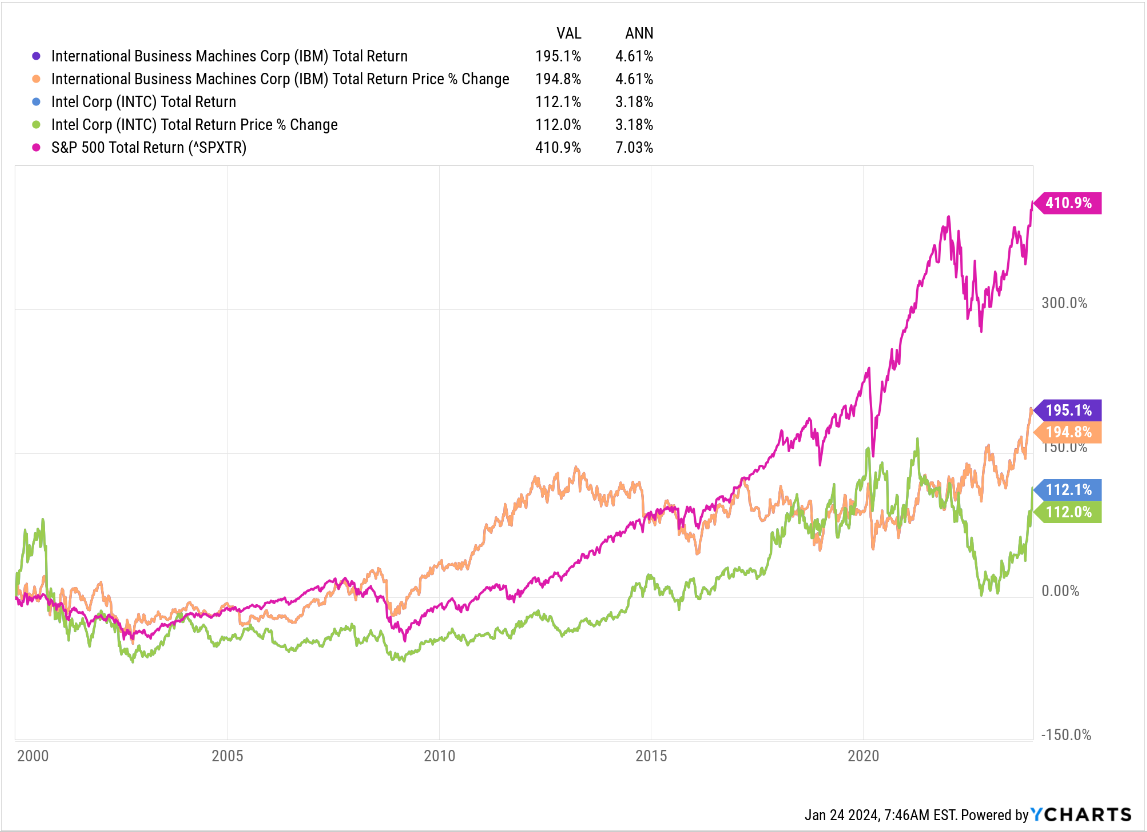

IBM last made a new all-time-high over 10 years ago, around the $213 – $215 are in April, 2013. Intel’s last all-time-high was September, 2000, when it hit $75.81 per share.

Here’s the performance of both stocks versus the SP 500 since 1/1/2000:

For performance sensitive readers, that’s brutal.

