As a fundamentally-oriented blog and investor, it’s not often a chart leads off an earnings preview, but it’s warranted for Netflix (NFLX) given the yawning earnings gap that exists for the stock between $700 and $740 per share.

This chart from TrendSpider shows that existing earnings gap from the October ’24 earnings release, which showed 5 ml net add in terms of subscribers and a record operating margin of 30%. In addition, NFLX management seemed to hold to expected ’25 revenue of 15%, although the current estimate expects +12% revenue growth in ’25.

As readers can tell from the TrendSpider chart, the earnings gap from the post-earnings move is still there.

For Q4 ’24, there is much Netflix should be excited about:

- The Christmas Day NFL games were thought to be well received

- Squid Games looks to be another hit

- As I’ve opened Netflix lately, I’m seeing more and more “RAW” events (professional wrestling)

- The ad tier for the lower-paying members, while still growing, saw tempered guidance for ’25 per mgmt

But let’s look at the estimate revisions:

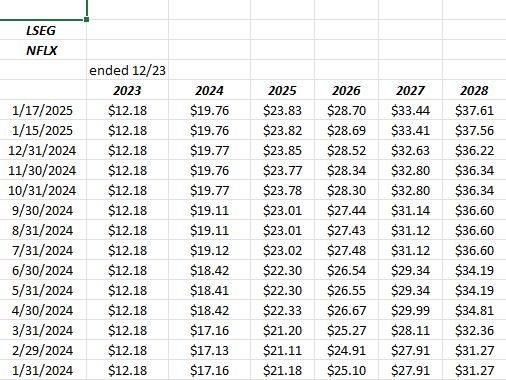

NFLX EPS estimate revisions:

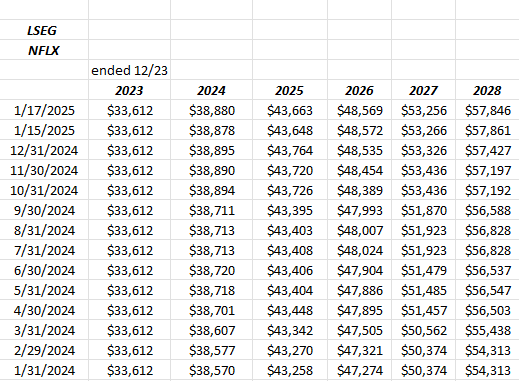

NFLX revenue estimate revisions:

Both of these data sets are sourced from LSEG.

The slight upward revisions to EPS estimates look a little more confident than the revenue estimate revisions, which isn’t surprising for a growth stock like Netflix. The “average” EPS estimate upside surprise from 9/30/21 through 9/30/24 for NFLX is 10%. The average revenue “upside surprise” is 0%.

And the EPS upside surprise is coming from the better operating margin at Netflix, which hit a record of 30% in Q3 ’24. Again, management looks to have guided to 28% for 2025, but no doubt they will have a more refined 2025 guidance forecast next week.

Q4 ’24 estimates:

When Netflix reports their Q4 ’24 earnings after the bell on Tuesday, January 21 ’25, street consensus is expecting $10.1 billion in revenue, $2.2 billion in operating income and $4.20 in EPS, for expected year-over-year growth of 15%, 48% and 99% respectively.

However, all investors will be looking at the 2nd pass at 2025 guidance, which analyst’s currently have modeled at $43.67 billion in revenue and EPS of $23.85 for expected full-year 2025 growth of 12% and 21% respectively. That would be a slowdown from ’24’s expected full-year revenue and EPS growth of 16% and 65% respectively.

Current March ’25 quarterly estimates are expecting 12% revenue growth, 18% operating income and 10% EPS growth.

Valuation:

With NFLX trading at 42x and 35X expected 2024 and 2025 EPS estimates, for expected 65% and 21% growth in ’24 and ’25, the stock is very cheap on the ’24 estimates (albeit with just one quarter left) and looks more expensive on a subdued ’25 estimate.

Despite the tremendous improvement in Netflix’s free-cash-flow the last few years, at 45x and 47X, price-to-cash flow and price-to-free-cash-flow, nothing really looks cheap about the stock, even the 8x price-to-sales.

Only NFLX’s 2% free-cash-flow yield might be a little surprising given the rest of the metrics. Less than 3 years ago, NFLX was generating negative free-cash-flow (FCF) and just over the last 7 quarters, NFLX’s FCF has gone from negative to over $7 billion in FCF.

Summary / conclusion:

The stock has been a good performer the last few years, but mind that earnings gap.

This blog has trimmed small amounts of the shares so a pullback from $830 to the $700 – $740 range wouldn’t be felt too harshly by clients.

NFLX’s market position relative to it’s competition, particularly Disney, and it’s lead amongst it’s streaming competitors is thought to be truly formidable, so pullbacks should be bought for the streaming leader when they happen.

One of this blog’s earlier articles on NFLX from July ’24 talks about the “narrow moat” status that Morningstar has applied to the streaming giant. Morningstar is conservative and doesn’t throw the “wide moat” designation around very easily, but I’ve always wondered what gets NFLX that designation. Even Bob Iger has admitted that NFLX has a nearly-insurmountable lead in streaming.

(Previous articles on NFLX written for readers can be found, here, here and here.)

None of this is advice or a recommendation but rather just an opinion. Past performance is no guarantee of future results. All EPS and revenue estimate revisions are sourced from LSEG. Investing can and does involve the loss of principal, even for short periods of time. None of the above information may be updated and if updated, may not be done in a timely fashion.

Thanks for reading.