Nike, (NKE), the beleaguered sports footwear and apparel giant reports their fiscal Q3 ’26 financial results after the closing bell Tuesday, March 31st, 2026.

The stock has been the proverbial “house of pain” (hat-tip to the Jim Cramer’ism), down -22% annualized from Nike $179 peak in late November ’21 to its current price of $52 – $53 per share in late March ’26, versus the SP 500’s +10% return for the same period. The only conclusion that can be drawn was that Elliott Hill and his team were left with the proverbial “nuclear winter” landscape (certainly amongst footwear retail) when he assumed control from the former CEO, but the fact is Elliott has also made some progress at the retail level getting Nike footwear (particularly Nike footwear) prominently reinstalled at Dick’s (DKS).

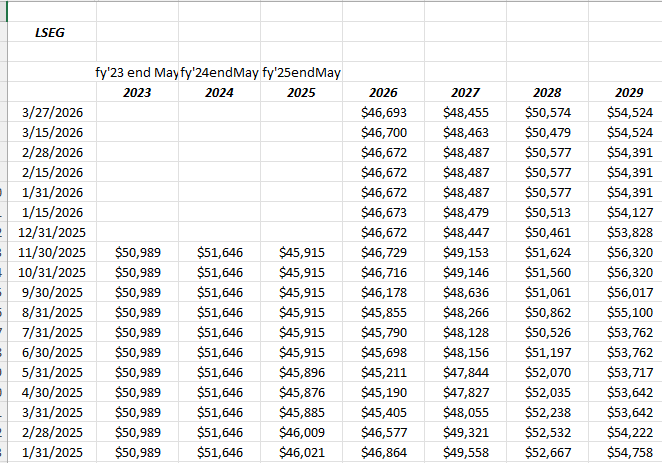

Current Street expectations for Nike’s fiscal Q2 ’26 are $11.23 billion in revenue, EPS of $0.28 and operating income of $512 million, for “expected” declines y-o-y of 0%, -48% and -31% respectively.

For fiscal Q4 ’26, ended May ’26, street consensus is looking for $11.3 billion in revenue to generate $386 bl in operating income and $0.21 in EPS, for expected y-o-y growth of 2%, EPS growth of +50%, and operating income growth of +20%, but the grim prospect of the Q4 ’26 numbers is that the actual numbers remain sequentially down from fiscal Q3 ’26’s estimates, while fiscalQ4 is typically the strongest quarter of the year.

Jeffries recently put out a Nike update after Dick’s results (DKS) quarterly results were reported noting that DKS’s management was “unequivocally positive” on Nike’s strength in running innovation. (The Austin Texas store was mentioned in one of the last two calls as perhaps being Nike’s epicenter on running innovation and improvement for the brand.)

My own anecdotal experience with Dick’s and Nike is that on Sunday, March 22nd, ’26 I went into a Dick’s Sporting Goods Store in Oak Brook / Lombard, Illinois, looking for some ice pack for the knees devices (old man) and the place was absolutely jammed. I had trouble finding a parking spot and the checkout lines were stretched well back into the store. Nike footwear and apparel was displayed prominently both on the main floor and the upper, running-related floors.

EPS and revenue estimate revisions:

The EPS estimate revisions for Nike look back one year: note the drop after the tariff implementation in early ’25, from fiscal February, March ’26 and ’27 through the present. The tariff compares get easier now, but there is still an impact. The bigger issue could be the relationship with China and how “unfriendly” China can make US companies as perceived by the Chinese citizens, while selling US products into the Chinese market from a public relations perspective.

Nike revenue estimate revisions are unchanged over the last 15 months for fiscal ’26, ’27 and ’28.

I would have preferred to see some mild upward drift to the estimates signaling at least low-single-digit revenue growth.

Valuation:

This has been written about on past Nike previews, but Nike’s peak valuation when the stock was trading at $179 in November ’21, was 50x EPS, 4.9x price-to -TTM revenue and 40x and 43x cash-flow and free-cash-flow.

Today, those same multiples are now 34x expected ’26 EPS for a -27% EPS y-o-y growth rate, (or 23x for an expected 47% EPS growth rate in fiscal ’27), a 1.5x price to TTM-revenue valuation and 30x and 28x cash-flow and free-cash-flow (ex-cash).

Still a lofty valuation, but the price of the stock has come down, as has the numbers.

The stock still isn’t cheap, with the exception of the dividend yield which is now 3.15% (assuming full-year dividend).

A technical look at the stock:

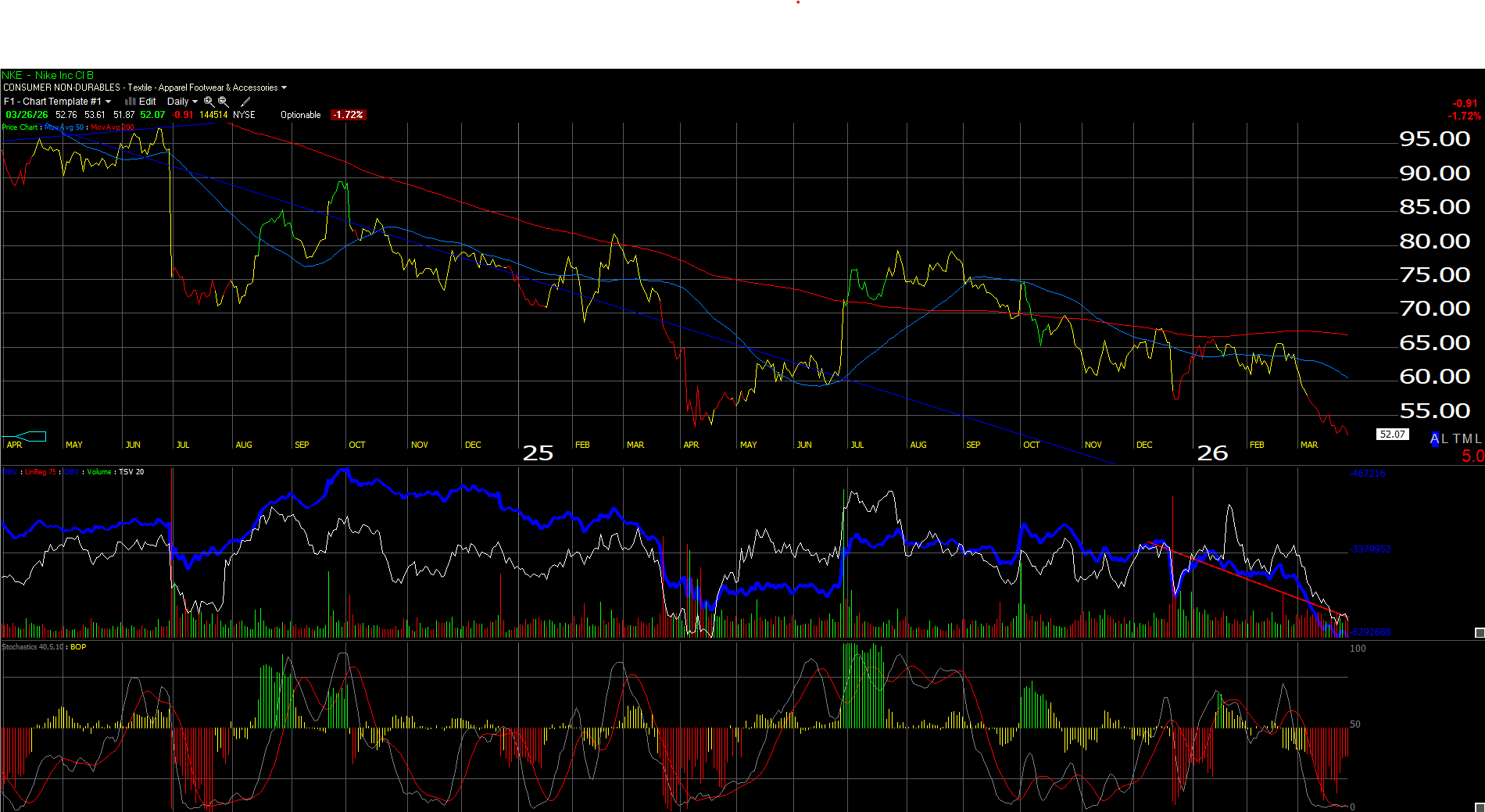

Technically, Nike is very oversold on the Worden daily chart (bottom lower-right panel) and it is getting there on the weekly chart.

I like the bottom with the early April ’25 lows near $52, but the stock cannot go lower than this after they report next Tuesday night, March 31.

Summary / conclusion: I’d like to put a valuation on Nike’s stock and say I think Nike is worth “X” but I can’t without seeing some return to at least mid-single-digit revenue growth. Nike is a like a bleeding wound that quarter-after-quarter seems to find another hole to dig itself into, and I’m talking China and the present strained relationship with China, and the stock tends to slip lower after seemingly good news.

Nike is seeing some signs of progress with North America revenue +9% y-o-y, led by the running franchise, but to give clients a historical perspective, China used to account for 20% of Nike total revenue, but a whopping 50% of Nike EBIT, but that EBIT percentage has now fallen to 19% from the peak around 50% in late 2021, 2022.

Again, here’s the consensus for “expected” y-o-y revenue growth, EPS and operating income, for the all-important Nike fiscal Q4 ’26 to be reported late June ’26:

- Revenue +2% y-o-y

- EPS: +50% y-o-y

- Operating income: +20% y-o-y

These y-o-y numbers are due to easier compares vs the fy Q4 ’25, not to better growth in the business model, which is ultimately needed.

From a portfolio construction standpoint, this blog never owned Nike in the last 20 years, until it dropped down to around $130 in early ’23, where it was initially bought, but the stock was then sold, and then repurchased after it went through $100. Nike has been a huge disappointment but Nike’s abrogation of the retail market by the past management team and allowing numerous sneaker brands, like Hoka, Skechers, and the slip-on tennis shoe evolution to grab all that shelf and market share really was an unmitigated disaster for the brand.

Nike is still owned given it’s non-correlated price movement with the post-Covid, 2020 bull market.

Elliott Hill – in my opinion – is more Mark Parker than John Donahoe, and I suspect Elliott Hill and his team can return the Nike brand – at least partially – to part of it’s former glory.

Any sign that the stock will hold low-to-mid $50’s Tuesday night March 31, ’26 will be a big technical positive.

None of this is advice, recommendation, but only an opinion. Past performance is no guarantee of future results. Readers should gauge their own comfort with portfolio volatility, and adjust accordingly. LSEG is the sole source of this blog’s EPS and revenue estimates for both the SP 500 and individual stocks.

Thanks for reading.