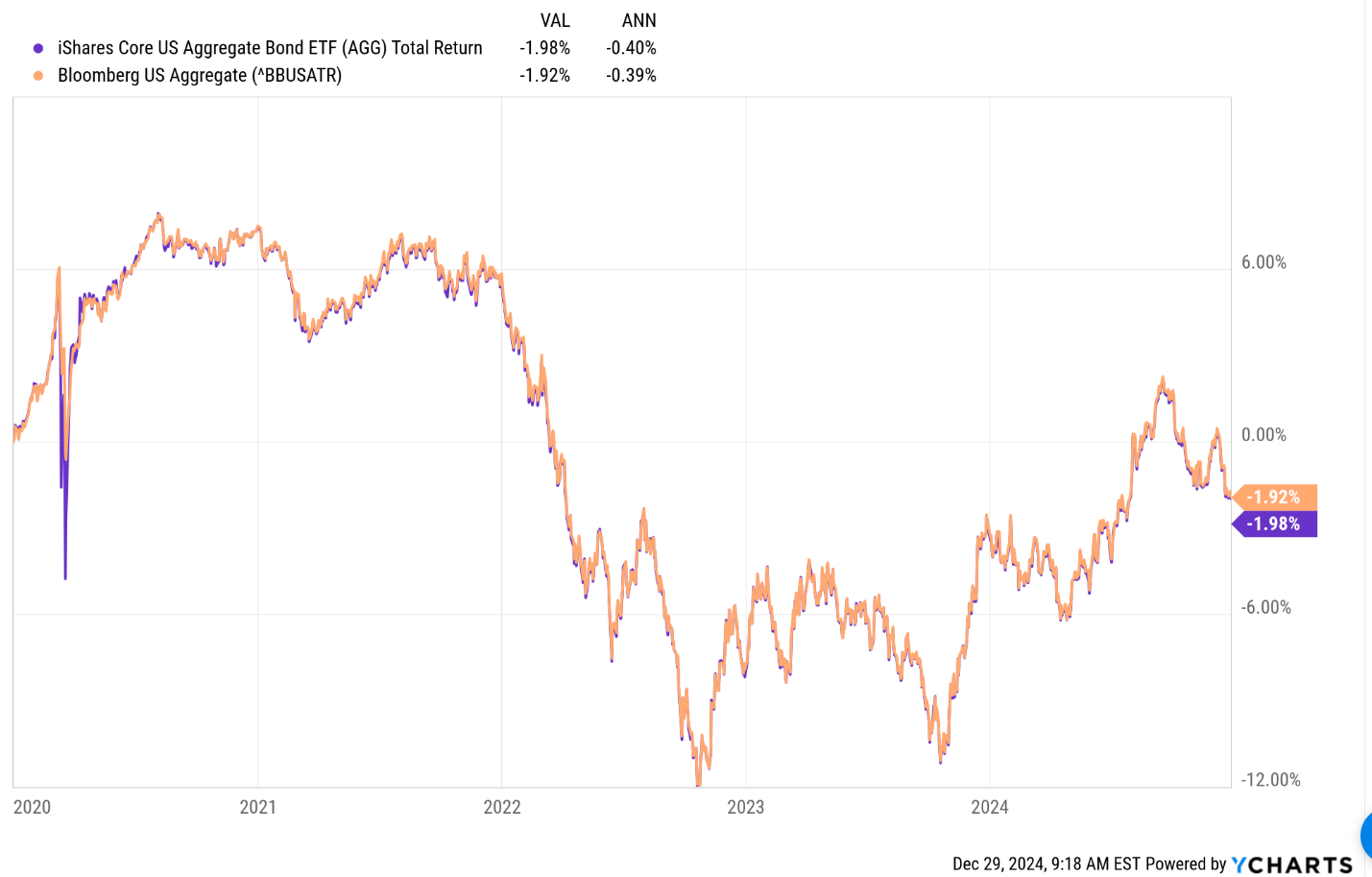

Here’s a decade-to-date total return chart for both the AGG ETF, and the Barclay’s US benchmark index courtesy of YCharts.

This a grim chart for the AGG decade-to-date, as it shows a negative total return from 1/1/2020 to 12/27/2024.

Rick Reider, Blackrock’s Chief Investment Strategist for Fixed-Income, has been on CNBC a few times, and he’s always worth a listen to, but Rick has been talking 7% yield portfolios of late, which is probably easier to find when you’re a Blackrock fixed-income or mutual fund trading desk, than if you’re an advisor, looking for individual Treasuries, bond ETF’s or fixed-income mutual funds.

