Thursday night, October 17th, Netflix will release their 3rd quarter, ’24 financial results after the closing bell.

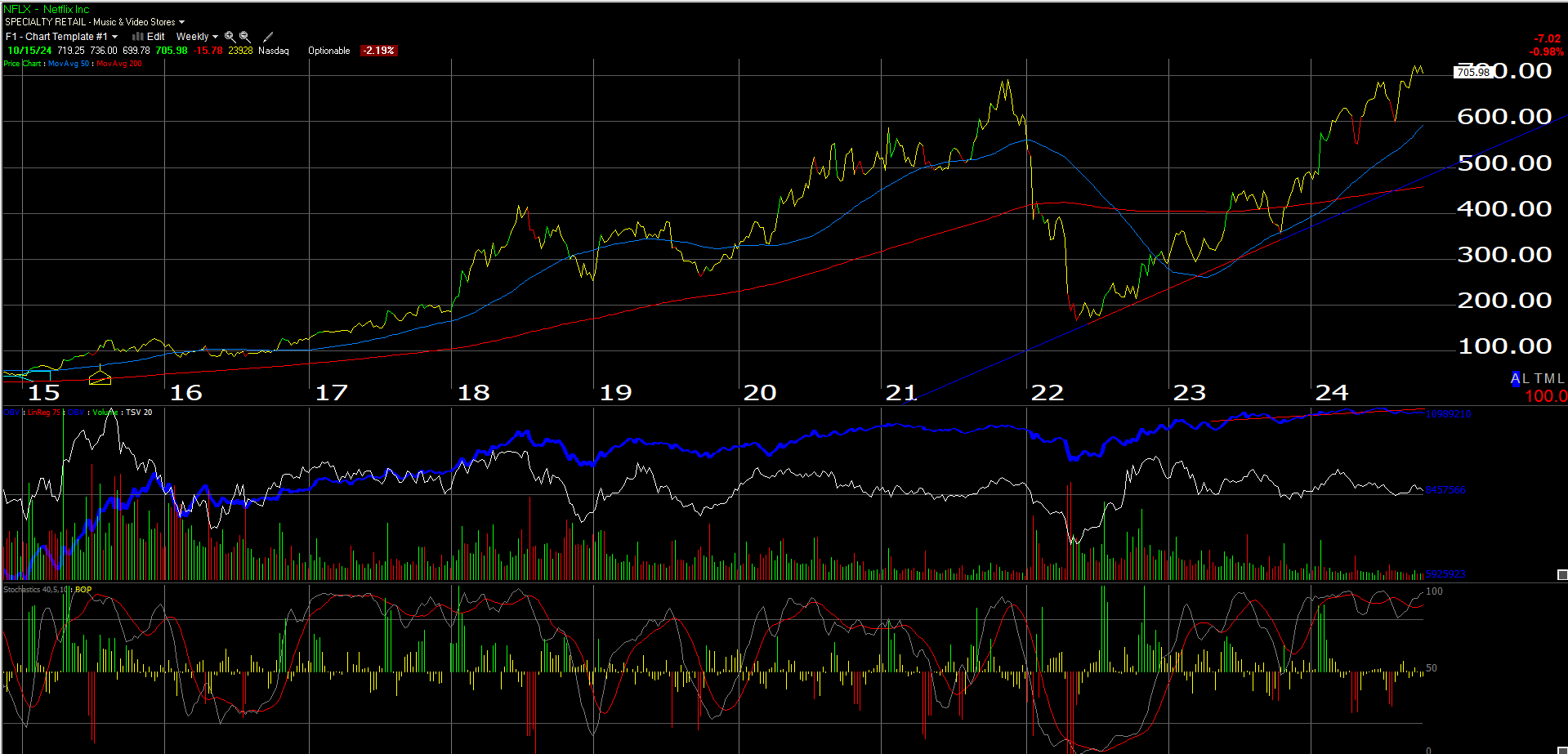

With the stock’s valuation, it’s always a “heart attack on a plate” waiting for Netflix’s numbers, but the streaming giant has continued to deliver for shareholders, and the important technical metric is, in the last month, Netflix has traded over $700, or it’s 11/19/21 high print of $700, and the stock has remained above that key level. That being said, it hasn’t been a robust “breakout” but more of a lackluster move above the Nov ’21 peak.

