Bank of America (BAC) is scheduled to report their 3rd quarter, ’24 earnings release on Tuesday morning, October 16th, ’24, with consensus expecting $0.77 in EPS on $28.3 billion in net revenue for expected y-o-y growth of -14% on flat or 0% revenue.

To say the sell-side has subdued expectations for Bank of America is an understatement, although this preview of the financial sector numbers was also subdued given the tough compare with 2023.

Low expectations can be a good thing, particularly in a bull equity market.

One major positive to (BAC) in my opinion is the way the stock absorbed the selling by Berkshire of Hathaway of a substantial part of it’s Bank of America position. Per the mainstream financial media, Mr. Buffett has reduced their BAC position to under 10% of outstanding.

Two issues have supposedly hurt the stock over the last few years: a liability-sensitive balance sheet, which means BAC’s liabilities have re-priced faster than assets, which is not necessarily a good thing with fed funds rate increases and a term structure that has seen higher yields from early ’22 through late ’23, and issues around expense control, or the sell-sides desire for better expense control (let’s put it that way).

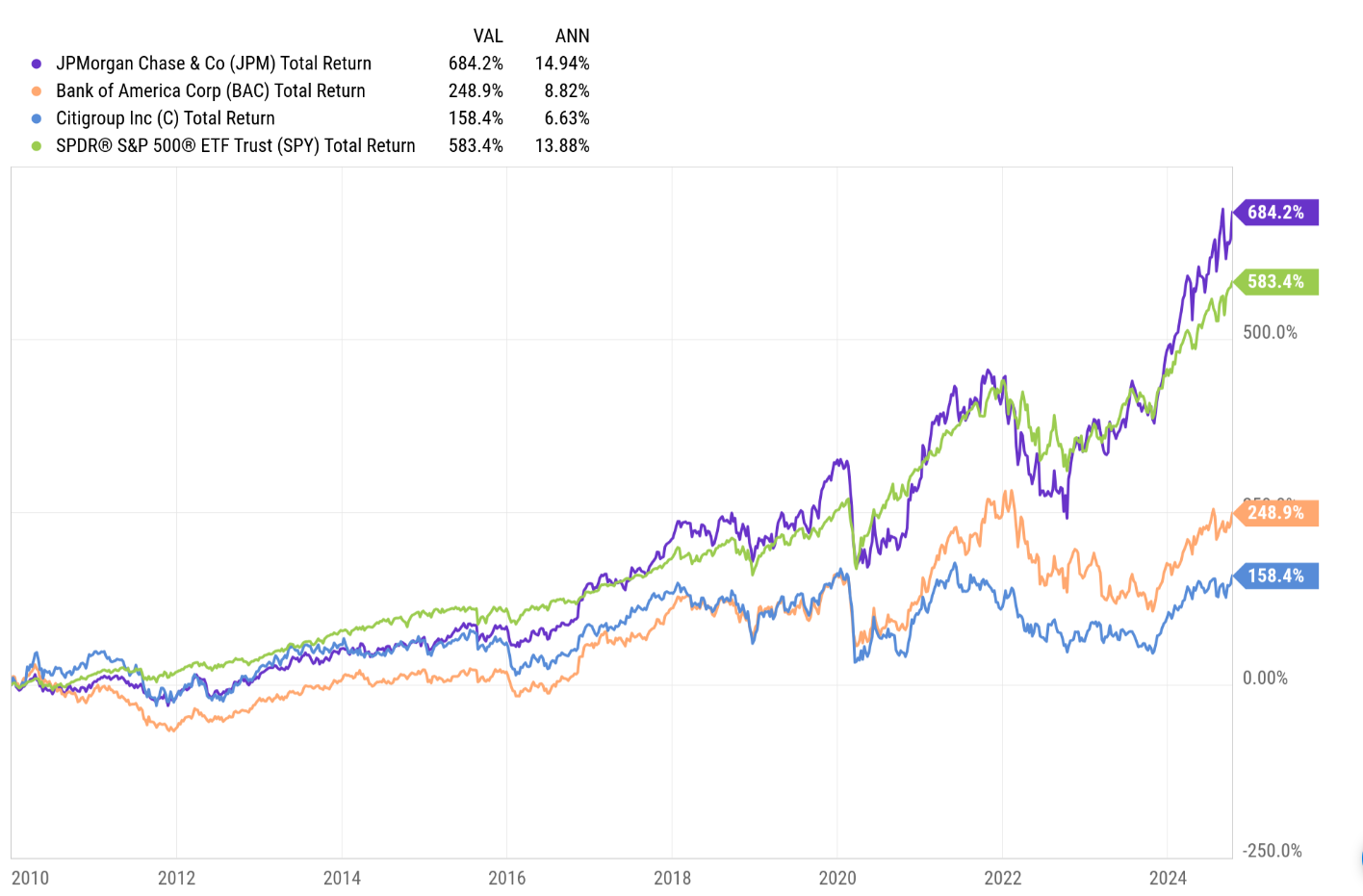

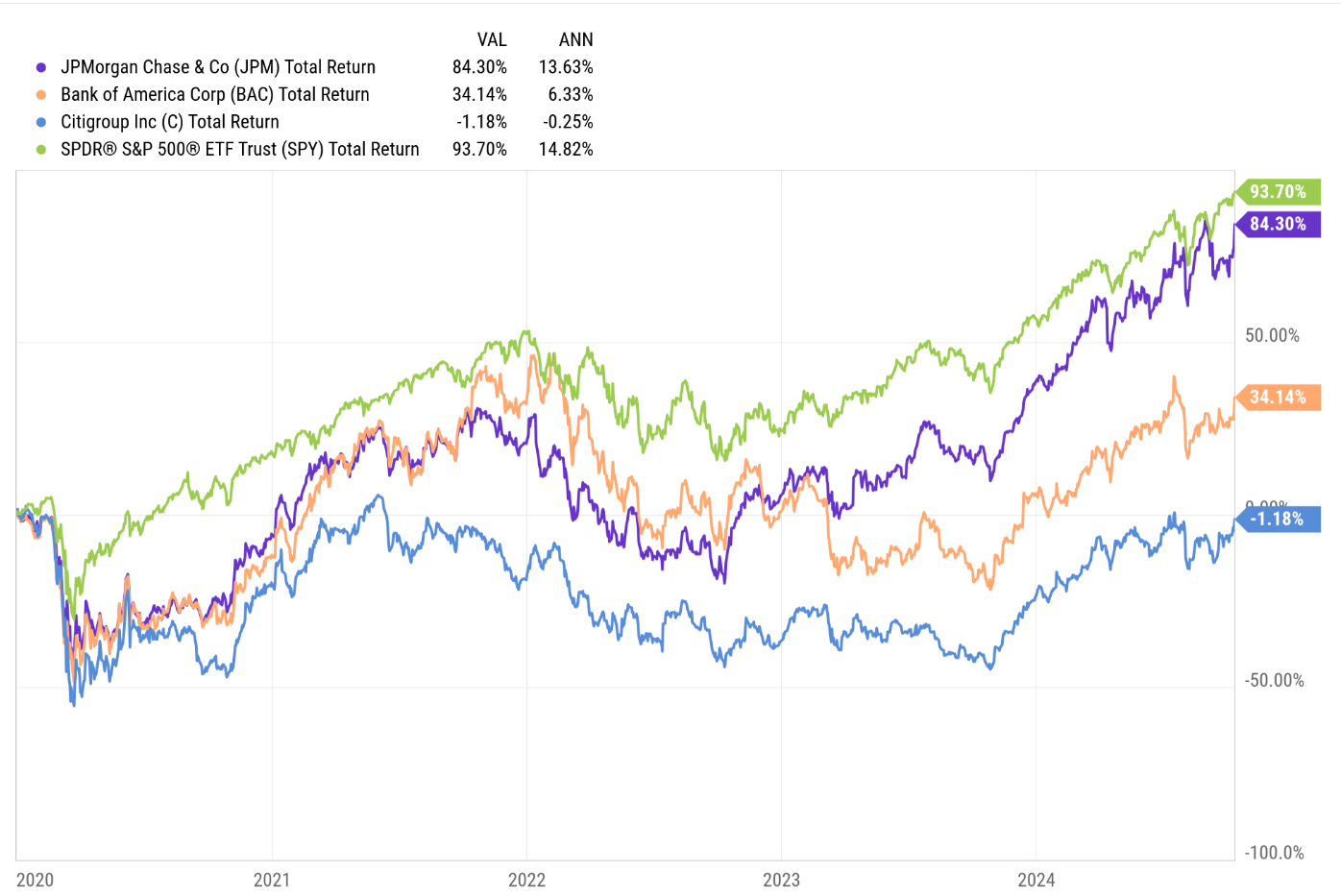

Here’s the longer-term performance charts of our favorite banks:

Looking back to 1/1/2010, only JPMorgan is beating the SP 500 (SPY).

