Ed Yardeni was featured on CNBC’s Morning “Squawk Box” with Brian Sullivan and Sara Eisen on Friday, December 27th, 2024, and Ed – being the SP 500 earnings guru – thought that the SP 500 EPS in 2025 could print “$280’ish” while the LSEG current, full-year calendar estimate for 2025 is $275’ish.

Here’s the recent history of full-year calendar year estimates for the SP 500 EPS:

- 2025: SP 500 EPS growth (est) +13% (to $275.07 current), SP total return – unknown

- 2024: SP 500 EPS growth (est) +10% (to $243.94 current), SP 500 total return YTD +26.79%

- 2023: SP 500 EPS growth +1% to $222.94; SP 500 total return +26.19%;

LSEG hasn’t updated subscribers on current SP 500 estimates since December 13th, which isn’t a big issue since this time of year analysts really aren’t changing numbers much, hence the number of actual estimate revisions are lower, but the current forward 4-quarter estimate from LSEG is $263.39 (as of 12/13/24), while the current full-year calendar estimate for 2025 is $275 is $275.07.

Readers should remember, Q4 ’24 SP 500 earnings don’t really begin in mid-January ’25, when the big banks start to report.

The December ’24 nonfarm payroll report isn’t scheduled to be released until January 10th, 2025 (per Briefing.com), and the big banks aren’t scheduled to report Q4 ’24 earnings until the following week (also per Briefing.com calendars), so some key reports are a little delayed to start 2025.

If the Trump Administration can reduce the overall corporate tax rate to 15% – 17%, from the current 21%, that alone might make the difference in the “Yardeni estimate”.

The Trump Administration will be dueling between better growth initiatives, (i.e. lower taxes, lower reg’s, etc.) and deficit reduction, i.e. less spending.

