One quick note

FBK Financial, a small-cap bank ($2 bl mkt cap) reports Monday night, July 14th after the close. The net revenue estimate is just $135 million per LSEG, and total annual net revenue this year is expected at $600 ml, with the annual EPS estimate of $3.66 currently. FBK is the old FirstBank, recently merged with Southern States, and that’s about all I know about the company fundamentally.

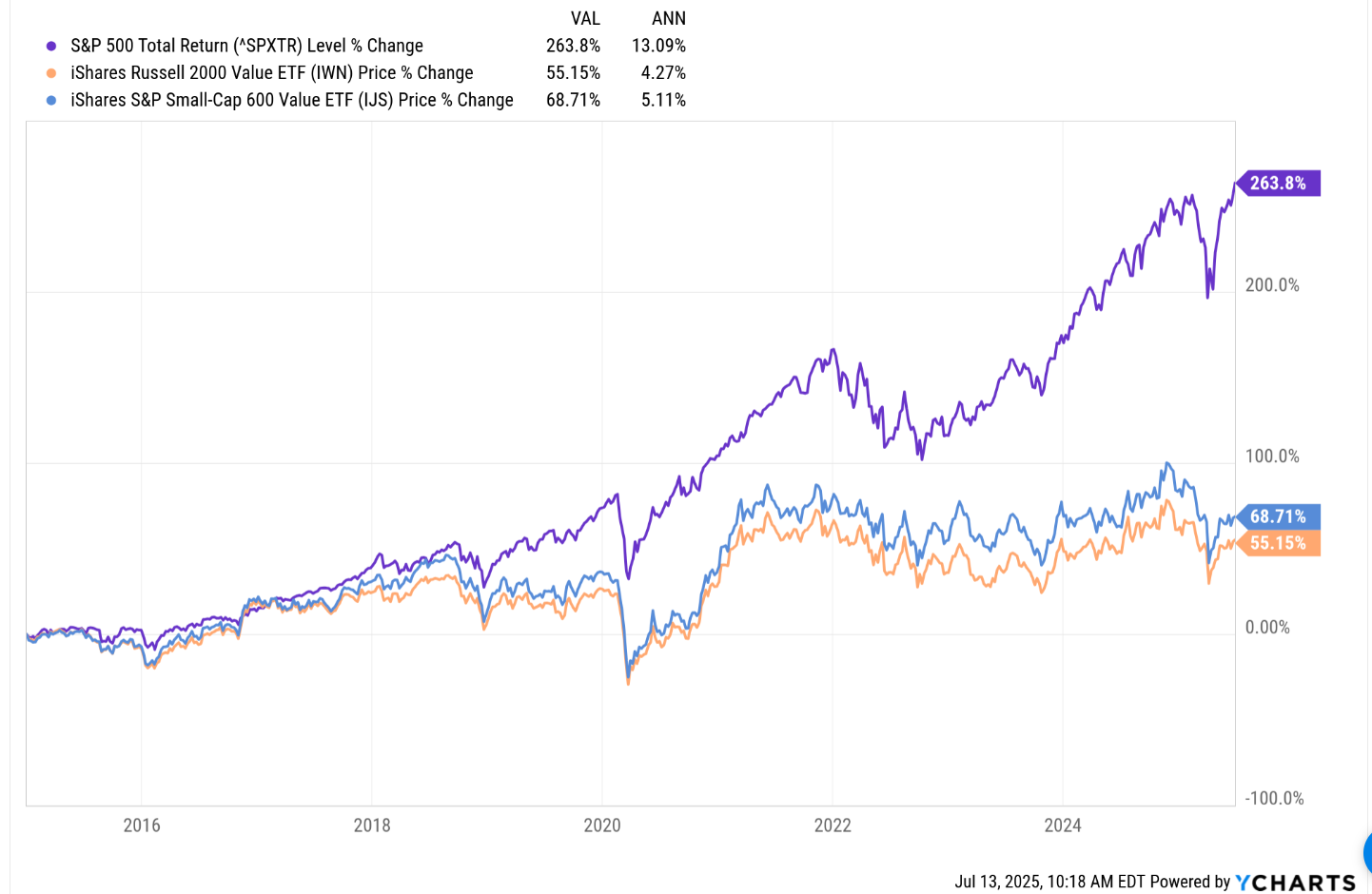

The point being that small-cap value has been a house of pain the last 10 years for anyone allocating assets and more so for anyone benchmarking against the SP 500, but ultimately this “pain” will come to an end.

Here’s the annual return charts comparing small-cap value to the SP 500 since 1/1/2015:

Chart source: Ycharts.

Just looking at two small-cap value ETF’s, the IWN (iShares Russell 2000 Value) and the IJS (iShares Smallcap 600 Value), financials are the largest sector in each ETF, at 25% of the market cap of the ETF’s respectively, and a lot of that 25% are small banks.

If there’s a beaten-down “non-correlated” (or uncorrelated) asset class to the SP 500’s bull market, it’s the Russell 2000 Value segment, and the biggest concentration within that asset class is financials. Recent blog posts on style-box updates and such have tried to focus small-caps and their relative under-performance for some time.

It’s becoming harder and harder to find “value” in this market after a 15 – 16 year secular bull market in the SP 500. This will be a controversial statement but “value” isn’t always defined as below 1x price-to-book or below 1x price-to-revenue, or below 10x EPS, or 8x free-cash-flow. Despite the PE ratio, sectors that have been long put-of-favor, and have seen little investor interest can get a catalyst that gives the group momentum quickly.