Since 1/1/2020, none of the above bank stocks have managed to beat the SP 500 (SPY).

As you’d expect JP Morgan’s total return is pretty close to the SP 500’s this decade, as of 10/11/24.

Valuation:

For full-year 2024, BAC is expecting 1% revenue growth on -6% EPS growth so the results seems rather contained for the bank giant. The next 2 years – ’25 to ’27 BAC consensus is expecting 5% revenue growth to generate 13% – 15% EPS growth.

Today, at $42 per share BAC is trading at 13x an expected ’24 EPS of $3.21 and with a 3-year average PE of 12x, EPS growth is expected to average 7%.

Trading at 1.2x book and 1.7x tangible book value (TBV), Bank of America is much more modestly valued on a book basis, than say JP Morgan, but not as cheap as Citigroup (C), which will follow this earnings preview.

Bac also sports a lower teens ROTCE (return on tangible common equity), much lower than JPM, but higher than Citigroup.

BAC’s stock price peaked in early ’22 at $50 per share in January and then again in February ’22. It should be able to easily trade back that level in a good market for financial stocks.

Citigroup (C) earnings preview:

When Citigroup (C) also reports their 3rd quarter ’24 financial results Tuesday morning, October 16th, analyst consensus is expecting $1.31 in EPS on $19.8 billion in net revenue for expected y-o-y declines of -14% and -1% respectively.

In the 2nd qurater of ’24, Citi grew net revenue of +3%, on EPS growth of +14%. Jane Fraser is trying to reduce headcount, but as of the 2nd quarter Citi’s total headcount was 229k, down from a peak of 240k, but well up from 220k in December, 2020. I’ve heard both ways on expected headcount changes, i.e. headcount reduction is done, and there is more to come.

In terms of relative sector performance, looking at the above 14-year and 4-year total returns respectively, Citigroup has been a big laggard although Jane Fraser has started to turn the bank around operationally. Citi’s ROTCE is below that of BAC and well below that of JPMorgan, but on a book value basis, Citi is the cheapest of the bigger banks.

Its Citi’s book-value (BV) and tangible book value (TBV) valuations: Citi’s book value as of the June ’24 quarter was $99.70 per share while the $87.50 per share, leaving Citi trading at 0.66x BV and 0.76x TBV at that time.

The expected ROTCE for Citi (per Morningstar) is 10% – 12%, which is an improvement from Citi’s 7% historically.

Summary / conclusion: Many of the major banks (and certainly the regionals) have not made new all-time-highs since 2021 given the impact of fed funds rate hikes on the bank balance sheets, but if BAC can trade over $55 (2006 high) it will make a new all-time-high and if Citi can trade over $80, (mid-2021 high), it too will have made a post-2008 new high.

JPMorgan is the cream of the crop, but from a portfolio construction standpoint, BAC and C can provide a defensive element to the financial services weighting, within portfolios. Better expense control comes up with both BAC and C in terms of ’24 and ’25 expectations, so that’s one avenue to add incremental EPS growth, and it’s completely under management control.

For both banks, expected 2025 and 2026 EPS growth is expected to be stronger than in 2024, but let’s wait and see what guidance holds in January ’25.

The fact is both BAC and C, are less-momentumy (not a great word) than a JPM, and thus would likely probably hold their value better in a decent correct of 15% – 20%. Both stocks recently increased their dividend, with Citi now sporting a 3.25% yield.

It’s an almost perfect environment for the larger banks that were just decimated in 2008, with mostly very good consumer credit activity, corporate loan growth still in the 3% – 4% range, net interest income after rate hikes offering additional portfolio yield and higher net interest margins, solid capital market activity particularly on the bond side as credit spreads remain tight, and home prices still rising, not to mention an easier Fed. The only negative heard on the capital market side is a lack of any IPO market, or at least much smaller than expected given the strength in US equity markets.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal, even for short periods of time. All EPS and revenue estimates are sourced from LSEG.

Thanks for reading.