It’s rare for a fundamental analyst to start an earnings preview off with a chart, but here’s Netflix’s weekly chart:

Speaking of technicals, the SP 500’s growth stock leadership of the last few years hasn’t traded well since late June, early July, ’24, lagging the SP 500 and some other asset classes in the 3rd quarter ’24, and the fact is Netflix is part of that crowd. It’s not part of the “Mega-cap 7” so to speak, but Netflix is valued like those names, and thus subject to the bottom falling out of bed on a numbers miss.

Fundamental and valuation metrics:

When Netflix reports their results Thursday night, after the bell, consensus sell-side estimates will be expecting $5.12 in EPS on $9.77 billion in revenue for expected y-o-y growth of 37% and 14% respectively. The consensus operating income estimate is $2.72 billion and is expected to be up 37% y-o-y.

In the June ’24 quarter, NFLX reported 17% revenue growth, 38% operating income growth, and 48% EPS growth, all y-o-y.

There is no question the biggest improvement in Netflix’s fundamentals the last 3 years has been the improvement in operating cash-flow and free-cash-flow. In the Sept ’22 quarter, NFLX’s trailing-twelve-month (TTM) free-cash-flow has just $533 million, and in the subsequent 7 quarters since then has risen to $6.8 billion as of the June ’24 quarter. Consensus estimate for free-cash-flow per LSEG for Q3 ’24 is $1.7 billion.

LSEG’s free-cash-flow estimate for calendar ’24 is $6.4 billion and they could be past at $6.6 billion by the 3rd quarter, depending on Thursday night’s release.

Morningstar has a $10 billion free-cash-estimate for Netflix by the end of 2028.

As of today’s price, Netflix sports a 2.2% free-cash-flow yield, which is unusual for a growth stock trading at 37x ’24 EPS.

Netflix is trading at 37x expected ’24 EPS of $19.13, which is 60% growth over 2023’s actual EPS of $11.99. Looking out using ’24 to ’26 EPS averages and PE averages, the stock is trading at 33x a three-year average EPS for expected 31% growth, so on a “PE-to-growth” basis, there are some doubters on the expected EPS growth.

To round out the valuation metrics, NFLX is trading at 7x price-to-sales, and 29x and 41x price-to-cash-flow and price-to-free-cash-flow.

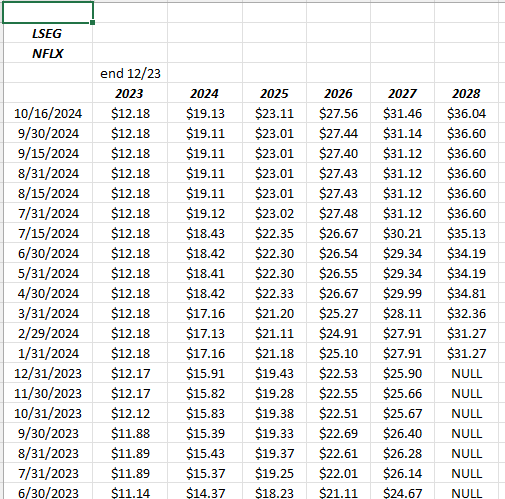

Here’s a quick look at EPS and revenue estimate revisions for Netflix:

EPS:

That’s an 18-month look for Netflix. That’s a 31% increase in the EPS estimate from 6/30/23 through 10/16/24 for 2024 and then a 27% increase for the same period for 2025. Roughly 8 quarters ago, estimates were looking for high 20% EPS growth for 2024, today, the expected EPS growth for NFLX for 2024 is 60%.

