Source: EarningsWhispers chart

Tesla (TSLA), Meta (META) and Microsoft (MSFT) all report after the closing bell, Wednesday, January 29th, 2025. Three large-cap growth giants (part of the Mega-Cap 7) will have a significant influence on the market Thursday morning, January 30th, especially since the FOMC decision to be announced Wednesday afternoon at 1 pm central, often has an impact on the last few hours of trading that day. (Late Wednesday and after hours could make for interesting trading.)

Amazon (AMZN), and Alphabet (GOOGL) are scheduled to report the following week, the week starting February 3rd ’25, per the Briefing.com calendar.

On Thursday, investors get a small break from market-moving news, although more earnings news will be forthcoming with Apple (AAPL) Intel (INTC) and Visa (V) scheduled for Thursday, January 30th, ’25 after the market close. (It’s doubtful Intel is a market mover, but Visa, as a large-cap growth stock, is part of the SP 500’s leadership group the last two years.)

Friday morning is really what’s important (in terms of economic data) though, since December PCE and Core PCE are due out at 7:30 am central time. The market’s two most important inflation indicators are Core CPI and Core PCE, and while Core CPI was right in line at +0.2%, two weeks ago, and we saw a Treasury rally following the release, of the two releases, the Core PCE matters more.

![]()

Source: Briefing.com (click on the table to expand it)

Consensus is expecting +0.2% for December Core PCE. The mainstream media loves to raise the stress level of viewers in front of important data like this.

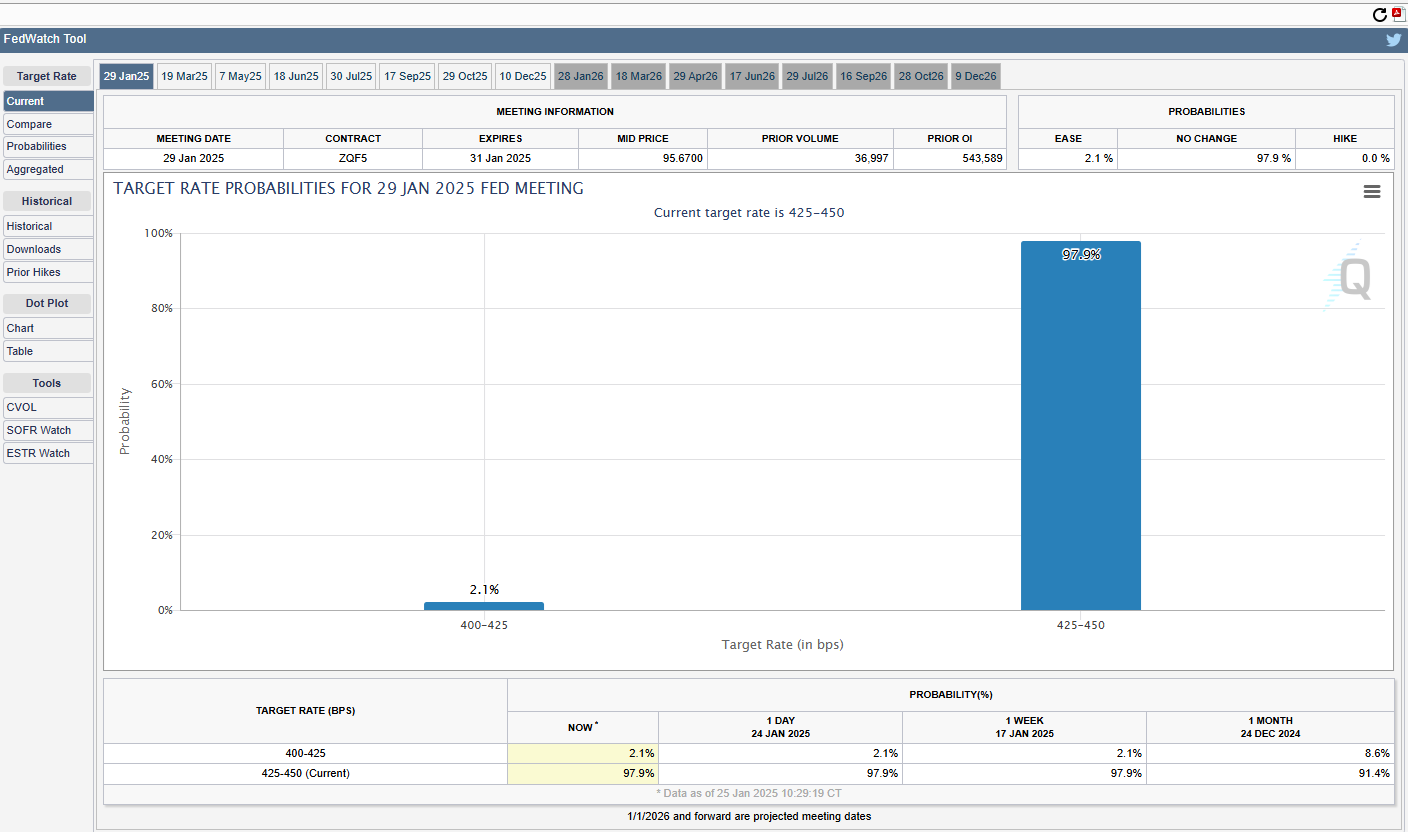

Fed funds futures:

While there is a 97% probability that the present 4.375% fed funds rate target will remain “unch’ed” at the Wednesday, January 29th FOMC meeting referenced above, the CME fed funds futures are currently forecasting a 27% probability of a 25 basis point rate cut for the March 19th, 2025 FOMC meeting. Let’s watch and see if that 27% probability changes on Wednesday afternoon, and then again on Friday morning after the December PCE data is released.

Personally, I do think the fed funds rate will continue to drop over time, certainly below 4% since the Fed statements indicate that the current fed funds rate remains above neutral at it’s current levels. Despite the hysteria of the mainstream financial media, I do expect the Fed will eventually see a core PCE and Core CPI around 2.5%, at which time they could declare victory.

Given the expected drop in fed funds in 2025, and a slowly declining inflation rate, there is still good opportunity (in my opinion) in the longer-end of the Treasury yield curve, or so-called ” adding duration” for investors. It won’t likely happen next week, but it should happen. High-yield and investment grade-credit remains well bid. A 5% 10-year Treasury yield would be a perfect spot to add duration, but investors may not see that level again. Above 5% on the 10-year Treasury yield, and there’s a bigger problem for Treasuries.

Summary / conclusion: 78 SP 500 companies have reported Q4 ’24 results as of Thursday night, January 23 ’25, and another 103 SP 500 components will report next week, beginning January 27th, ’25, both statistics according to LSEG.

Bloomberg is out with headlines this weekend talking about the “stocks jumping on earnings wins by the most since 2018”. That could be an accurate statement since the so called “upside surprise” or “beat rate” for SP 500 earnings for Q4 ’24 so far is +8.6%, versus last quarter’s very strong actual rate of +7.5%. (Here’s the blog post from January 3 ’25, where readers were given a heads-up to expect a Q4 ’24 earnings season..)

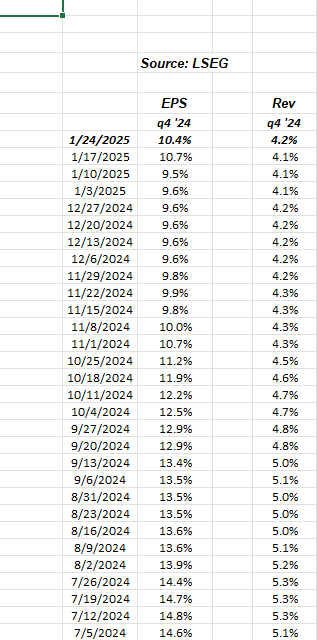

The tip off was the higher starting growth rate for Q4 ’24 EPS relative to other quarters.

Here’s the week-to-week progression in the expected Q4 ’24 SP 500 EPS growth. The low was 9.6% in early January ’25. Expect the actual Q4 ’24 SP 500 EPS growth to eventually come in around 11.5% – 12%, but much depends on the mega-cap 10 earnings of next week and the week after.

Healthcare and industrial sector EPS growth is expected at +4% and -0.3% respectively, for full-year 2024 earnings growth, just 2 – 3 weeks left in the reporting period and 8 weeks left in the calendar year quarter.

Those same two sectors are expected to grow EPS +20.4%, and +19.2% in 2025, with the industrial sector showing the most improvement in y-o-y growth since October ’24. (Healthcare numbers are unchanged.)

The defense sector, which typically trades better under Republican Administrations, will see Boeing (BA), Lockheed Martin (LMT), and General Dynamics (GD) report Tuesday and Wednesday this coming week. Defense is part of the industrial sector.

Clients are long the ITA (Defense ETF), as well as Boeing and Lockheed Martin coming into earnings this week. My biggest fear around the sector is that the defense and military budget will be used as a hammer for the deficit reduction nail. Congress did pass a $888 billion defense package last Spring ’24.

None of this is advice or recommendation, but only an opinion. Past performance is no guarantee of futures results. Investing can and does involve the loss of principal, even for short periods of time. All SP 500 EPS and revenue data is sourced from LSEG. None of this information may be updated, and if updated, might not be done in a timely fashion.

Thanks for reading.