Netflix reports after the closing bell on Thursday, July 17th, 2025.

Sell-side analysts are looking for $7.08 in earnings per share on $11.07 billion in revenue for the streaming giant, and expectations for $3.6 billion in operating income. Expected y-o-y growth for all three of these metrics is 45%, 16%, and 45%.

Q1 ’25 saw revenue up 13%, operating income +37% and EPS +21%. With Q4 ’24 results reported in January ’25, Netflix guided to a 29% operating margin for calendar ’25, while with the Q1 ’25 earnings saw Netflix guide the operating margin to 33% for calendar ’25.

Netflix has been steadily walking up the operating guidance for the last few years, which is a considerable positive for the stock. My question is “What’s peak operating margin for the streaming giant” ?

The last year subscriber growth in the US & Canada has been tempered as the other global geographies continue to grow mid-teens to low 20%. Netflix management pulling back on reporting subscriber growth hasn’t impacted the stock much as the streaming king is adding revenue from areas like advertising revenue, which is likely higher-margin revenue than the traditional content business.

Netflix’s move into live sports has also been well received

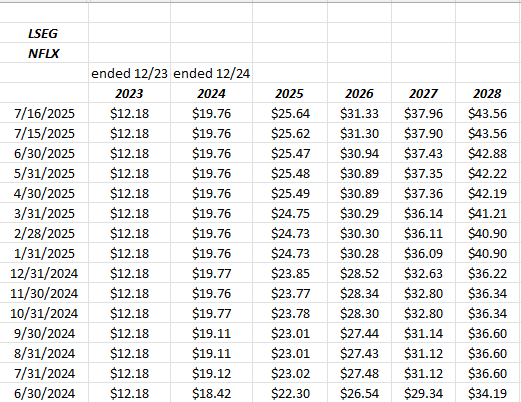

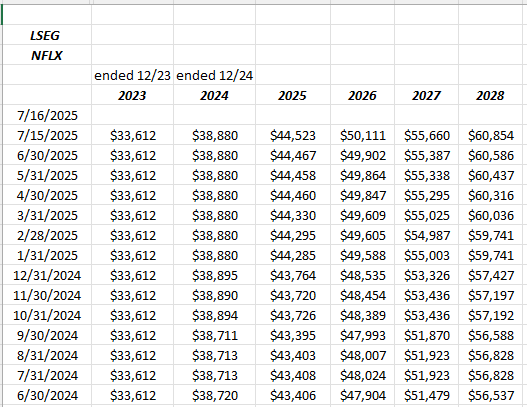

NFLX EPS and Revenue estimate revisions:

The EPS estimate revisions have been consistently higher the last 18 months.

Netflix’s revenue revisions have been steadily higher as well, just less robustly, which could be indicative of the operating margin leverage impacting EPS estimates.

Valuation:

Over the next 3 years, the consensus estimates expect an average 23% EPS growth, on 13% revenue for Netflix, while the stock is currently trading at an “average” PE for the next 3 years of 41x.

The trailing twelve month (TTM) cash-flow and free-cash-flow valuations are roughly 58x and 62x actual cash-flow. (More on this in the summary / conclusion).

In terms of “quality of earnings” Netflix’s TTM cash-flow and free-cash-flow covers net income 0.85x and 0.8-x respectively.

There is absolutely nothing cheap about Netflix’s stock, but that’s what happens when you have a communications giant (within the SP 500, NFLX is part of the communications services sector) that has substantial pricing power, a business model that continues to evolve into higher margin areas like advertising and live sports, and continues to expand across the globe. As this blog has mentioned in recent Netflix earnings previews (here and here), when your primary competitor’s CEO (Disney and Bob Iger) comes out publicly and comments on the competitive lead that Netflix has built on it’s competition, that says something.

Technical analysis:

Netflix put in a major top at $700 in late 2021, and consequently pulled back to the $150 area during 2022, and only broke out above the $700 in September ’24.

This stock could easily correct on a tough quarter, which would likely bring it down to the $1,000 area.

Summary / conclusion:

With EPS and revenue revisions consistently positive, and Netflix’s ability to push through price increases, and with the advertising revenue expected to be a larger piece of the revenue picture, this blog continues to be a long-term holder of the stock, but one fundamental improvement I’d like to personally see is cash-flow and particularly free-cash-flow start to “lever”.

That could also mean the business might be starting slow, but with the revenue “flywheel”, steady improvement in free-cash-flow and an improvement in the “free-cash-flow” yield, would be welcome. (NFLX’s free-cash-flow yield at the time of the Q1 ’25 earnings release was just 1.62%, not uncommon for a growth company (and very often worse) but still a low number.

Netflix repurchased $3.5 billion worth of stock in Q1 ’25, which for the one quarter was 50% of all the share repurchase dollars spent in calendar ’24. It looks like analysts have built more repurchases into coming quarters, which should be supported by greater free-cash-flow.

Netflix is a top 10 holding for clients with a roughly 4% weighting in client accounts.

There is no question the company is in the sweet spot of the business model as they have left competitors in the dust the last 3 – 5 years, and continue to innovate with live sports. The model’s pricing power is a huge plus. Personally I’d like to see better cash-flow and free-cash-flow generation.

None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future results. Clients and readers should gauge your own comfort with portfolio volatility and adjust accordingly. The information above may or may not be updated and if updated may not be done in a timely manner.

Thanks for reading.