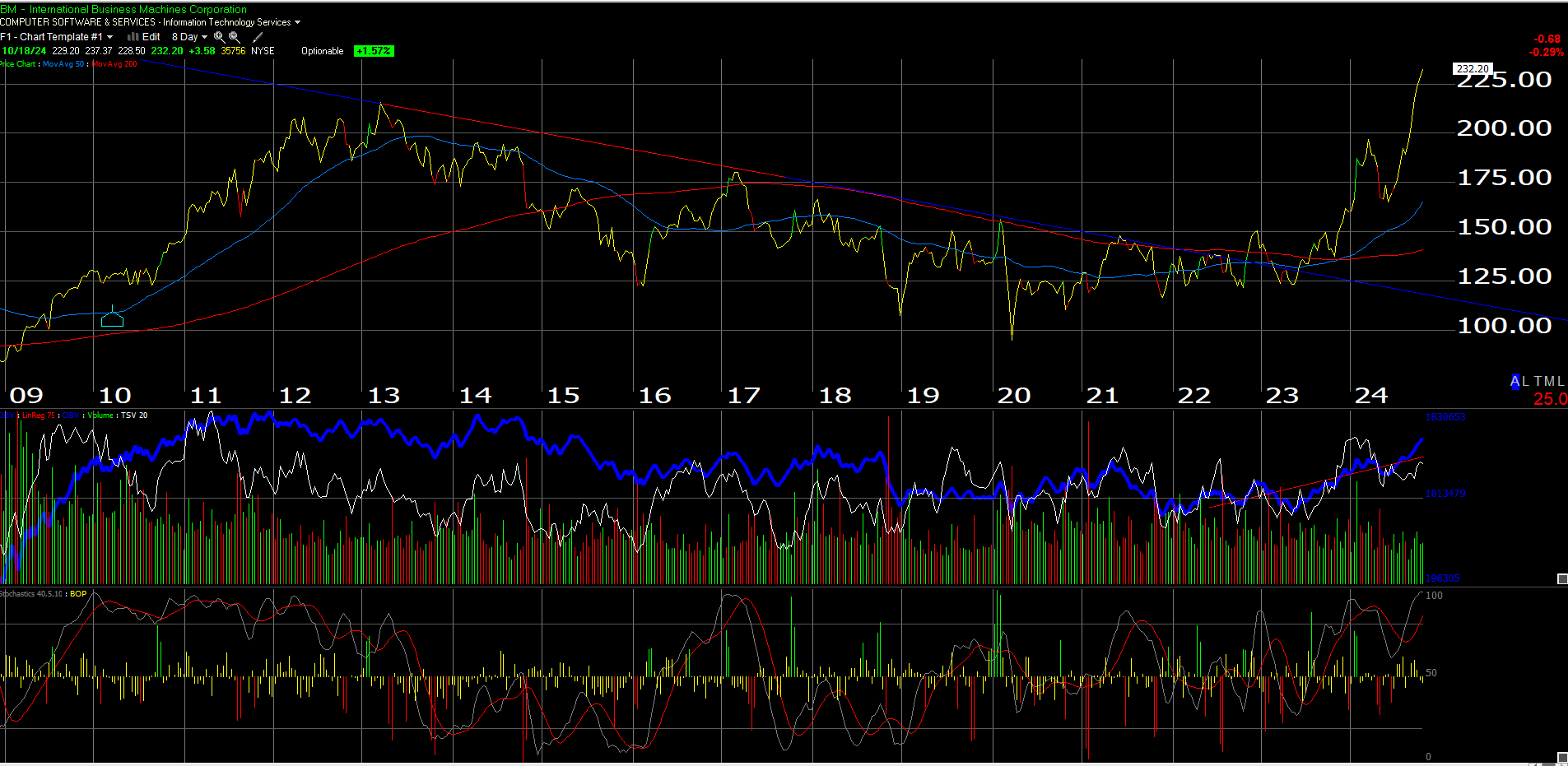

September, ’24 saw the stock see a strong breakout above the April ’13 highs of $213 – $215, as evidenced by this Worden chart:

This is an actually an 8-day chart of IBM, which allows the left-hand margin to go all the way back to 2013, so readers can see the old all-time-high.

