Morgan Stanley is scheduled to report 3rd quarter, 2024, financial results on Wednesday morning, October 16th, before the opening bell.

Analyst consensus Wednesday morning is expecting $14.4 bl in net revenue to generate $1.58 in EPS for y-o-y growth of 9% and 14%.

Last quarter, Q2 ’24, net revenue grew 12% and generated 47% EPS growth as management fees rose 16% as Institutional Securities was the star of the quarter. Morningstar noted that Wealth Management’s operating margin at 27%, was still below management’s targeted goal of 30%.

Full-year ’24 expectations are for EPS to grow 24% on 9% revenue growth, as Morgan Stanley has basically now divided the firm between the brokerage and wealth management businesses and the old investment bank or institutional securities business.

The big kick in the 2nd half of ’24 is expected to be investment banking fees, which one sell-side firm has targeted at 48% y-o-y growth, vs the 32% first half of ’24 y-o-y growth.

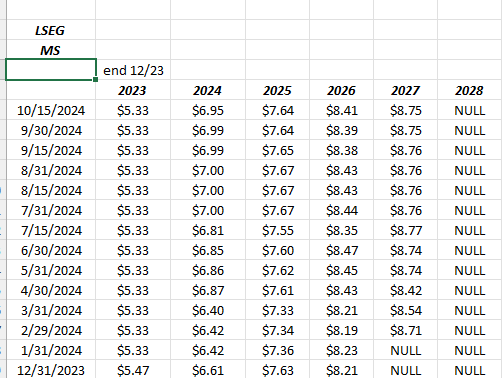

EPS estimate revisions:

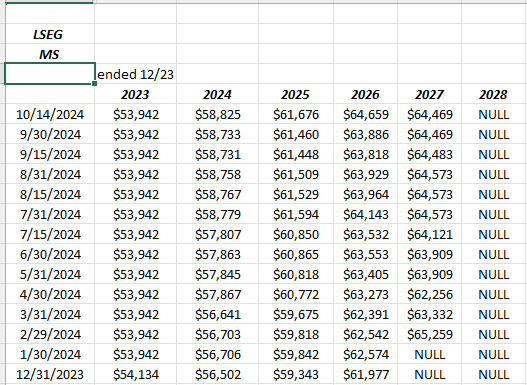

Revenue estimate revisions:

The Morgan Stanley revenue estimate revisions have been steadily positive the last 10 months.

Given this, we should probably expect some degree of “upside surprise” from Morgan Stanley Wednesday morning.

Valuation:

Morgan Stanley is still just trading at 16x expected ’24 EPS of $6.95 – $7.00, for expected y-o-y growth of 28%. The next three years “average” EPS growth is expected at 16%, and the average PE using $110 per share and the forward estimates is 14x, so MS remains cheap on a PEG (PE-to-growth) basis.

Technically, the stock broke out to a 4-year high last week, which is always a good sign.

Summary / conclusion: My own opinion is that Morgan Stanley did a far better job of maintaining and executing in the wealth management business, than Goldman Sachs has in the last 10 – 15 years.

Goldman Sachs was sold last week from client accounts (and it wasn’t a big position) although the banker giant should report a good quarter tomorrow morning, i.e. Tuesday, 10/16/24.

Going forward, clients will likely own more Morgan Stanley than Goldman Sachs, as I think Morgan is better positioned with the wealth management business than Goldman.

Both Goldman and Morgan Stanley carry a “narrow moat” rating from Morningstar. Of the two, with Morgan Stanley’s having done the better job of executing in wealth management, Morgan Stanley should have the more consistent and dependable earnings growth, as well as hold it’s value better in a down market.

None of this is an advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal even for short periods of time. All EPS and revenue estimates are sourced from LSEG. Readers should gauge their own comfort with portfolio volatility and adjust accordingly.

Thanks for reading.