It’s no mystery that international has outperformed the SP 500 in 2025, and not by a small amount.

The dollar’s direction will likely determine whether 2026 is a repeat of 2025 for the asset class, and the top strategist’s on Wall Street, like David Kelly of JPMorgan and Rick Rieder of Blackrock have both said the dollar is still too strong and needs to come down more.

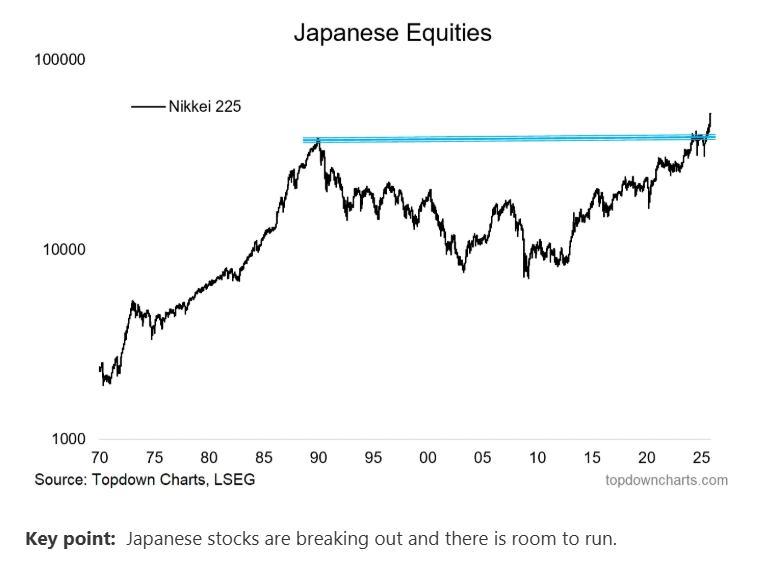

Japan and the Nikkei:

Callum Thomas of TopDownCharts, who hails from New Zealand, has been posting on X and LinkedIn for years, and does a good job.

This chart above from TopDown Charts shows the breakout in the Nikkei 225, the Nikkei’s first poke of it’s head above the 1989 high – and its happened in just the last year.

This blog is playing the breakout via the EWJ or the iShares MSCI Japan Index Fund ETF.

Here’s the annual returns for the EWJ as of 10/31/25:

- 1-year: +25.52%

- 3-year: +20.79%

- 5-year: +9.35%

- 10-year: +7.25%

- 15-year: +6.77%

Morningstar’s returns tracks something called “earliest available” annual return, which for the EWJ would be it’s first trading month, which is December, 1991, or two years after the Nikkei’s peak in 1989, and that “earliest available annual return” is just +2.85% over the last 33 years.

The 5-year return is still less than 10%, and note the spreadsheet at the top of this page, and how the 10 and 15-year returns are still below 10%.

In the last 12 – 18 months, international as an asset class has closed the gap with the SP 500, but the sentiment around non-US is far less frothy than the US.

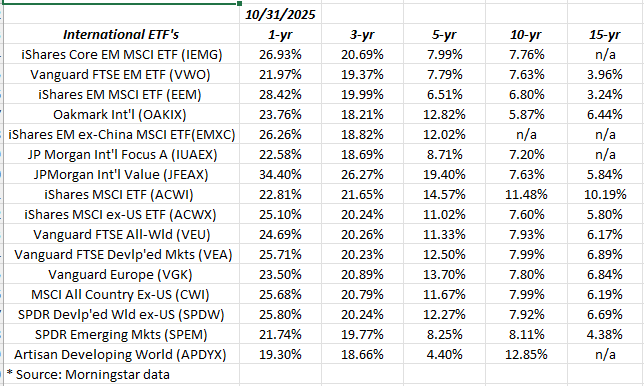

Top 10 – 12 Holdings as of 10/31/25:

- JP Morgan Income Fund (JMSIX): YTD return +6.33%

- JPMorgan (JPM) common equity: YTD return +32.11%

- JPMorgan Developed Int’l Value (JFEAX): YTD return +36.05%

- Amazon common stock (AMZN): +11.32%

- Microsoft (MSFT) common equity: +23.44%

- Nasdaq 100 (QQQ) equity ETF: +23.51%

- Schwab (SCHW) common equity: +28.81%

- Alphabet (GOOGL) common equity: +48.87%

- IBM common equity (IBM): +42.13%

- Tesla common equity (TSLA): +13.05%

- iShares Emerging Market ex-China (EMXC ETF): +31.81%

- iShares +20-year Treasuries (TLT ETF): +6.80%

SP 500 YTD return as of 10/31/25 was +17.40%

- This blog manages $55 million via separate accounts at Charles Schwab and has done since 1995. There are 4 – 5 larger accounts that represent roughly 20% of the $55 million, and several of those are 100% equity.

- The three JPMorgan positions were not intentional, although JPMorgan has been very supportive of this blog’s work, and when this blog was looking for an international fund / ETF in late ’24 to re-allocate to, the JFEAX fund – even in ’24 – was performing ahead of those funds followed.

- Most client accounts are managed on a “balanced” basis with allocations targeted towards 60% equity / 40% fixed-income mix.

- The large-cap tech positions have been trimmed over the last 12 – 14 months, since this secular bull market is now in it’s 15th year, with the start coming on March 9, 2009. Rather than re-balance at the end of a quarter, the rebalancing is done almost continually, with rotation from what has outperformed materially to an asset class, sector or stock that has underperformed materially. It takes time to sell larger positions often due to tax constraints and it often take time to build out-of-favor positions into material positions.

- The three newer positions in 2025 were the JFEAX, the EMXC, and IBM. Not on the top 10 list yet, but shares are still being added are Boeing (BA), EWJ (Japan Nikkei ETF) and Nike (NKE).

Summary / conclusion: Having lived through the 2000’s decade when international investing completely missed the late 1990’s bull market and only began to outperform in mid 2000 through 2007, only to collapse once again in 2008, 2025 was likely one of the best years of non-US asset-class returns since the late 2000’s.

In my opinion (and it’s only that) is that the “China-centric” gravitational pull from 2000 to 2007, when China was growing 15% per year, from 2000 to 2010, 2011 (and maybe longer), may be the reason the international outperformance lasted only several years in the 2000’s. Everything non-US was dependent on that Chinese economic engine.

The fact that China is no longer as dominant as it once was, may actually be a reason international returns could see a longer streak of high-single-digit, low double-digit returns over the next few years, given the asset class has been dead money for so long.

None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future results. None of this information may be updated, and if updated, may not be done in a timely fashion.

Thanks for reading.