Pretty hard to believe, given what we were facing in early April ’25 with “Liberation Day” but the estimated SP 500 EPS growth has risen from 8% in late June ’25 to 10% by late August ’25.

Doesn’t seem like a lot but it’s a bigger move than you’d think in 8 weeks time.

Rates of change:

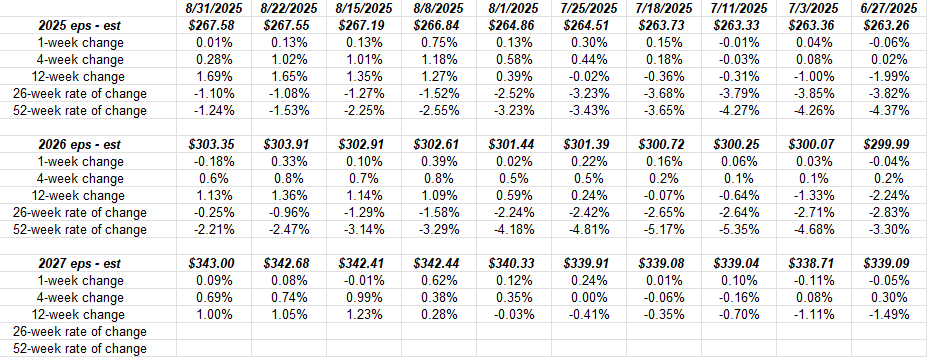

Since late June ’25 all three SP 500 EPS estimates for calendar ’25, ’26 and ’27 have moved higher, and not by a little bit.

The “rates of change” are all improving across most time series.

It’s even more unusual to see the forward years like ’26 and ’27 moving higher at this time: the normal pattern is to be seeing slight revisions lower.

Forward 4-quarter estimates:

- 8/31/25: $283.34 (end of month is Sunday, so that date is being used)

- 8/22/25: $283.03

- 8/15/25: $282.02

- 8/8/25: $282.57

- 8/01/25: $281.15

- 7/25/25: $281.37

- 7/18/25: $280.83

- 7/11/25: $280.60

- 7/03/25: $279.92

- 6/27/25: $269.60

In this weekly progression of the forward4-quarter estimate, there has been only one week – the last week of July to the first week of August – that the sequential FFQE actually declined from the previous week’s estimate.

(Remember, the forward 4-quarter estimate covers the period from Q3 ’25 through Q2’26, so yes it’s a leading indicator for SP 500 earnings, while the vast majority of the data is backward looking.)

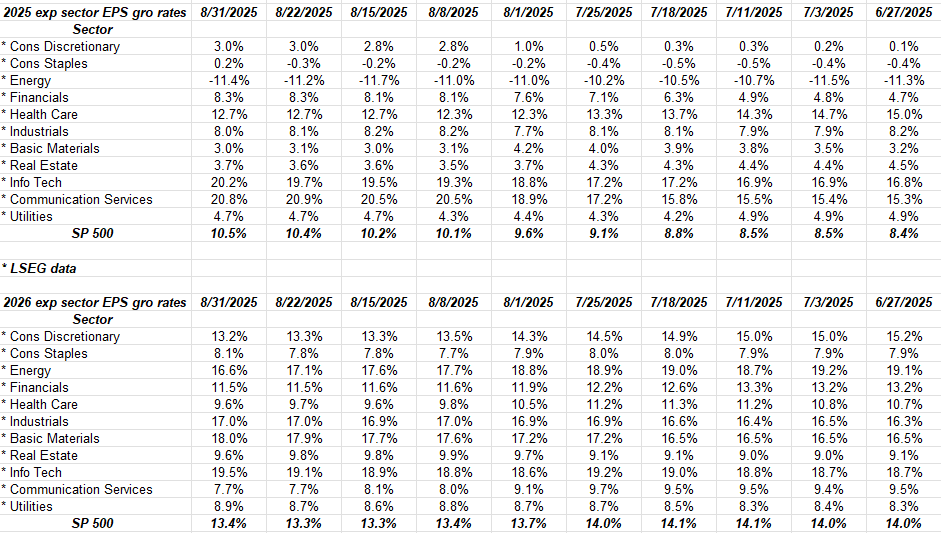

Looking forward by sector:

Technology and communication services are driving all the growth (or most of it anyway) in the SP 500: look at the change in expected calendar ’25 EPS growth rates for technology and communication services since June 27 ’25.

Next year – 2026 – is the bottom half of the above table, and it’s still pretty stable.

Summary / conclusion:

Haven’t done a weekly update in a while, even though the numbers were updated every week.

