Cisco (CSCO), the former networking giant that is still trying to reshape and reinvent itself, 25 years after the large-cap growth and large-cap technology bull market ended, reported their fiscal Q3 ’25 financial results last week.

Cisco managed to generate a 4% upside in EPS, with a $0.96 print (versus the $0.92 estimate) on a 1% revenue upside surprise.

The non-GAAP operating margin also beat at 34.5%, and Cisco raised guidance for fiscal Q4 ’25.

While AI orders exceeded $600 ml, thus surpassing $1 billion for Cisco, it’s been downplayed since Cisco’s annual revenue is expected to be $56.5 billion in fiscal ’25 versus $53.8 billion in fiscal ’24, thus AI orders are still a small percentage of revenue.

The Splunk acquisition is likely the bigger deal for Cisco, as the acquisition greatly enlarges the security division at Cisco (see historical numbers below), and is expected to be an area of growth for the network giant. Cisco management did say that organic growth numbers will be reported for Splunk after Q4 ’25, or after this quarter end.

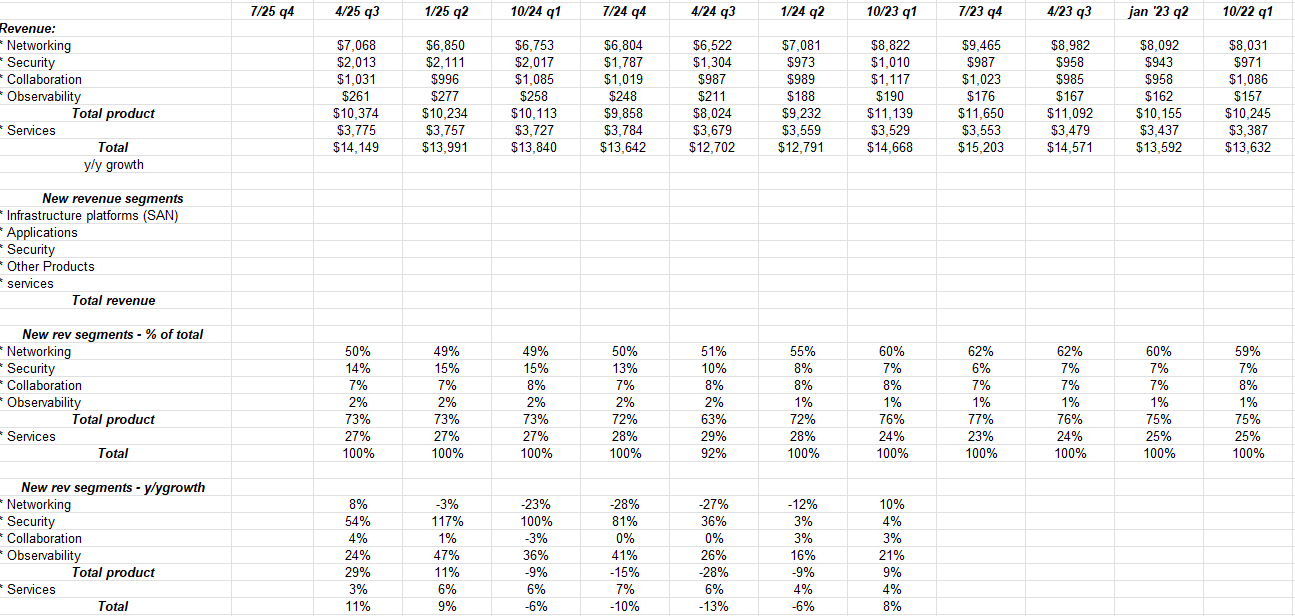

Source: earnings report, internal spreadsheet

Readers can see how the Splunk acquisition led to the sharp increase in the security segment as a percentage of Cisco’s revenue and y-o-y growth, but that y-o-y growth – after Q4 ’25 – will start to reflect the true or organic growth rate of the security segment, and not acquired growth.

Summary / conclusion: This blog has acquired a small position in Cisco and will likely continue to acquire shares, given the free-cash-flow yield of 5%, and the fact that – in this secular bull market for the SP 500 that started in March, 2009 – the stock has dramatically unperformed the SP 500, and thus represents an un-correlated or non-correlated security, relative to the benchmark.

With fiscal ’25 ending July 31 for Cisco, full-year ’25 growth will be 1% revenue and 2% EPS (expected) growth, hardly torrid, but the next three fiscal years (’26 – ’28) are expecting 5% revenue growth and 7% EPS growth. Even a disappointment or warning wouldn’t likely dent the stock too much at 15x forward EPS.

The above points were all covered in the earnings preview of Cisco, but with uncertain markets, I’m warming up more to the stock.

This blog’s internal model values Cisco closer to $70 – $75, so the discount to perceived fair value isn’t that yawning, while Morningstar’s fair value is mid-$50’s.

The Cisco management team really needs to come up some model to generate faster revenue growth. Business models tend not to last as long in the technology sector, but it’s also easier to reinvent the tech model and morph it into another growth area – like from the cloud to AI – than say a financial or industrial company or retailer changing it’s stripes.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results.