Charles Schwab (SCHW) is scheduled to report their Q4 ’24 earnings on Tuesday morning, January 21, 2025. Analyst expectations for the 3rd party custodial giant are $0.91 in earnings per share on $5.19 billion in net revenue, for expected y-o-y growth of 34% and 16% respectively. Operating or pre-tax income is expected at $2.4 billion for expected y-o-y growth of 50%.

These are the best y-o-y rates of growth for SCHW since the Dec ’22 quarter.

The EPS estimate has improved from $0.84 exiting Q3 ’24 to $0.91 today, so don’t ignore that.

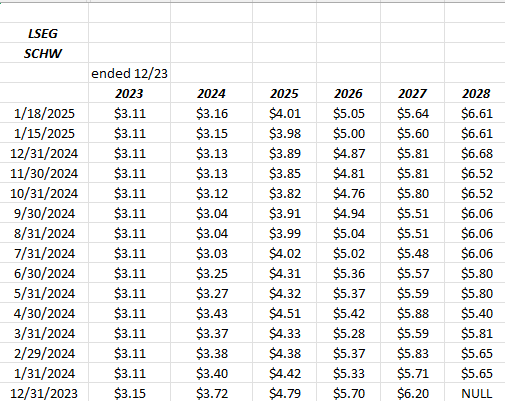

Source: LSEG

Looking at the above EPS estimates for 2024 and 2025, note how EPS estimate revisions were negative, and then bottomed in late July, August ’24, which is about when the investment community and the fed funds futures figured out that the FOMC was going to start reducing the fed funds rate in late September, ’24.

The so-called “cash sorting” issue at Schwab is really just a function of the inverted Treasury yield curve, and it’s crimped financials for 3 years now. With fed funds at 5.375% from the week of July 28 ’23, Schwab was feeling the maximum distortion of the 5.375% money market rate, and – at that time anyway – the 2-year and 5-year Treasury yields of 4.88% and 4.18%, which squeezes the net interest margin, and Schwab felt that to the maximum from July ’23 until late September ’24, when the pressure started to ease (if only a little).

80% of Schwab earnings are net interest income related, so as the net interest margin was squeezed, so was Schwab’s earnings, and margin.

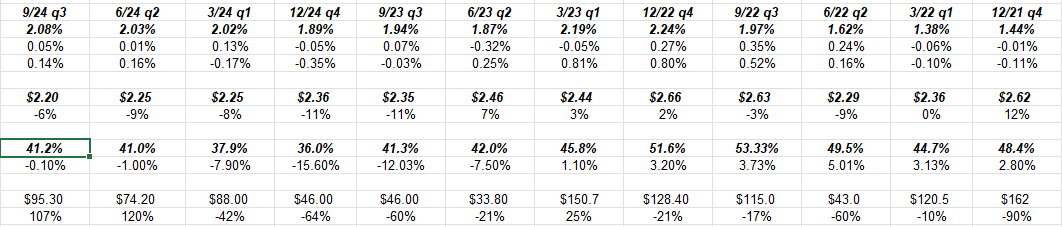

Schwab’s net interest margin should average around 200 bp’s or 2% over time, in a “normal” market environment, which should help generate a pre-tax operating margin in the high 40% – low 50% range. Here’s the progression on Schwab’s pre-tax operating sine just prior to the FOMC raising the fed funds rate through Q3 ’24:

The cursor highlights the latest quarter pre-tax margin.

There is still some upside remaining to be captured in Schwab’s operating margin for investors.

The other side of the growth equation, is Schwab’s “net new” asset growth which in Q3 ’24, was $96 billion and in the Q2 ’24 was $74 billion. Schwab ended Q3 ’24 with $9.9 trillion in AUM, compared to Blackrock’s $11 trillion as of Q4 ’24.

It will be interesting to see how Schwab and Blackrock AUM compare after Schwab releases their Q4 ’24 AUM number.

Schwab’s valuation:

At $76 per share, Schwab is trading at 24x and 19x estimated ’24 and ’25 EPS of $3.16 and $4.01. Expected growth in ’24 just 1%, versus expected EPS growth in ’25 of 25%.

