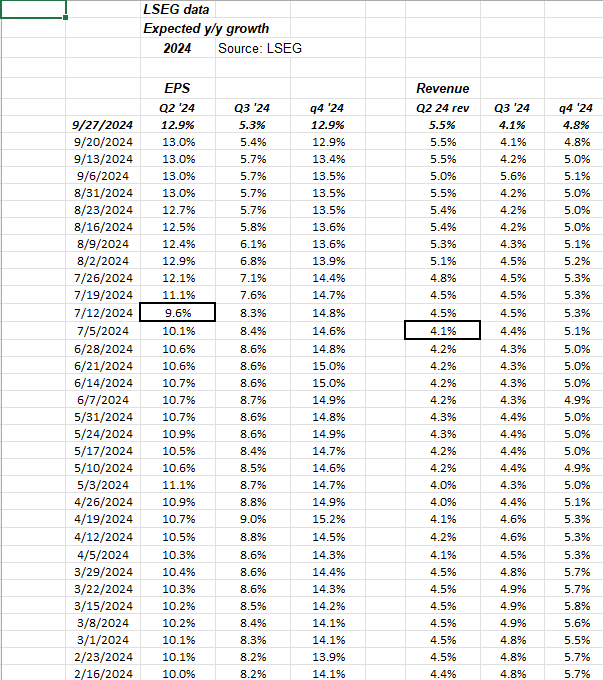

Here’s a quick look at how Q3 and Q4 ’24 EPS and revenue growth have trended since early in ’24.

The spreadsheet is internal, but the data is updated weekly and sourced from LSEG.

The black-bordered boxes show the nadir for expected Q2 SP 500 EPS and revenue growth. Readers should expect Q3 EPS and revenue growth for the SP 500 to bottom within the next two weeks, and then once Q3 ’24 financial results start to get released, the expected quarterly EPS and revenue growth should tick higher.

The big difference between Q2 ’24 and Q3 ’24 EPS growth is expected to be the energy sector, which is of 9/27, is expected to show a drop of 20% once Q3 ’24 earnings start. As of today, energy is expected to show an EPS decline of -20% in Q3 ’24, on a drop of -3.7% revenue.

What’s maybe more interesting is that the energy sector is facing a very tough comp from Q3 ’23, when energy sector EPS fell 33% and energy revenue fell 17%. Usually, that’s an easy compare and a low hurdle to beat from a reporting perspective, and yet the Q3 ’24 numbers are not expecting any bounce.

For Q3 ’24, the sector with the best, expected y-o-y EPS growth is still technology at 15%.

SP 500 data:

- The forward 4-quarter estimate fell this last week to $257.47, down from lasty weeks, $258.76 and the quarterly start at $261;

- The PE ratio on the forward estimate is 22.3 versus last week’s 22x and the quarterly start of 21.6x;

- The SP 500 earnings yield slipped to 4.48% last week from 4.54% and has now fallen steadily since the 8/2/24 “yen carry trade” peak near 4.87%;

- The big difference this quarter in the SP 500 quarterly earnings results, was the “upside surprise” fell to 4.6% from the last 5 quarter’s strength, well above 4.6%.

When the quarterly roll happen Tuesday, expected the forward 4-quarter estimate next week to be up near $267 per share, since the quarterly estimate will now be Q4 ’24 – Q3 ’25, versus this quarter’s Q3 ’24, versus Q2 ’25.

If you look at how the “expected” forward 4-quarter estimates look over the next few quarters:

- Q3 ’24 – Q2 ’25: $257.47

- Q4 ’24 – Q3 ’25: $267’ish (that will change a little by next Friday, 10/4);

- Q1 ’25 – Q4 ’25: $277.28 (calendar ’25);

Note the expected $10 increase per quarter as we roll forward.

Let’s see if that changes as Q3 ’24 earnings start.

Summary / conclusion:

In terms of YTD performance, the stalling out of the top 10 mega-cap names in the SP 500, (MSFT, AMZN, GOOGL), is indicative of the subtle shifts occurring beneath the surface of the SP 500.

Technology faces tough comp’s in Q3 and Q4 ’24, – versus 20234 – when technology sector grew EPS +15% in Q3 ’23 and +24% in Q4 ’24.

It’s highly doubtful technology comes apart like it did from March, 2000 to early, 2023, but high PE names see PE compression, when growth slows, even just a little. Microsoft is still 10% or $40 below it’s all-time high.

Maybe even more interesting is what happened in China this week.

Looking at EEM (iShares Emerging Market ETF) and VWO (Vanguard’s Emerging Market ETF), both saw sharp increases this week in YTD returns: The VWO’s YTD return as of last week, 9/20/24 was +11.05%, versus this week’s YTD return of +18.31%, while the EEM’s YTD return as of last week, 9/20/24 was +9.41%, versus this week’s YTD return of +16.72%.

China is +30% of the market cap of the emerging market benchmark, and the world’s 2nd largest economy, when ranked by annual GDP growth.

Personally I think China is un-investable. That country is still faux capitalism, to a large degree. Just the presence of SEO’s (state-owned enterprises) is a red flag.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. All SP 500 EPS and revenue data is sourced from LSEG, unless specifically noted. Investing can and does involve the loss of principal even for short periods of time. Readers should gauge their own comfort with portfolio volatility and adjust accordingly if needed.

Thanks for reading.