Congratulations to the US military for the successful rescue of the 2nd airman this weekend in Iraq. That had to be a big moment and a huge morale booster, for the military and the teams that were sent in to find the airman. (“No Person Left Behind”: Gotta love the US military.)

With Monday morning, April 6th, we’ll see the market reaction to the events over the long weekend, although it doesn’t seem like much has changed around the Strait of Hormuz. From the basic statistics being read around the Strait, about 20% of the world’s crude oil production flows through the Strait, which is not insignificant.

So how does this impact international equity and fixed income ?

Well, when the first air strike by the US and Israeli Air Force hit Iran on February 27th, 28th, 2026, crude oil spiked, interest rates across the globe started to rise, and the dollar started to strengthen.

As we saw in March, none of the above-referenced factors is typically good for equity and / or bond investing.

What was really hurtful for the international equity and bond asset classes, the groups were coming off their best year in 2025 since 2005 – 2006. International had good momentum, and then it all stopped on a dime on February 27th.

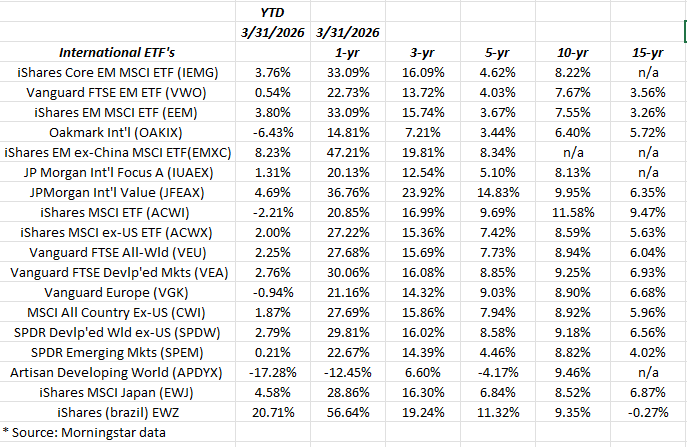

That being said, here’s the annual return data for international equity:

As of 3/31/26, all of these various international equity mutual funds (with one exception) and ETF’s had positive YTD ’26 returns, which means that the asses class still handily beat the SP 500, even though most are well off their highs.

This blog’s largest international asset class holdings are the same (JPMorgan Int’l Developed Value (JFEAX), Ishares EM ex-China (EMXC) ETF, and a smaller position in the iShares MSCI Japan ETF (EWJ), as they were last year when the asset class written about, here, here, and here. These three previous posts were from late 2025, but here’s a post from late, 2024.

Summary: When Maduro’s rendition back to the United States for criminal prosecution occurred, the general discussion was that the world had a plentiful supply of crude oil, so getting additional crude out of the ground in Venezuela was a longer-term priority, rather than something that had to be done quickly. While the Strait of Hormuz complicates the issue greatly, it’s also not a supply issue, i.e. we could probably assume that sooner rather than later the demand and supply for crude oil will quickly return to equilibrium, once the Strait can be insulated from attacks.

The most compelling aspect to the International annual return table is the “5-year” annual return data, which for most of the individual holdings, remains below 5% per year.

The final reason to consider international equity is that the SP 500 secular bull market in the US is now over 18 years old. Looking around for “non-correlated” to the US bull market improves the chances protecting principal from a nasty bear market in the SP 500.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. All the annual return data is sourced from Morningstar.

Thanks for reading.