Netflix reports their first quarter, ’25 after the closing bell on Thursday, April 17th, 2025, with street consensus expecting $10.5 billion in expected revenue growth, $3 billion in operating income and $5.72 in earnings per share (EPS) for expected year-over-year growth of 12%, 14% and 5% respectively.

Netflix, even with the expected price hike this quarter (the latest Netflix price increase just came through this month), faces very tough compares in 2025.

Here’s how the year-over-year (y-o-y) growth numbers looked in 2024:

- Q1 ’24 revenue, op inc and EPS: 15%, 54% and 91%

- Q2 ’24 revenue, op inc and EPS: 17%, 38%, and 48%

- Q3 ’24 revenue, op inc and EPS: 15%, 52% and 45%

- Q4 ’24 revenue, op inc and EPS: 16%, 52% and 102%

While expected revenue for Q1 ’25 is inline with previous quarters, both operating income and expected EPS growth, for Q1 ’25 is well below 2024’s actual growth rates.

Q4 ’24 results released in mid-January ’25, showed that the Q1 ’25 guidance was a little light at the same time Netflix raised revenue guidance for full-year 2025. (According to the notes (unsure of the source), 55% of the new member sign-ups came in countries with the tiered-ad plan. The 4th quarter saw the NFL games on Christmas Day, the Squid Games, and the Jake Paul – Mike Tyson fight.

Have to wonder what Netflix has planned for Q4 ’25.

Q2 ’25 per the current consensus is expecting $10.9 billion in revenue and $6.27 in EPS for expected growth of 14% and 28% respectively.

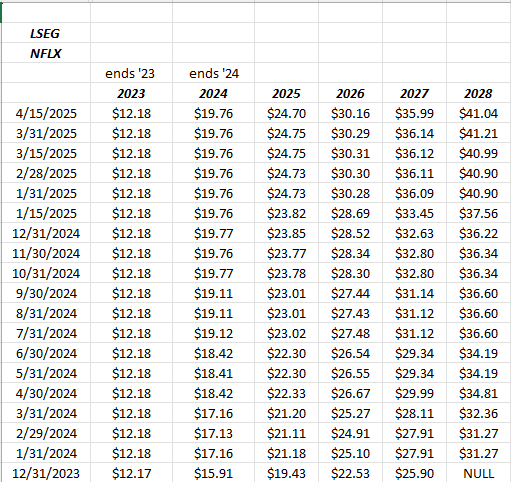

Netflix EPS revision trends:

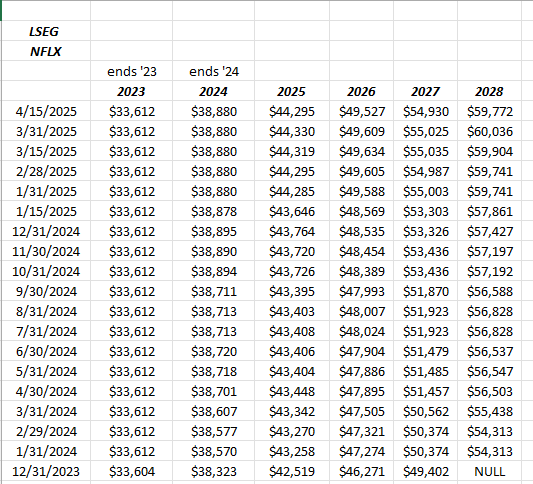

Netflix revenue revisions trends:

Both EPS and revenue estimate trends remain positive for Netflix, but the increase in EPS is more noticeable, thanks to Netflix’s improving operating margin. The Netflix operating margin has improved from the low 20% range in 2023 to 30% by the end of ’24, probably much of that due to Netflix’s pricing lower.

Valuation:

With a growth stock, valuation is usually the first negative cited, and Netflix is no exception.

Trading at 40x expected ’25 EPS that is expected to grow at 25%, the PE-to-growth ratio is probably a little smaller than expected, possibly due to the market turmoil since March 31 ’25, but it still leaves plenty of downside should there by anything in the earnings report that gives investors pause about long-term growth.

Preferring to look at the metrics over a 3-year forward time-frame, EPS is expected to grow (average) 22% over the next three years, with an average PE of 33x on 12% average 3-year expected revenue growth.

What looks even worse is the 55x – 60x cash-flow and free-cash metrics, which is somewhat understandable as Netflix continues to invest in sports programming. There has been a tremendous improvement in Netflix’s cash generation since Covid when Netflix was free-cash-flow negative for a period of years, but since 2022, the Netflix free-cash-flow generation has improved dramatically.

This blog’s intrinsic value estimate on Netflix is $1,050, while Morningstar has an estimate of $700 per share.

In late 2021, Netflix peaked at $700 per share, and fell all the way to $160 by mid-2022 in the midst of the fed funds rate increases that year.

Summary / conclusion: Netflix had a remarkable 4th quarter ’24 thanks to the NFL games, etc. Although on smaller scale, Netflix capex spend seems to resemble Amazon a little bit as the streaming giant tempers capex, and then when it sees an opportunity like the Jake Paul – Tyson match, and the NFL games on Christmas Day, capex ramps to 2x what it was in Q4 ’23.

The stock returned 84% in calendar ’24, so this blog’s Q4 ’24 earnings preview was probably too conservative, since the stock jumped sharply following earnings.

Without question, Netflix’s largest competitive advantage is the lead they have on their closest competitors like Disney and Amazon. As a Prime subscriber, I occasionally watch Prime streaming, and while there are some decent shows, it pales in comparison to Netflix.

Netflix has been a top 10 holding for clients, but after 2024’s gain, about 10% of the shares held have been sold, just to make sure that Netflix’s weight within client accounts doesn’t get too large.

There is a lot of bullishness surrounding Netflix coming into Wednesday night’s report, which is unusual given the market instability and uncertainty. The recent Wall Street Journal article and a could of other articles have talked positively around the stock, given any lack of tariff impact on Netflix’s business.

Frankly, I’d rather see a lot of bad news baked into a stock prior to earnings, than good news, since it limits the downside of any disappointment.

There is that $700 gap still outstanding and looming from what looks to be the October ’24 earnings report, but in some cases those gaps never get filled.

Readers should know that there is significant downside with a name Netflix, should earnings disappoint, for any reason.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal, even for short periods of time. EPS and revenue estimates are sourced from LSEG.

Thanks for reading.