Next week, Q3 ’24 earnings start and the majority of the interest on the part of investors will be Friday, October 11th’s financial services earnings, from JP Morgan (JPM), Wells Fargo (WFC), Blackrock (BLK) and BNY Mellon.

![]()

What’s interesting about this table from Briefing.com is that of the financial services companies reporting next Friday, 10/11, only one – BNY Mellon – shows y-o-y EPS growth expected for Q3 ’24.

For the sector as a whole, financial services is presently looking for just +1.8% EPS growth in Q3 ’24, versus the +23.5% compare in Q3 ’23, and +4.3% revenue growth expected in Q3 ’24, vs +5.1% in Q3 ’23.

That’s a tough EPS compare (as it stands right now).

The fact is though a few quarters since Q3 ’23 have had low expectations for the financial stocks coming into the quarter’s releases, and then the numbers were quite good: low credit reserves, strong capital market activity, mid-single-digit corporate loan growth, relatively healthy home sales (i.e. mortgages, etc.) all generate positive EPS attribution, particularly for the bigger banks.

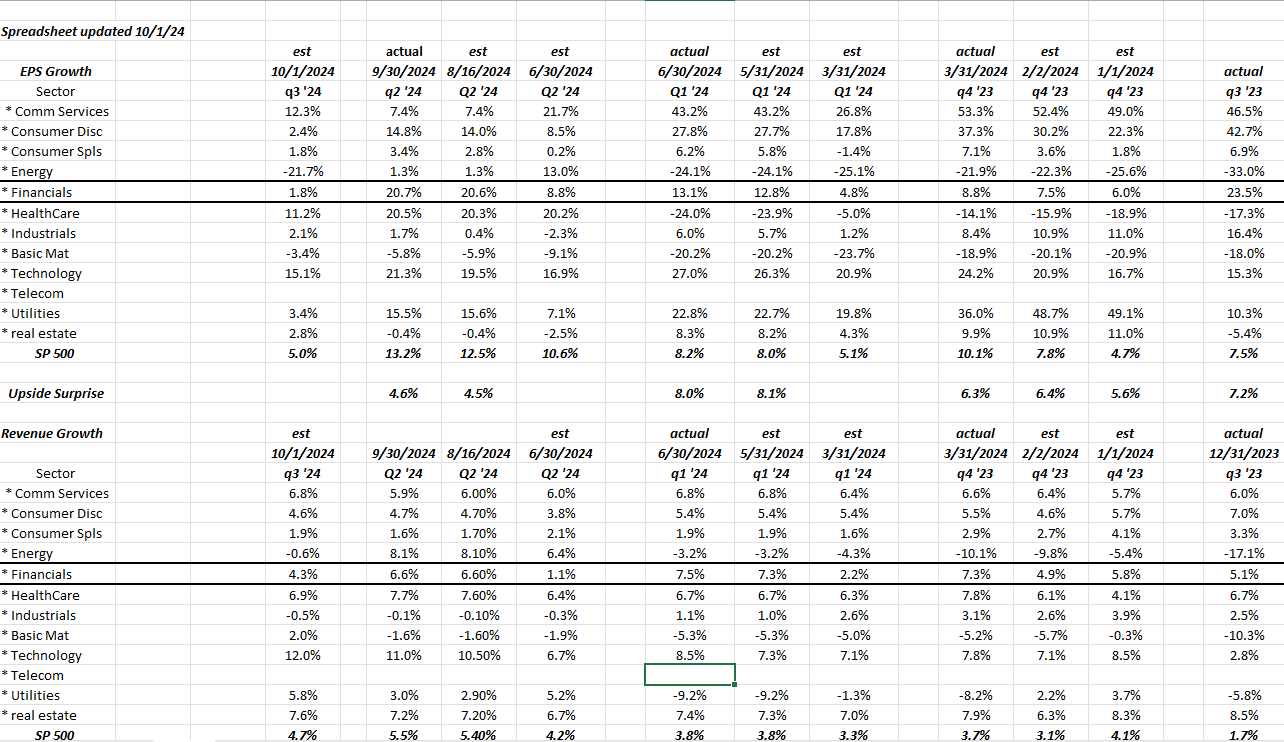

Here’s a table that’s a little wonky, but readers can see the progression in EPS and revenue growth for the Q4’23 through Q2 ’24:

LSEG is the source of these growth rates. The black-bordered line is the financial sector.

Surprising to me was that the financial sector was expecting just +4.8% EPS growth in Q1 ’24, and the actual was more than double that amount at +13.1%. Q2 ’24 same way +8.8% expected at the start of the quarter, while actual was +20.7%.

Revenue growth has been relatively consistent at 5% – 7% since Q4 ’22.

Who wins in today’s environment ? Same ‘ol, same ‘ol, i.e. major banks like JPM, and Bank of America (BAC), Wells Fargo (WFC), which should reflect very positive credit profiles and the addition of strong capital markets activity. Goldman Sachs (GS) and Morgan Stanley (MS) too.

The regional banks will likely only start to outperform when the Treasury yield curve steepens and the Treasuries bought for bank portfolios, begin to “ride the yield curve”. (You have to have read Homer & Leibowitz in business school to get that reference.)

SP 500 data:

- The SP 500 saw it’s quarterly bump this week to $266.66 from $257.47 last week, or roughly the amount that was expected in last week’s update.

- The PE on the forward estimate is 21.5x versus 22x last week;

- The SP 500 earnings yield jumped to 4.66% with the quarterly bump versus the 4.48% last week;

- The “kinda” red flag around Sp 500 EPS is that Q2 ’24’s EPS estimate started the quarter out at $59.22 on June 30, and ended up at $60.40 as of 10/4/24, which is just a 2% increase. Also the upside surprise for SP 500 EPS this quarter was just 4.6% versus the 6% – 8% in the previous quarters.

It’s not a “sell everything’ tell, but it’s clear that the sell-side may be pulling in their horns on expected Q3 ’24 SP 500 EPS growth.

That’s understandable too.

For the SP 500 as a whole, EPS growth is expected at 5% in Q3 ’24, on 4.7% revenue growth.

Summary / conclusion:

This blog will be out with a JP Morgan preview before Friday morning, along with some other financial names, but this blog doesn’t model Blackrock or Wells Fargo. This blog turned a little more conservative on JPMorgan before Q2 ’24 earnings were released, since there is a good chance that Jamie Dimon will be leaving the bank, possibly within 3 years, and maybe even sooner since if Republican nominee Trump is elected, he has indicated that Jamie Dimon will be a candidate for Treasury Secretary. JPM is the most expensive large bank on a book value basis, but the fact is Jamie has run that bank like a well-oiled machine since even pre-2008.

The nonfarm payroll report will likely give the “econ bulls” some ammunition as the Atlanta Fed’s “Nowcast” shows expected Q3 ’24 GDP growth at +2.5% (as of October 1 ’24).

That’s still healthy growth, and that likely continues to bide well for continued health in consumer credit metrics like credit card chargeoffs, home equity, auto loan delinquencies, etc., etc.

None of this is a recommendation or advice, but only an opinion. Past performance is no guarantee of future results. All SP 500 EPS and revenue data is sourced from LSEG. Investing can and does involve the loss of principal, even for short periods of time.

Thanks for reading.