The Moody’s downgrade – the last downgrade from the Aaa level – of U.S. Treasury debt that occurred on Friday, May 16th, 2025, after the market close – was probably not a coincidence given the headlines around the Trump Administration’s tax and budget bill that saw some resistance last week from Republicans in Congress. The fact is there is gamesmanship and negotiations around every major Congressional bill, but Moody’s may have gotten to the point where this seemed like “more of the same” from a spending standpoint, and it was time to act. (Texas Representative Chip Roy’s, (R., Tx) Friday rant carried on the major news networks may have been the final nail in the coffin for Moody’s.)

Medicaid seems to be the big sticking point, as well as SALT to a smaller extent, but Medicaid spending reductions of $880 billion were expected to pay for part of the $1 trillion defense bill and some expected tax cuts.

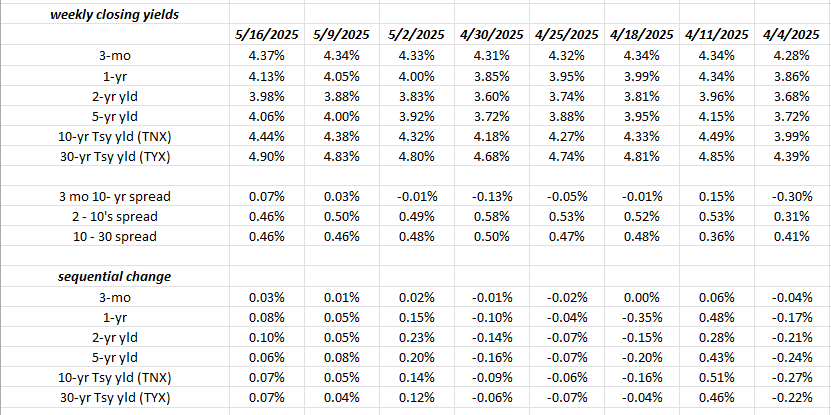

The above spreadsheet is a look at the Treasury yield curve updated every Friday afternoon, starting with the “Liberation Day” selloff in early April ’25.

The above spreadsheet is a look at the Treasury yield curve updated every Friday afternoon, starting with the “Liberation Day” selloff in early April ’25.

Note the HUGE jump in Treasury yields the week of April 11th, and since then the various yields have been range-bound, capped by 4.5% on the 10-year Treasury and 5% on the 30-year Treasury.

Is the credit rating downgrade enough to break the technical resistance of the 10-year and 30-year Treasury ?

The 10-year Treasury yield traded as high as 4.80% in mid-January ’25 so that’s ultimate resistance, while the 30-year Treasury recently tested January ’25’s high tick of 5% and so far has held. The 30-year Treasury yield through and above 5% on heavy volume, would probably result in further curve steepening for the rest of the Treasury yield curve.

The surprising aspect to the economic data so far in ’25 (for me anyway) is the very good core CPI and core PCE inflation data from January through April, although April PCE and core PCE doesn’t come until May 30th.

If the President and the Treasury Secretary hadn’t catapulted the market’s anxiety level with Liberation Day, investors could make a plausible case from just the inflation data alone that Jay Powell and the FOMC might be (or might have been) a lot closer to lowering the fed funds rate, but with tariff’s inflation impact, the FOMC and Powell are back to neutral. (The FOMC and Powell said more than once in late ’24 that the fed funds rate was still “restrictive” and monetary policy was still more restrictive than neutral, probably offset by what is still – as Jay Powell has also mentioned – a healthy labor market.)

As was noted in the SP 500 earnings update yesterday, high-yield credit spreads have improved smartly both the last two weeks and from the week of April 11th, when high-yield credit spreads peaked. That’s a plus for the equity market but not so much for Treasury total returns.

Summary / conclusion: Treasury Secretary Bessent shortly after Liberation Day, did a press conference or interview (can’t recall which) and took investors and the American public through the math and the calculus of the tariff strategy, and the budget bill, all of which was designed to reduce the budget deficit from a record 7.5% of GDP to closer to 3.5%, which sounded pretty ambitious then, and more so now.

Tariffs are expected to generate $700 – $800 billion in income for the US, once the negotiations are concluded.

One thing that struck me about the President’s Saudi Arabia trip was that OPEC (twice) had announced sharp production cuts of 440,000 bpd (barrels per day), so my guess is that these two events probably were related or connected more than the random observer might notice, since Secretary Bessent noted around Liberation Day that lower crude oil prices were a way to bring down US inflation, and help Americans with more discretionary income (my words, not his).

Interest on Treasury debt is now the largest single line-item expense in the US budget so the Trump Administration needs to get the FOMC to lower the fed funds rate, and not by 25 – 50 bp’s to help – along with Medicaid reductions to get that budget deficit lower.

This blog is still bullish Treasuries in ’25, and likes high-yield and investment-grade credit, but all this works only if the labor market weakens enough to let Powell and the FOMC reduce the fed funds rate, and the longer-end of the Treasury curve ultimately flattens.

Again, the Treasury market must sense that deficit reduction is real.

Most clients are long and overweight corporate high-grade and high-yield corporate credit and then offset with Treasury (or TLT) positions. No mortgages, no muni’s a very small exposure to non-US fixed income ETF’s. (All muni positions were sold the day after the President was elected and the Republican majority gained control of Congress.)

This could all go wrong quickly. (The bast laid plans and all that.)

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results.

Thanks for reading.

Why did you sell all muni positions?

Republican President and Congress typically means lower tax rates, which means less demand for muni’s. When Pres Biden and the Dem’s won in 2020, and were in control in Washington, i bought muni’s since Dem’s typically mean tax increases (increases demand for tax-exempt income) and Republicans typically means lower tax rates (and thus less demand for tax exempt income).