The big tech companies, or the so-called Mega-cap 7, do not report their Q3 ’24 financial results until Halloween week:

- Alphabet: Tuesday, 10/29/24 AMC

- META: Wednesday, 10/30/24 AMC

- Microsoft: Wednesday, 10/30/24 AMC

- Apple: Thursday, 10/31/24 AMC

- Amazon: Thursday, 10/31/24 AMC

Nvidia isn’t scheduled until mid-November ’24.

The point being that’s a big chunk of the SP 500’s market cap and earnings weight that will all get reported in a 72 hour time span at the end of October, just a week before the Presidential election.

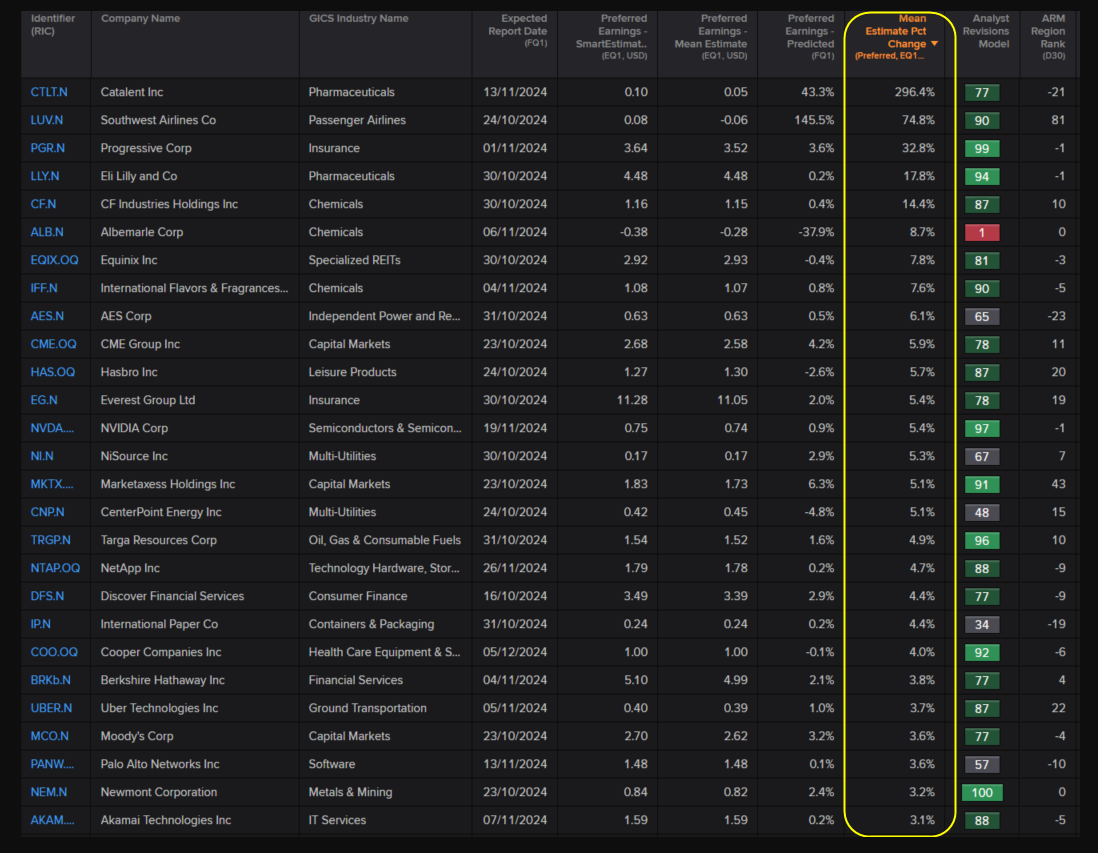

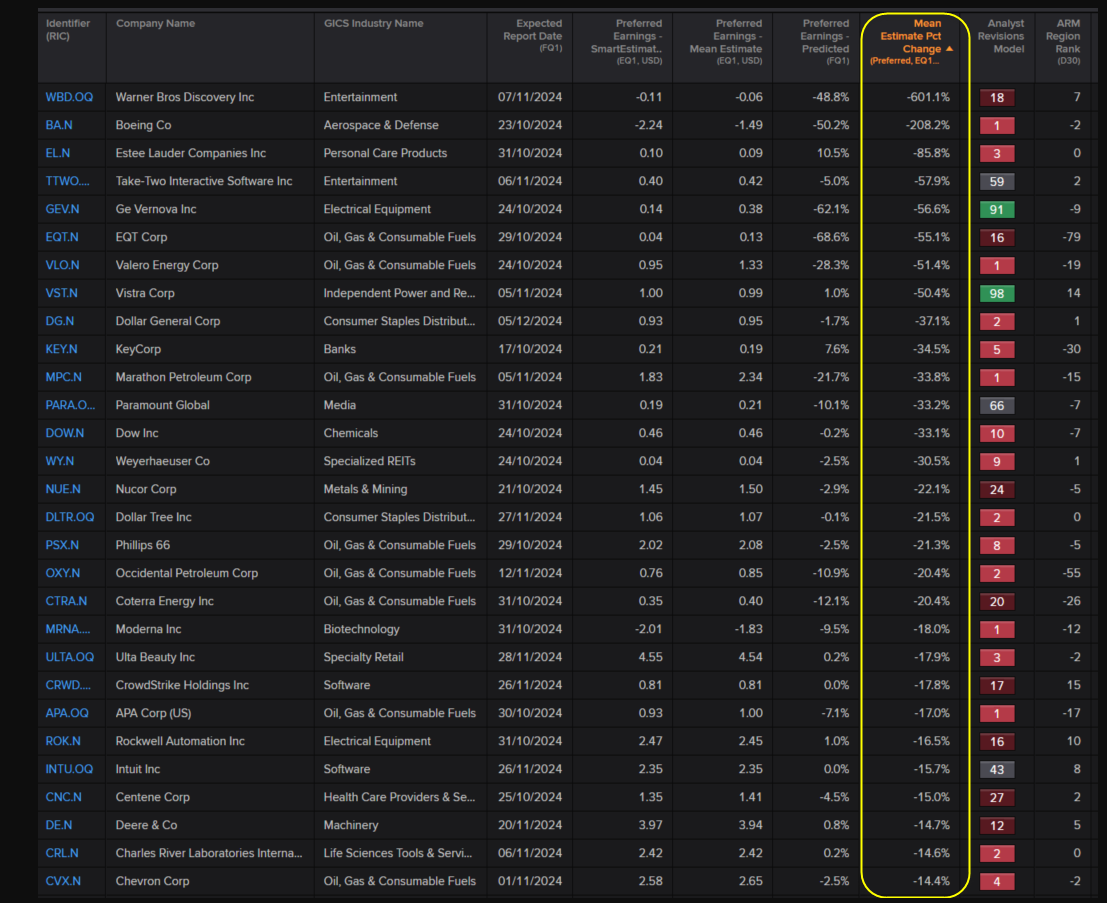

Largest “expected” positive and negative EPS surprises for Q3 ’24:

Positive:

Courtesy of LSEG – click on above

Courtesy of LSEG – click on above

Here’s a question for readers though: if the “upside” or “downside” surprise is that predictable, shouldn’t investors by buying the expected negative surprises and selling the expected upside surprises ?

The energy sector and Boeing (BA) are certainly leading the negative revisions.

At some point Boeing (BA) will be buyable for long-term investors.

IBM (IBM) and Tesla (TSLA) will be getting the closest scrutiny from this blog come Wednesday night, October 23rd, ’24. CME Group (CME) and Coca-Cola (KO) will also be seeing their valuation model’s updated. (Tesla is now the 12th largest stock in the SP 500 today, falling out of the top 10, so it’s pretty wrung out in terms of momentum. I worry that Elon is now getting distracted by politics. Tesla needs a lower-cost model for US consumers.)

