While the SP 500 is up 10.72% YTD as of Friday, 8/29, so in fact is the Barclays Aggregate and the various credit sectors within fixed-income, having a relatively decent year as well.

Here’s a quick rundown of the SPY, AGG and 60% /40% balanced portfolio:

- SPY: +10.72% YTD

- AGG: +5.01% YTD

- 60% / 40%: +8.44% YTD

If you’d gone to sleep December 31 ’24, and woke up this weekend, you’d think, “wow, not much has gone on in 2025”.

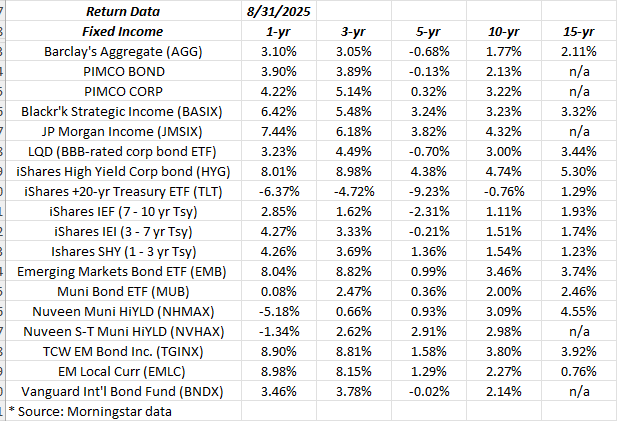

Regular readers know this table as the bond asset class annual returns data looking back 15 years.

An e-mail from a reader this week, asked about emerging market and non-US fixed income returns and the three securities above that capture this data are Emerging Markets Bond ETF (EMB), the TCW EM Bond Inc. (TGINX), and the EM Local Currency ETF (EMLC). One international fixed-income ETF tracked is the Vanguard International Bond ETF (BNDX), but the return isn’t nearly as good as the emerging markets currently.

The weaker dollar is no doubt one reason for the better performance this year, but another reason is that the Fed cut rates twice in late 2024, thus many central banks throughout the rest of the world followed.

Emerging markets tend to have bigger current account issues (and hence more volatility currencies and more frequent devaluations) as well, and thus may have rallied in more stable international economic conditions.

To be frank, I don’t know why EM credit has rallied more than international in 2025 or even for the past few years. Maybe the asset class has simply become more stable than the late 1990’s. In July, 1997, we had the Thai Bhat and Malaysian Ringghit devalue dramatically, after Mexico’s devaluation in late 1994.

Note the 3-year returns too in the emerging-market securities. The EM’s have been a good place to pick up extra yield for a few years now.

This blog’s single-largest position is Andy Norelli’s JPMorgan Income Fund, which is having another good year versus the AGG, just not quite as strong of outperformance as last year.

While high yield and investment grade credit spreads are near all-time-tights, the high-yield ETF’s like HYG and SHYG are still performing well. The question is, does a 5% – 6% annual return on high yield warrant the risk with the very tight credit spreads ? Most would probably say no.

My own opinion is that what’s keeping the bid under high yield is economic data like last week’s Q2 ’25 GDP revision from 3% to 3.2%, as the Fed seems to be leaning easier (at least until we see this week’s August payroll data and the next week’s August CPI / PPI data).

It’s hard to imagine a better environment for taxable high-yield credit than 3% GDP growth and the prospect for lower fed funds rates.

Municipal bond returns are mostly negative for the credit space, while the MUB (National municipal bond ETF) is just barely positive. The OBBB likely did muni’s in since muni’s find much better demand when the Democrat’s are controlling the White House and the Congress (think ordinary income tax rate hikes).

Summary / conclusion: A 25 basis point rate cut in the fed funds rate in mid-September still only brings the fed funds rate down to 4.125%. Ultimately I would think that the current Administration wants that fed funds rate well below 4%.

Still, an easier Fed will likely continue to keep a bid under the majority of bond market asset classes for the rest of the year.

Don’t forget to look at the TLT (+20-year Treasury ETF): that’s a murderers row of ugly returns out to 10 years. The 10-year return is still positive at +1.59%, but over the 15-year period, it likely doesn’t come close to a positive, real, (i.e. inflation-adjusted) return. So why hold Treasuries ? It’s a flight-to-quality instrument, when the VIX is spiking and market fear is elevated: even during Liberation Day as the SP 500 corrected 20%, the 10-year Treasury yield traded down to 3.88% – 3.89%. The TLT traded up to $94 (in price) and has since sunk back down to the mid $80’s, as market fear has dissipated.

Ultimately this was going to be a tough decade for fixed-income after 8 years of zero interest rates (2008 – 2016) and then again during Covid.

None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future results. All return data sourced from Morningstar.

Thanks for reading.