Schwab (SCHW) will report their calendar Q2 ’25 financial results on Friday morning, July 18th.

Analyst consensus is expecting $1.10 in earnings per share on $5.73 billion in revenue for expected y-o-y growth of 51% and 22%. Pre-tax income is expected at $2.77 billion for expected y-o-y growth of 44%.

Since Schwab peaked at $96 per share in early February ’22, the stock originally fell to the $50 area (and even a little lower than that) in 2023 (twice) but has slowly made it’s way back to within 9-iron distance of it’s former all-time-high in the last two years.

Schwab is up 24% YTD (as of Wednesday night’s 7/16 close).

When SCHW peaked in early ’22 it was trading at 40x earnings, for what was expected to be 20% y-o-y EPS growth, while today SCHW is trading at 20x for an expected EPS growth rate in ’25 of 37% on revenue growth of 15%.

A high-multiple momentum stock is now a reasonably-valued PEG (pe-to-growth) play.

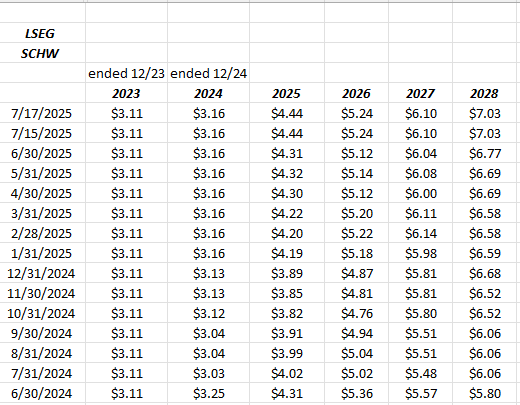

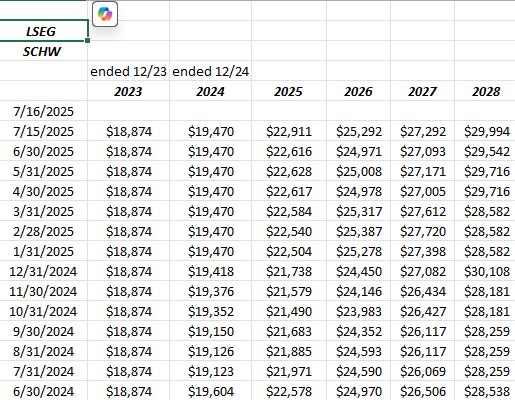

SCHW EPS and revenue estimate revisions:

SCHW’s 2025 EPS estimated bottomed in late ’24 and has been revised steadily higher since that time.

Schwab’s revenue estimate revisions have followed the same pattern.

In Q1 ’25, revenue grew 18%, pre-tax income was up 33%, and EPS rose 41%. Net new assets alone grew $39 billion in March ’25. Jefferies made an interesting point in their post-earnings analysis that TDAmeritrade’s business is slowly returning to Schwab, accounting for 2% – 3% organic growth in Q1 ’25. Jefferies also noted that Schwab currently has roughly 30% wallet share of TDAM’s clients that were onboarded, while that should be closer to 50%.

Summary / conclusion:

With Schwab’s merger / acquisition of TDAmeritrade now behind it, Schwab’s investment thesis returns to a “fundamental” one. Trading at 20x forward EPS for expected earnings growth in ’25, ’26, and ’27 of 37%, 18% and 16%, on expected revenue growth for the same three years of 15%, 12% and 8%, the valuation story is self-explanatory.

Technically, a break and heavy volume close above $96 – $97, after a three-year consolidation period, would be a very favorable technical sign.

Schwab recently raised the quarterly dividend from $0.25 to $0.27 per share, the first increase in 8 quarters.

As an advisor who has all clients assets with Charles Schwab as a 3rd-party custodian, I was relieved Schwab didn’t chase the crypto or bitcoin craze in the 2020’s, but watching the rise of RobinHood of late, and in particular after Amazon and Walmart announced they were considering converting to stablecoin (US dollar-backed crypto) to reduce the cost of the interchange fees from credit cards, I wondered if this wasn’t the ultimate legitimization of crypto, by America’s two largest retailers, and if Schwab is now behind the “Bitcoin” boat.

As the low-cost leader in the former “discount-broker” realm, Schwab is still an asset-gathering juggernaut. The net new assets that get brought in every quarter is still quite formidable.

With current growth expectations of 37% in EPS and 15% revenue growth in calendar ’25 and the current multiple 20x, the stock is way too cheap here. If a $125 fair value price is used for Schwab, the stock is still just trading at 28x for 37% expected EPS growth this year.

Schwab is this blog’s 2nd largest financial weighting behind JPM and in the top 10 of client holdings. Past articles on Schwab are here, and here.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. None of the information above may be updated, and if updated may not be done so in a timely fashion.

Thanks for reading.