Citigroup earnings preview:

Citigroup (C) reports Tuesday morning, July 15th, before the opening bell, and analyst consensus coming into the 2nd quarter’s earnings release is expecting $1.60 in earnings per share on $20.98 billion in revenue for expected year-over-year growth of 5% and 4% respectively.

With Q1 ’25 earnings release, Citi mgmt affirmed their 2025 net revenue guide of $83.1 – $84.1.

In Q1 ’25 fixed income revenue rose 8%, while equity-related revenue rose +23%. The US Personal Banking (USPB) segment saw revenue increase only 1% y-o-y. That was thought to be a disappointment. The personal banking segment is Citi’s 2nd largest segment at 24% of net revenue and 18% of operating income behind the markets group.

Jane Fraser is Citi’s CEO and I suspect she is working through how to reinvigorate growth at the personal banking giant, while determining what’s the right staffing level. The headcount reductions may not be done.

Citi’s real strength is it’s valuation: it’s still trading below both tangible book value 0.97(x) and book value (0.80x).

The stock is trading with a PE of 12x and 9x respectively at it’s current price with current estimates, which are well below the expected EPS growth in 2025 and 2026 of 22% and 29% respectively.

Here’s Citi’s 3-year historical and 3-year expected EPS growth rates: (click on spreadsheet):

![]()

That’s Citi’s story right now – if the expected EPS growth rates materialize, and the $10 EPS estimate for ’27 comes to fruition, the stock should trade at least to $100 per share or 10x earnings. Citi is probably a little extended here from a trading perspective, but let’s see if those expected EPS estimates hold up after Q2 ’25 results.

Citi’s achilles heel remains, which is the low ROE or ROTCE, which is just high-single-digits, versus high-teens or low 20% ROTCE for the rest of the so-called money-center banks.

Any decent pullback on Citi, and the stock would likely be added to client accounts.

JPMorgan earnings preview:

If there’s a yin to Citi’s yang, it’s JP Morgan’s (JPM) stock. While Citi still trades below book and tangible book value, with a high single digit ROE, JPM trades at 15x – 16x earnings for expected high-single-digit EPS growth over the next 3 years, while it likely can still generate high teens, low 20% ROTCE or ROE. (JPM generated better-than 20% ROTCE for 4 of the last 5 quarters and the only reason the 5th quarter can’t be confirmed is that it wasn’t recorded in my notes at the time of earnings.)

Most analysts do a poor job estimating JPM’s forward “earnings per share”. Forward EPS estimates are typically low-balled by the Street. In late ’23, JPM’s 2024 EPS consensus was $13.50’ish, but actual EPS for ’23 was north of $18 at $18.21. 2024 EPS estimates started out in the mid $12 expectations, but actual EPS ended the year at $15.84. In 2022, a tough year for financials, the EPS started out at $12 flat and finished at $11.98, so analysts get the tougher year right, but have a harder time modeling the upside surprise, which frequently happens with brokerage stocks. When the market conditions are right, JPM can produce healthy upside surprises.

JPM’s stock has been a machine the last 1,3, and 5 years (annual returns) returning 40.8%, 38.6% and 26.2% while Citi has returned 35%, 26% and 13% for the same time periods.

That being said, JPM is the 10th largest stock in the SP 500 by market cap, and while Berkshire is a bigger weight, financials don’t tend to remain long within that “top 10” category, particularly if the CEO will be leaving in a few years.

That – in my opinion – is the biggest risk to JPM is Jamie Dimon’s departure. He’s done a fabulous job in growing the bank, including the asset management and ETF groups, but the departure scenario keeps cropping up.

JPM’s Corporate and Investment Bank is 43% and 47% of Citi’s net revenue and net income respectively as of the April ’25 quarter.

For the most part, the fundamentals of the financial and banking sectors remained very healthy. High-yield credit spreads remain well bid, credit card delinquencies and defaults remain well contained, and credit defaults within high-yield debt remain in very low-single-digits, and I consider these metrics the “early-warning” system for the financial sector. Mergers & acquisitions were supposed to be robust this year, but the tariff turmoil likely postponed some of those deals. Still, the capital markets should make a positive contribution to the big banks results for Q2 ’25, while guidance will likely remain tempered if only for tariff uncertainty. Corporate loan growth for the last 12 – 18 months, is rather subdued, which is somewhat surprising, and I wonder if private credit is playing a role in that.

There is no question fed funds rate cuts would be a plus for the financial sector, even if the yield curve widens more than expected.

JPMorgan is clients single largest equity position today while Schwab is the 2nd largest financial position and Citigroup is within the top 15. Clients have seen regular trimming of JPM from accounts in small quantities to keep the stock’s weight within reason.

Technology and financials are now a whopping 47% of the SP 500’s market cap weight as of Friday, July 11th, 2025. Those sectors were the catalyst behind the two bear markets of the 2000’s, which I’m not sure yet is a positive or a negative.

Bespoke had an interesting paragraph in their weekly Bespoke Report: for Q1 ’25, in early April around the tariff turmoil, sentiment was bearish, anxiety was high, the stock market had sold off sharply, and there was a lot of worries over expected guidance. Now with Q2 ’25 earnings, sentiment is relatively positive, we’ve seen a sharp, 90-day rally in stocks, with almost a complete opposite set of conditions coming into Q2 ’25 results, versus Q1 ’25 results.

None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future results. None of this information may be updated, and if updated, may not be done in a timely fashion. Readers and clients should gauge their own comfort with market volatility and adjust accordingly.

Thanks for reading.