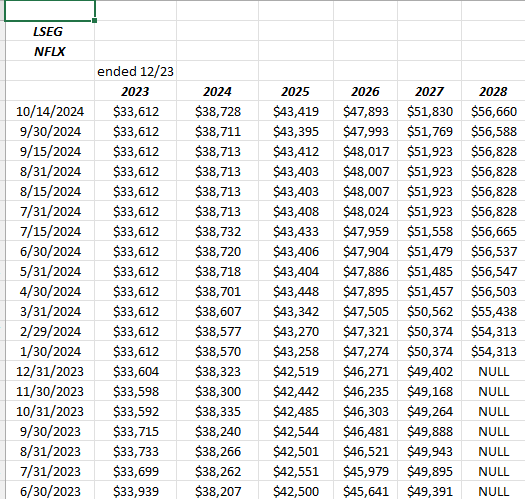

Revenue:

The revenue estimate revisions are much smaller for Netflix, although analysts probably understand this as the US streaming market is reaching some saturation (thought US and Canada is 60%, which still seems like some room for growth to me), and Netflix’s member growth will come from other other geographies like Southeast Asia, India, South America, and maybe a little more in Europe and Canada.

The Next Big Thing:

On August 20th, 2024, Variety Magazine released a story that noted that Netflix’s “upfront advertising” had doubled and then the company came out and confirmed with this (cut-and-pasted from Briefing.com)

![]()

(Click on above)

Here’s what followed from the sell-side analysts after this advertising update:

- 8/21/24: TD Cowen analyst sees ad revenue growing from 4% to 13% by ’29;

- 8/30/24: Pivotal Research boosts NFLX price target (PT) to $900

- 9/13/24: JPMorgan analyst Doug Anmuth says NFLX ad tier revenue to reach 10% of total rev by ’27;

- 10/1/24: KeyBanc analyst raised NFLX PT to $760;

- 10/7/24: Barclay’s downgrades NFLX to underweight;

- 10/7/24: Piper Sandler upgrades NFLX to overweight;

- 10/10/24: Oppenheimer upgrades NFLX PT to $775;

- 10/11/24: Guggenheim upgrades NFLX PT to $810;

- 10/16/24: Loop Capital upgrades NFLX PT to $800;

Bet that Barclays analyst feels lonely.

That incremental ad revenue, while small today, is likely revenue with a greater margin than the traditional streaming business.

Morningstar has a target 30% operating margin target on NFLX by the end of 2028, (NFLX’s operating margin was 26% in June ’24 quarter and 28% in March ’24 quarter).

Finally, per some of the sell-side comments, NFLX is due to hit subscribers with another subscription price increase, supposedly before year-end ’24.

Summary / conclusion:

There is a lot of nervousness around Netflix’s earnings coming into Thursday night, but that’s always the case given the valuation. If readers cannot handle a pullback in the stock to $600 or even $500 in the stock, then be sure and adjust your risk coming into earnings.

I am less nervous after writing this earnings preview given the above commentary and results around the advertising business or “ad tier” as sell-side analysts call it.

It’s clear that NFLX’s advertising “flywheel” so to speak, might lead to additional revenue opportunities, but what those might be aren’t entirely clear yet. The two NFL football football games that will be offered Christmas Day could be an additional for Netflix given the 4th quarter every year is typically NFLX’s weakest quarter.

Given how growth stocks are trading, the thought was to trim some NFLX prior to the release, but now, expect positions to be held as is coming into Thursday night’s earnings release, even though the stock could easily trade off $50 after release.

Longer-term it’s clear that NFLX’s business model is just crushing the competition. When Bob Iger of Disney came out in the last 3 – 4 months, and openly paid homage to NFLX’s dominance in streaming, it caught my attention. Tough competitors usually don’t do that.

Could Netflix be putting in a big double-top on the weekly chart, shown above ?

Absolutely. Know your risk.

The EPS and revenue estimate revisions should give readers at a least a little comfort around sell-side expectations.

Here’s some articles written on Netflix in previous quarters, both earnings preview and then a follow-up: July ’24 here, here, March ’24, here, and here. And there’s more on the this blog’s website.

Netflix was up 45% YTD after Tuesday night’s, October 15th, 2024 market close, a little less than 2x the SP 500’s YTD return.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. All EPS and revenue estimates are sourced from LSEG. Readers should gauge their own comfort level with portfolio volatility and adjust accordingly. Investing can involve the loss of principal, even on a short-term basis.

Thanks for reading.