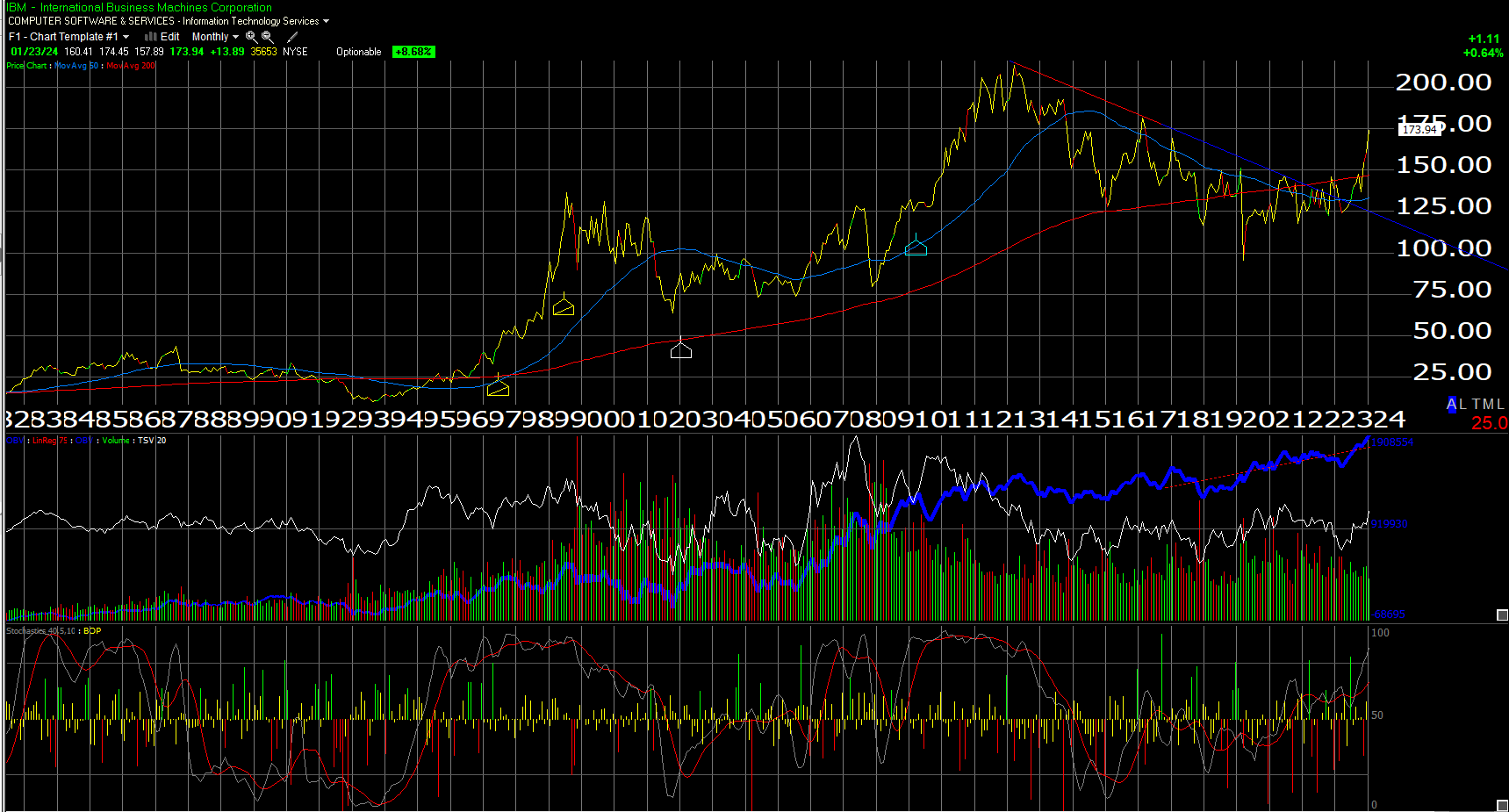

IBM: Technical analysis portends better growth for Big Blue

This monthly chart of IBM shows a significant break in the trendline in the stock beginning in Q4 ’23.

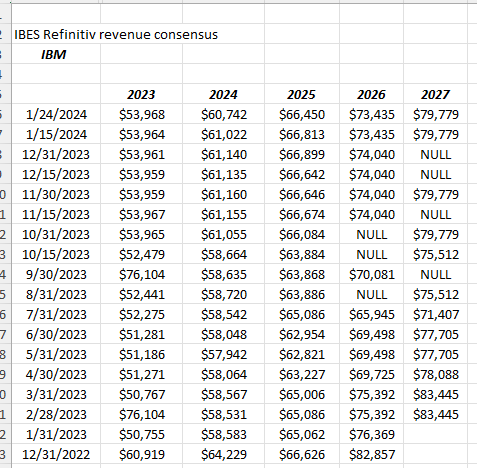

Tonight, IBM is expected to report $17.3 billion in revenue and $3.78 in EPS, which is 4% and 5% yoy growth respectively for IBM.

The 4th quarter every year is typically IBM’s strongest quarter of the year.

F04 2024, current sell-side consensus is currently expecting 4% EPS growth and 3% revenue growth, so the sudden improvement in the stock price, has not yet been driven by dramatic earnings or revenue improvement.

When looking at IBM’s business segments, (and it’s just an opinion), but Big Blue seems to moving closer and closer to a software firm. Morningstar has noted that the consulting business looks to be a decent long-term business, but RedHat is probably maxed out in terms of it’s potential (James Whitehead, RedHat’s CEO who moved over to IBM when IBM bought RedHat, has already left as of a few years ago), but’s it’s still a guess as to what IBM will look like in 5 years. Big Iron seems to be long gone for the former mainframe giant, but will software be the primary revenue driver in 2029 – 2030 ?