SP 500 data:

- The forward 4-quarter estimate ended this week at $265.72, down slightly from last week’s $266.09;

- The PE on the forward estimate 22x, vs 21.8x last week, and 21x as of June 30 ’24;

- The SP 500 “earnings yield” is 4.53%, vs last week’s 4.58% and June 30’s 4.63%;

- There have only been 75 companies reporting Q3 ’24 to date. The EPS upside surprise is +6.4%. That’s still a little lower than Q2 ’24 at +8%, but still healthy.

Summary / conclusion: It’s the last week of the month where we get the big mega-caps reporting so we have another week to bide our time, and watch the action.

JPMorgan is having a tough time making a new all-time high, despite it’s good quarter. There is still a wet blanket over the major banks as net interest income is expected to be lower in calendar ’25.

The surprising metric to Netflix was that they guided ’25 revenue to be between $43 – $44 billion, or inline with the current consensus estimate of $43.5 billion, the surprise being they are giving that guidance 90 days ahead of their Q4 ’24 financial release, which is when investors and analysts usually get next years guidance.

This blog pegged the Netflix quarter properly (I thought).

This blog will be out with some bank summaries and some previews for next weeks stocks over the weekend and early next week.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Investing can involve the loss of principal even for short periods of time. All SP 500 EPS and revenue is sourced from LSEG.

Thanks for reading.