Blackrock’s flagship Strategic Income Opportunity Fund (BASIX) and which sports a 22% weighting in below-investment-grade bonds (per the current Morningstar data) has a year-to-date total return of 4.88%, which is still respectable, versus the JP Morgan Income Fund (JMSIX), which has a current weighting in high-yield of 36% – 37%, and has a year-to-date total return of 7.51%.

Blackrock launched BINC or the Flexible Income Active ETF in late May ’23, which sports a 34% weight in below-investment-grade credits. When you pull the ticker up on Morningstar, the ETF is now named the “iShares Flexible Income Active ETF” so I don’t know if Blackrock has any involvement in BINC, but I thought it was Blackrock’s and Rick Reider’s response to try and capture more credit-spread in a tough bond market environment overall.

This blog swapped the Blackrock Strategic Income Fund (BASIX) entirely for the JP Morgan Income Fund (JMSIX over 18 months ago, given the management fee is much lower at 40 bp’s for the JMSIX, versus Basix’s 100 bp’s, and – as you’d expect – the outperformance of the JMSIX (versus the AGG) has been much greater.

High-yield credit has won 2024, as the HYG (iShares iBoxx High-Yield credit ETF) has returned 7.83% YTD, while the Bloomberg High-yield index (unsure of it’s composition) shows a 8.01% YTD total return as of 12/27/24.

Also performing well this year is the EMB (iShares JP Morgan USD Emerging Market Dollar ETF) which returned 5.58% YTD as of 12/27/2024.

If the various fixed-income asset classes were to be listed top-to-bottom in terms of 2024 YTD returns, here’s what the list would look like:

- Bloomberg High-Yield Index: +8.01%

- Corporate high-yield (HYG): +7.83%

- Emerging Market JPMorgan USD Credit (EMB): +5.58%

- Bloomberg Investment-Grade index: +1.90%

- Mortgage-Backed Securities (MBB): +1.05%

- Barclay’s Aggregate (AGG): +1.04%

- Municipal Bond ETF (MUB): +0.89%

- High-Grade Corporate ETF (LQD): +0.68%

Return source: Bloomberg for Bloomberg indices, Morningstar for representative ETF’s

Credit wins 2024 for sure, and the lower the credit rating, the better the outperformance for investors, but with US credit spreads at all-time-tights, or very close to the record, credit-spread investors need to be wary of credit risk. Like any market, risk comes on quickly.

Keep an eye on credit defaults as tracked by the credit rating agencies. As credit defaults (i.e. bankruptcies) start to rise, high-yield credit spreads will start to widen out, and you might suddenly start to find a bid in the Treasury market.

This being said, credit will likely have another positive year similar to 2024, IF (and it’s a big IF), President Trump and the Trump Administration can get the US corporate income tax reduced from 21% to 15%. While some of the mainstream media made fun of President Trump by not rationalizing his desired 15% corporate income tax rate, all I know is my own rationalization for wanting lower income tax rates, it’s that I don’t want to give more money to the US government – or any government for that matter – and that I can save and invest my own money better than the US government can. Personally, I’d love to see personal and marginal income tax rates reduced by this next Congress, but (again) the deficit hawks will surely push back on any measure that doesn’t bring spending and the deficit down permanently.

“Duration” or a bond / fixed-income ETF’s changes to interest-rates (i.e. interest-rate sensitivity) has worked against bond returns this year, and decade, but really since 2022 when the Fed started moving the fed funds rate off of zero. However, by the Fed’s own admission they’ve overshot the “neutral” fed funds rate by moving to 5.375% in late July ’23, and are now in the process of bringing the fed funds rate back down to neutral, currently at 4.375%.

Summary / conclusion:

The pro-growth, lower corporate income tax objective for the Trump Administration could result in another year for high-yield credit spreads in 2025, but know that credit spreads are bumping up against “all time tights” to Treasuries. If you want the “anti-credit” or credit hedge trade in 2025, own longer-duration Treasuries, since the two asset classes have been negatively correlated since 2022.

Other than that, unless the US economy weakens markedly (and that seems unlikely given credit spreads, job growth and the overall health of the US consumer), it could be a tough decade for Treasuries and duration, as we now have at least 2 years of a “pro-growth” Presidential Administration.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal even for short periods of time. All fixed-income return data is sourced from either Morningstar or Bloomberg and is noted as such. None of this information may be updated, and if updated, may not be done so in a timely fashion.

The Top 10 Holdings will be released on January 1 ’25.

Thanks for reading.