It’s hard to describe how strong this quarter’s results were: the SP 500 EPS “upside surprise” is still elevated at 7.8%. What’s maybe more interesting is that the SP 500 revenue upside surprise is 2.5%, which is well above 2023’s and 2024 numbers, even though the SP 500 returned 25% each of those years.

Makes you wonder if there is a disconnect with the labor market weakness that seems to be talked about so much. Granted, DOGE layoffs, immigration losses and AI job reductions will matter, but only immigration seems to be in full-force right now.

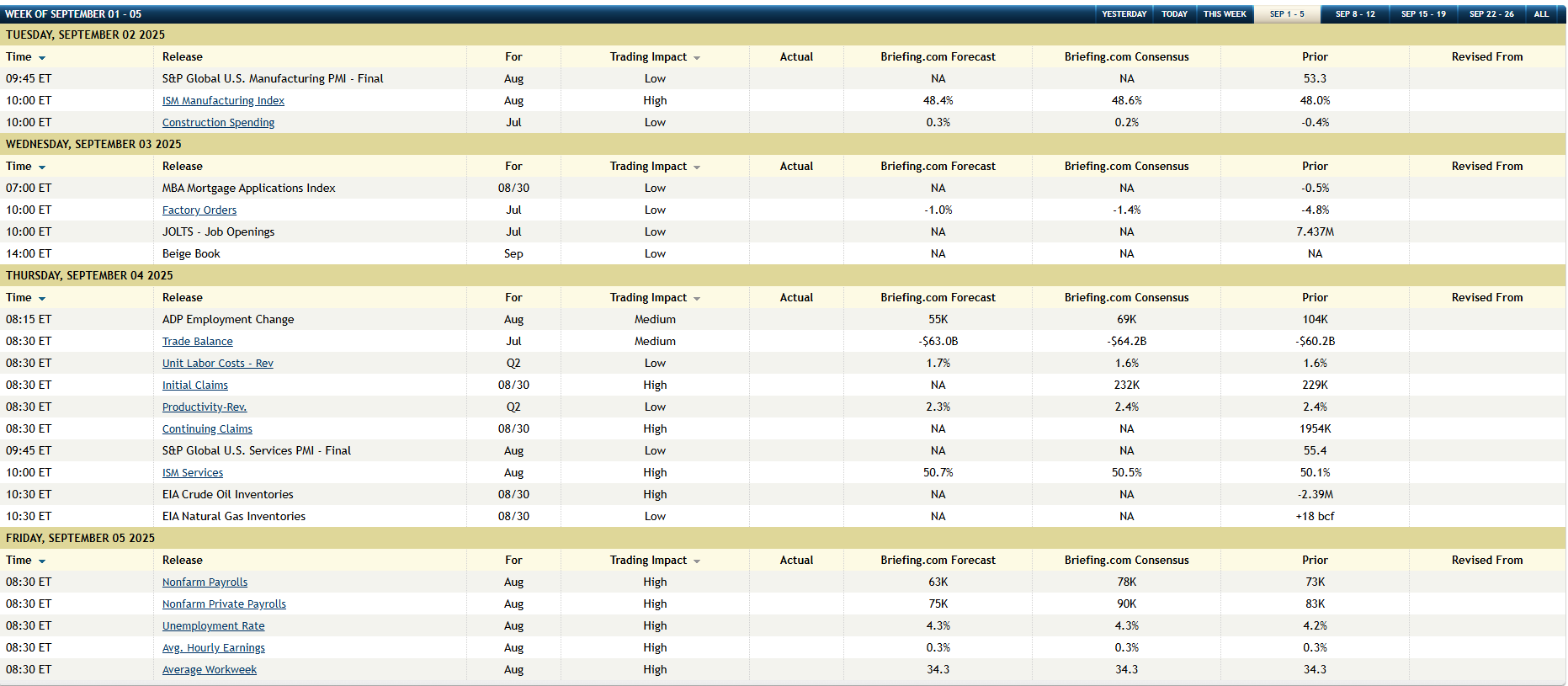

Next week, the August nonfarm payroll report is expected to show job growth less than 100k for both the overall and private sector payroll growth.

Here’s the economic calendar from Briefing.com for the week of 9/1/25:

The nonfarm payroll data is at the bottom of the page.

It feels like we are in uncharted waters with such strong Q2 ’25 GDP revisions and SP 500 earnings growth and yet talking about Fed lowering the fed funds rate, even though the 3 month, 1-year, 2-year, 5-year and 10-year Treasury yields are currently below the fed funds rate of 4.375% and have been for a while.

None of this is advice or a recommendation, but only an opinion. All EPS and revenue data for the SP 500 is from LSEG.com. Past performance is no guarantee of future results.

Thanks for reading.