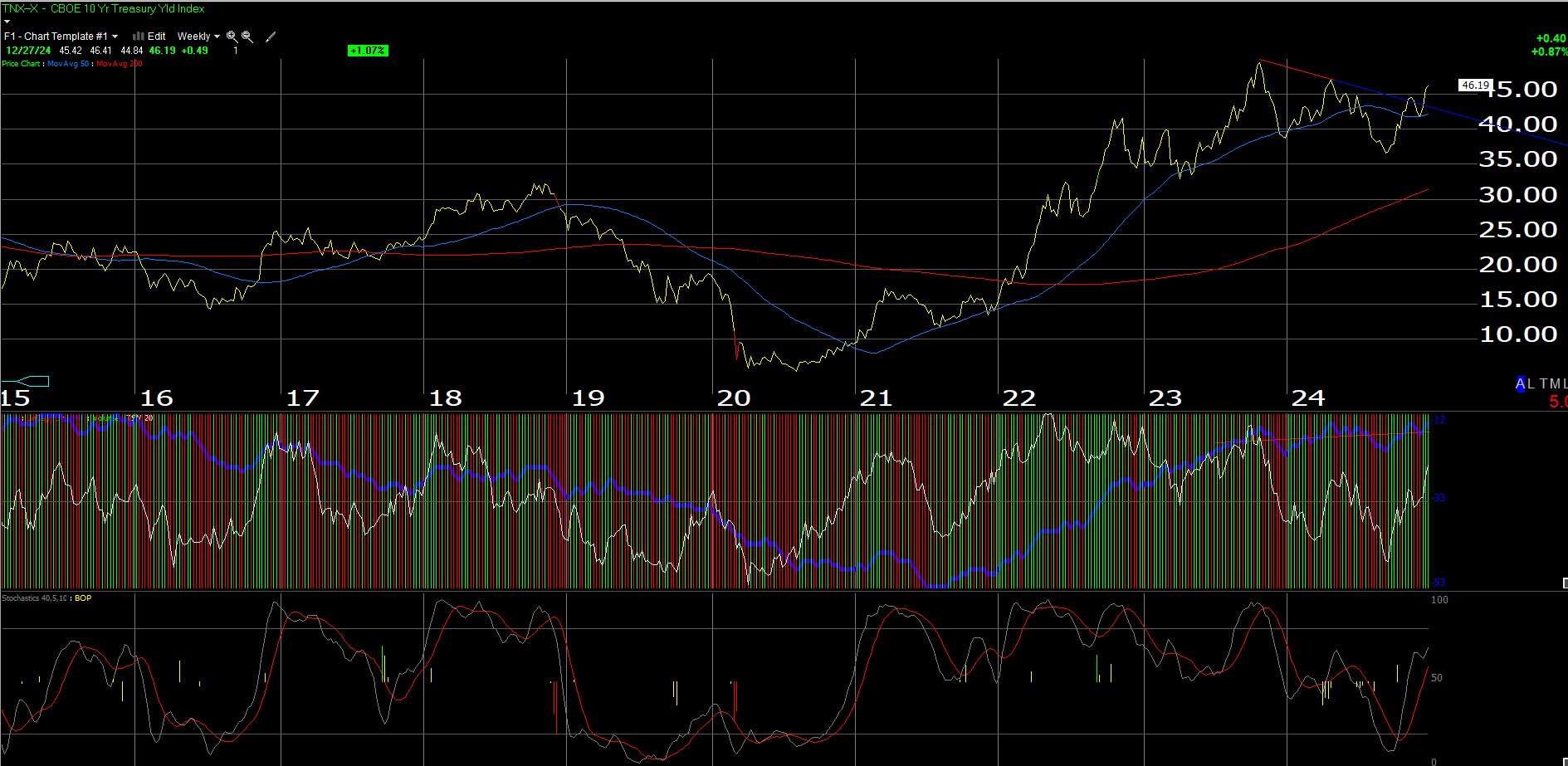

10-year Treasury Yield:

Here’s a weekly chart of the 10-year Treasury “yield” contract traded at the Chicago Board of Options Exchange.

The multi-year high yield tick for the on-the-run 10-year Treasury was the week of October 25th, 2023, when the 10-year yield hit 4.99%.

Prior to that late ’23 high tick, the last time the 10-year Treasury yield was up at these levels was between mid-2007 and mid-2008 or prior to the 2008 Financial Crisis.

Here’s my take for readers who may not be bond-market savvy: wait until the 10-year Treasury yield trades above 5.00% yield before getting too worried.

There will likely be a trade up in the 10-Treasury yield from 4.62% (last Friday’s closing yield) to 4.99% in early ’25, and it will get a lot of attention. Readers can hedge their bond portfolios with the TBF (unlevered ProShares Short Treasury short ETF), or if readers like to take more risk, the TBT (ProShares UltraShort Treasury ETF, which is levered.)

The yield curve is “steepening” currently, which is a positive for the banking system. The yield curve inversion that lasted over 2 years, is the brazilian jiu jitsu equivalent of the rear-naked choke, which, if you’ve ever been choked like that, you watch the lights on the ceiling gradually dim, and eventually turn black as your oxygen supply is cut off, and you are put to sleep.

It’s simply an educated guess but a “neutral” fed funds rate is probably closer to 2.5%, and thus anything over a 3.5% Treasury yield is likely an opportunity to add duration to your bond portfolio, but it will likely take more time to play out, maybe most of 2025, depending on the current Administration’s potential tax cuts, which would be bullish for US GDP growth, but likely worry the Treasury market, and push yields higher.

KRE (regional bank ETF) and Charles Schwab (SCHW) are two client holdings that should benefit nicely from yield curve steepening. Both are still below their 2021 highs, and thus have lagged the financial sector’s gains this year.

PE expansion / contraction:

So much emphasis (including this blog) is placed on year-to-year SP 500 earnings growth, when in fact, market returns are probably more influenced by “PE expansion” and “PE contraction”.

Frankly, I expect 2025 will probably be a year of “PE contraction” which means that – with expected 10% SP 500 EPS growth expected in 2025 – any market return below 10% will be a year of PE contraction.

This decade to date, the SP 500 has seen 3 years of PE expansion, and 2 years of PE contraction.

The magnitude of the difference between 2023 and 2024’s SP 500 EPS growth i.e. +2% and +10%, versus the SP 500 total return the last two years of +26% and +27% (with two trading days remaining in the year) could spell trouble for the benchmark. These latest comments add to this December 1 ’24 blog post about how the stock market math is working against 2025.

Just one opinion – take is as such.

Summary / conclusion: Please excuse the very crowded article title this weekend. The goal is to cover as much ground as possible in terms of laying out next year’s probabilities.

The “PE contraction” argument is a very valid reason 2025 could be tough.

The Treasury yield curve is likely going to continue to steepen, and then as the fed funds rate gets cut, the long end will rally nicely.

None of this is advice or a recommendation, but rather an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal, even for short periods of time. LSEG has NOT published their SP 500 earnings estimates for two weeks now. This isn’t on me. None of the above information may be updated, and if updated, may not be done so in a timely fashion.

Thanks for reading – always grateful for readers time.

Nice summary and thoughts, thanks. Always a good read.

thanks, WR.