One of the more positive datapoints about IBM, looking at the estimates is that after 4 years of negative revenue growth (and this doesn’t adjust for the Kyndryl spinoff), low-single-digit revenue growth is expected the next 3 years.

IBM has been shrinking for years, and got even smaller with the Kyndryl spinoff.

IBM hasn’t bought back any stock in 13 quarters, even though free-cash-flow has started to stabilize around the $9 – $10 billion annual run rate at IBM, with the dividend consuming $6 billion a year. Maybe Big Blue will announce tonight a resumption of the share buyback program tonight.

Valuation: With the stock trading at roughly 16x – 18x earnings, for expected EPS growth from ’24 – ’26 averaging 6% – 10%, the multiple is not daunting, but the important metric from an “estimate” perspective, is expected low-single-digit revenue growth the next few years. Price-to-cash-flow and free-cash-flow is 12x and 14x. The dividend yield is just under 4% with the stock trading at $175 per share.

Conclusion / summary: Finally (maybe) Big Blue can generate some sustainable albeit low single digit revenue growth the next few years. Let’s see if there is improved guidance or some fundamental improvement in the company’s fundamentals to warrant the increase in the stock price the last few months. Big Blue has a history of being out of favor for years, and then catching a tail-wind. Maybe IBM has found a way to capture some of the AI frenzy.

Intel: Intel reports after the close Thursday night and sell-side consensus and analysts expect $15.1 billion in revenue to generate $0.45 in EPS for expected yoy growth of 8% and +350% respectively. Q4 ’22 is an easy compare for Intel when it generated a 41% and 91% revenue and EPS decline respectively.

Q3 ’23 saw INTC beat on EPS by 42% ($0.41 actual vs the $0.22 estimate), and a 4% revenue beat. With a manufacturing-heavy plant base, and all that operating leverage, the 4% revenue beat is just as important as the 41% EPS beat, maybe more so.

The stock has had a remarkable run off it’s Feb ’23 lows near $25 and has almost doubled in price in 12 months.

Forward revenue and EPS estimates are expecting an average of 11% revenue growth and 61% EPS growth from ’24 to ’26, which is against the two sharply negative years of ’22 and ’23. In 2022, Intel EPS and revenue fell 66% and 16% respectively and in ’23 – of Q4 ’23 consensus is met – revenue will fall 14% and EPS will drop 48%. That’s two years of pretty ugly declines.

Intel’s avg PE for ’24 to ’26 is 19x.

The sell-side consensus is clearly expecting a recovery in INTC in the next 3 years. The PC business which is 56% of revenue as of Q3 ’23 and all of Intel’s operating income, seems to be on the mend. The business I’m intrigued by – and not being an electrical engineer take it with a grain of salt – is the foundry business, which was started by Pat Gelsinger, and appears to be a beneficiary of an expected re-shoring of semiconductor manufacturing from Taiwan to the US – but it’s still just 2% of revenue, although I’ve seen a few analyst comments where Intel is adding some customers to the foundry business, perhaps at a pace that is faster-than-expected.

My big worry with INTC is that it generated a negative $10 billion in free-cash-flow on a trailing twelve month basis as of 9/30/23. Pat Gelsinger and the management team have had to add manufacturing capacity at a time where they are most financially-constrained.

Capex has exceeded “cash-flow-from-operations” for 6 consecutive quarters.

That’s painful for a capex-heavy business.

Intel obviously hasn’t bought back any stock in a while – 9 quarters – and they’ve cut the dividend to take some pressure off and restore some free-cash-flow.

When looking at the results Thursday night, “revenue upside” is more valuable for Intel here than EPS upside, but revenue upside will likely drive EPS upside.

Overall conclusion: Old technology like IBM and Intel are starting to stir. Good investors always teach us that “always trust price” and both stocks have seen a nice bounce in the last few months. If IBM and Arvind Krishna, can find a sustainable business model, IBM probably has more upside than Intel simply because of Intel’s operating and financial leverage, from it’s manufacturing footprint. That being said readers will likely get sharper selloffs in Intel given the above.

Clients own very small positions in both stocks. Growth continues to work over value, but both of these companies look to turning themselves around after brutal periods of underperformance.

None of this is advice or a recommendation, and past performance is no guarantee or suggestion of future results. All revenue and EPS estimates and data is sourced from the LondonStockExchange Group (LSEG). Even though these two stocks are considered old tech, they are not without risk and volatility.