Schwab’s forward estimates reflect +25% growth expected in 2025 and +26% in 2026. Like the earnings preview of JPMorgan and Citigroup posted here last week, it was surprising to read that “expected” growth in the Schwab EPS estimates. Note how Citi traded after earnings last week. (The announcement of the $20 bl share buyback by Citi didn’t hurt. It’s doubtful Schwab would ever get close to that number.)

Schwab forward dividend yield as of Friday’s close was 1.31%, while the dividend has been maintained at $0.25 the last 8 quarters as Schwab rides out this period of squeezed profit margins.

Wait for the dividend to get increased again as one signal of Schwab’s confidence that the interest rate and yield curve environment are becoming less stressful for Schwab’s balance sheet (as I believe both are since September ’24).

Schwab hasn’t made any sizable share repurchases since March of ’23, and that quarter saw $2.8 bl of shares repurchased, with the stock trading (at that time) in the $50 range.

What’s normalized EPS for Schwab and what’s a fair value estimate ? Morningstar in late December ’24 boosted their “fair value” estimate on Schwab to $87, but Morningstar is notoriously conservative, although I think they do a great job with their research process.

In March ’21, SCHW’s total assets were $7 trillion, versus the $10 trillion today in a yield curve and FOMC monetary policy environment that should be more friendly to Schwab. The internal model’s fair value if we assume a 20% ROE, and a net interest margin above 2% and a pre-tax operating margin that can stabilize between 48% – 53%, would be closer to $120 – $125.

If Schwab earned $6 a share in two years, at a 20x multiple that would be $120 per share.

Schwab’s stock peaked at $95 in early, January ’22. The stock’s 3-year annual return is -2.8% versus the SP 500’s total return of 8.94% for the 3-year period from 1/01/22, through 12/31/2024, so SCHW has some catching up to do versus the general equity market.

Summary / conclusion:

Schwab is substantially at the mercy of the yield curve and the monetary policy environment, given the business model. If you are reading this post as a www.seekingalpha.com reader, do a search for my name and Schwab articles and as far back as 2012, I was writing about the 0% interest rate environment and how much it cost Schwab in terms of EPS, having to waive the money market management fees, since Schwab wasn’t paying anything (or very much) other than .01 to .02 basis points in money market yield from late 2008, through the first fed funds rate hikes in late 2016.

Since March of 2022, it’s just the opposite, but the inverted yield curve is not something welcomed or enjoyed by financial system institutions since it distorts savings, and forces savings into the very shortest end of the Treasury yield curve for money market rates. For example, one of Schwab’s higher end money market fund – per this blog’s spreadsheet which tracks that data weekly – was paying 5.25% around the July ’23 peak in fed funds at 5.375%, but has since fallen to 4.18% as the fed funds rate has declined.

The real attraction in early 2025 to owning or adding to Schwab stock is that it is a market laggard, and not the momentum stock it was from 2020 to 2022. The stock price paid dearly after the March ’22 fed funds rate hikes started.

In terms of the financial sector, as much as I like JPMorgan (#1 equity holding as of 12/31/24), it’s tough to add to the market’s leadership names, given their momentum and popularity. Building or adding to positions in market laggards, particularly if the macro environment (in this case that means the yield curve and monetary policy) can be a positive catalyst, is worth the risk, since it likely means less downside in a bear market. That it isn’t always the case, but readers get the point.

While (President) Trump 2.0 could represent it’s own challenges in terms of Fed monetary policy, and a US economic slowdown, Schwab’s net new asset growth, and pre-tax operating margin upside, have had this blog adding to shares since the low in the $50’s and $60’s.

Like a number of Top 10 holdings (see link above), Schwab has been a Top 10 holding for over 10 years. Some relative performance has been sacrificed over the last 3 years, but the brand’s intact, and monetary policy environment is changing.

The downside scenario is that US GDP growth stays too strong, inflation will not come down, and the yield curve remains flat or reinverts.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal, even for short periods of time. All EPS and revenue estimate revisions are sourced from LSEG. The information above, may or may not be updated, and if updated, may not be done in a timely fashion.

Thanks for reading.