That’s also a breakout of an 11-year base, (if you want to call it that), although IBM’s stock has a long history of performing like this, i.e. long periods of a range-bound stock price, followed by a big breakout, which dates back to the 1980’s.

IBM fundamentals and valuation:

- When IBM reports their 3rd quarter Wednesday night after the closing bell, consensus expectations will be looking for $2.23 in EPS, on $2.6 billion in operating income, and $15 billion in revenue for “expected” y-o-y growth of 1%, 15% and 2% revenue growth.

Looking for a fundamental metric that supports the breakout in the stock and the ramp in the shares in the last 90 days, operating income beat consensus in Q2 ’24 had an “upside surprise” of 48%, with $2.87 billion actual, versus the consensus estimate of $1.94 billion (at that time).

- In the aforementioned Q2 ’24, IBM grew revenue +2%, operating income +16%, and EPS 11%, all y-o-y. The big takeaway from both Morningstar and the conference call notes, were that IBM’s AI is at a $2 billion run rate (since inception, not YTD), and Arvind Krishna noted on the conference call that it’s AI business mix is 1/4 software and 3/4’s consulting signings.

- For Q4 ’24 (typically IBM’s strongest quarter of the year), the sell-side consensus is expecting $3.76 in EPS, $4.3 billion in operating income, and $17.9 billion in revenue for expected y-o-y growth given current estimates of -2% EPS, +16% operating income and 3% revenue growth.

- For full-year 2025, the current consensus is $10.72 and $66.3 billion in revenue for full-year expected growth of 5% and 5%.

Let’s see how the guidance looks for Q4 ’24 and for 2025.

Perhaps something the street is warming up to, is IBM’s improved free-cash-flow. Since the middle of last decade, when IBM was routinely spending $500 million to $1 billion per quarter in capex ($3 – $4 billion per year), capex today has shrunk to a $1 billion per year run rate (as of the trailing-twelve-month numbers) which means IBM’s free-cash flow has improved without a commensurate improvement in cash-flow. (This is somewhat anomalous to what other big tech company’s are seeing i.e. huge y-o-y growth in capex spending on AI, so maybe Arvind and the team, have found a nice little niche within AI that can grow smartly and yet not require the huge capex outlays.)

IBM’s trading at 23x and 22x EPS for expected EPS growth this year and next year of around 5%, but the cash-flow valuation metrics are just half that at 12x and 14x TTM cash-flow and free-cash-flow. A few years ago, I was worried about IBM’s quality of earnings (comparing net income to trailing cash-flow and free-cash-flow), but today, IBM’s cash-flow and free-cash covers net income by 156% and 143% respectively.

No question cash-flow and more importantly free-cash-flow has improved.

IBM hasn’t spent $2 billion on a share repurchase since the March, 2019 quarter and the share repurchases dried up entirely shortly following March, ’19, but IBM could be ready to begin share repurchases again, with their cumulative growth in free-cash-flow the last 2 – 3 years.

Trading at 23x trailing EPS, and about that metric for ’24 and ’25 estimates, as well as 3x trailing price-to-sales, the 5% free-cash-flow yield and 2.75% look “meh” until you look at the cash-flow valuations.

Summary / conclusion:

Technically, and fundamentally, at least from a free-cash-flow story, IBM has become a more interesting story in 2024. The technical breakout should be noted for technically-inclined investors.

Ultimately, for IBM to be a stock that rivals some of the tech growth giants of today in forward expected stock price returns, it will need sustainable revenue growth in the high-single-digits (at least) and an occasional quarter of 10% revenue growth.

It’s not a bad thing that old tech is starting to stir. AI is giving every tech company with a software or consulting arm an opportunity to reinvent themselves.

Let’s see if IBM resumes share repurchases, but ultimately, a healthier IBM means consistent revenue growth and a viable AI strategy.

None of this is a recommendation or advice, but only an opinion. Past performance is no guarantee of futures results. Investing can and does involve the loss of principal, even for short periods of time. All EPS and revenue estimate data are sourced from LSEG.

Thanks for reading.